U.S. natural gas exports to Mexico continue to grow

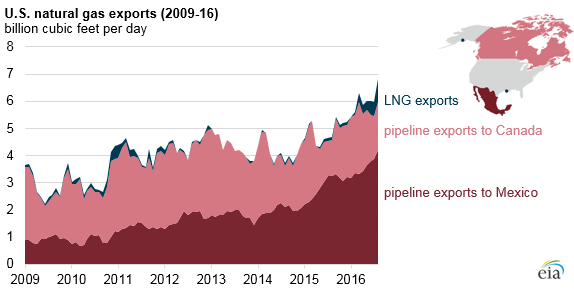

U.S. pipeline exports of natural gas continued to grow in 2016, and they have doubled since 2009. Almost all of this growth is attributable to increasing exports to Mexico, which have accounted for more than half of all U.S. natural gas exports since April 2015. In August, the United States exported 4.2 billion cubic feet per day (Bcf/d) of natural gas to Mexico via pipelines. U.S. daily pipeline exports to Mexico through August 2016 are at a yearly average of 3.6 Bcf/d, 25% above the year-ago level and 85% above the five-year (2011–15) average level.

In 2015, Mexico’s energy ministry (SENER) announced a five-year plan to significantly expand the country’s natural gas pipeline network to accommodate higher levels of natural gas imports from the United States. These imports would help meet increasing power demand, offset declining domestic natural gas production, reduce reliance on LNG imports, and create new markets for natural gas in currently supply-constrained regions. The plan proposed 12 pipeline additions, increasing the existing network capacity and adding more than 3,200 miles of new pipeline through Mexico.

According to SENER’s July 2016 update, contracts have been awarded for 7 of the 12 pipeline projects. The largest and most expensive of the awarded projects is the Sur de Texas-Tuxpan pipeline, which aims to supply the Mexican states of Tamaulipas and Veracruz with natural gas from southern Texas via an underwater route through the Gulf of Mexico. The pipeline will extend nearly 500 miles and provide a total transport capacity of 2.6 Bcf/d.

Growth in Mexico’s domestic electricity market has largely driven the country’s increasing natural gas usage. Because of the availability and affordability of U.S. pipeline natural gas, Mexico is meeting its growing electricity demand with generation from new natural gas-fired plants. U.S. natural gas exports to Mexico are expected to continue to grow in the short term, and SENER forecasts a widening gap between domestic production and demand through the end of the decade. Mexican imports of natural gas continue to outpace most projections. The 4.1 Bcf/d exported in August 2016 matched the level originally forecasted in 2013 to be reached in 2018.

However, uncertainty in Mexican demand growth, particularly from the power generation sector as natural gas-fired capacity competes with renewables and nuclear generation, may slow the increase in Mexico's natural gas imports, leading to lower pipeline capacity utilization. Domestic natural gas production may also rebound and reduce the need for pipeline imports from the United States.

Principal contributor: Kirstin Berndt, Mike Mobilia

Tags: exports/imports, international, Mexico, natural gas