Effects of renewable technology capital costs on electricity capacity and generation in two illustrative regions

Release Date: February 28, 2020 | Full report

Introduction

This paper analyzes a series of alternative cases that vary International Energy Outlook 2019 (IEO2019) Reference case capital cost assumptions in two regions for wind and solar electric power plants to explore the effects on the adoption of these technologies. Analysis of these cases shows that changes in capital cost assumptions tend to produce proportional shifts in the generating mix.

Two regions are examined, Other Non-OECD[1] Asia and Other Non-OECD Europe and Eurasia[2] , which differ in their exposure to electricity demand growth. Although Reference case levels of renewable technology costs result in some growth in wind and solar generation in all regions, the higher renewables penetration rates in regions with high demand growth such as Other Non-OECD Asia do not appear in regions with low demand growth such as Other non-OECD Europe and Eurasia in the Reference case.

Overall, three factors determine the growth of electricity generating capacity from renewable sources in the IEO2019:

- Government policies

- Electricity demand growth

- The cost and available resources to build new wind and solar facilities relative to other sources of generation

This analysis holds the first factor static. Both regions evaluated have relatively little policy mandating renewable generating source adoption, and the policy assumptions are not varied in this analysis, isolating the impact of capital cost from policy factors.

This analysis varies the second two factors, using the two regions as illustrative of different electricity demand growth patterns, and makes explicit changes to the assumptions related to renewable capital costs. Although capital costs for wind and solar generating technologies have declined substantially since 2010, future cost trajectories and the related effects on the adoption of these technologies remain uncertain and are location dependent. This paper uses a set of low and high renewables cost assumptions to examine two distinct kinds of competitive thresholds for electricity generating capacity.

The high cost cases help to illustrate the first competitive threshold: the point at which new renewable generation is economic to substitute for other new generation resources. In regions with high demand growth such as Other Non-OECD Asia, new renewable generation technologies are built instead of new conventional generation technologies as the least cost alternative. On an economic basis, new renewable generation capital costs must be competitive with the capital and operational costs for new facilities of the conventional technologies.

The low cost cases help to illuminate the second threshold: the point at which new renewable generation is economic to displace generation from existing generation capacity. In regions with low demand growth, such as Other Non-OECD Europe and Eurasia, new renewable generation technologies must displace existing conventional generation technologies as the least cost alternative. On an economic basis, the choice to displace existing generation means capital costs of renewable generation technologies are lower than the costs to operate and maintain existing conventional plants.

Analytic methodology

First used in IEO2019, the International Electricity Market Model (IEMM)[3] can examine these economic decisions. IEMM, a component of the World Energy Projection System Plus (WEPS+)[4], is a least-cost linear program that uses an economic model to optimize capacity planning and dispatch. IEMM receives regional electricity demands and fuel prices as inputs from the WEPS+ database and reports out regional projections of power sector fuel consumption, electricity capacity, and electricity generation by fuel and technology. IEMM’s least-cost optimization model illustrates the effects of renewable generation technology capital cost assumptions on capacity planning and dispatch decisions.

IEMM develops renewable generation capacity projections based on existing installed capacity, which is subsequently augmented by planned capacity additions to satisfy load growth projections, taking into account renewables policy targets and goals. The modeled renewables targets serve as a floor for renewables growth in any given region, and the model can—and in the IEO Reference case does—build additional renewable generation capacity if required as part of the least-cost mix of new and existing capacity needed to meet electricity demand.

The capital cost trajectories for electric generation capacity in the IEO2019 Reference case incorporate learning factors—reductions in capital costs over time as a result of learning‐by‐doing like the methodology used for the National Energy Modeling System (NEMS) Electricity Market Module[5]. Learning factors are calculated separately for major design components of generating technologies to account for shared components among systems. In IEMM, capital costs of new technologies decrease faster than more established technologies because of learning factors[6].

In the IEO2019 Reference case, electricity demand in Other Non-OECD Asia grows at 2.3% per year during the projection period from 2017 to 2050. This rate is greater than the world average of 1.8% per year during the same time frame and is the fifth-highest regional rate—behind India, Africa, the Middle East, and China. This region builds new electricity generating units to meet increasing demand.

In this growth environment, new wind and solar plants are built as long as their capital and operating system costs are competitive with those of new conventional builds (the first threshold). As such, the analysis of Other Non-OECD Asia focuses on a series of cases with increasing capital costs relative to the Reference case, addressing the question: How sensitive is solar and wind generation growth to increased estimates of future wind and solar capital costs in a relatively high demand growth region?

Unlike Other Non-OECD Asia, in Other Non-OECD Europe and Eurasia in the IEO2019 Reference case, electricity demand grows modestly at a rate of 1.0% per year during the projection period, lower than the world average of 1.8% per year and the non-OECD region average of 2.4% per year. Without strong load growth in this region, new plants would displace generation from existing capacity (the second threshold).

To be economical, the cost to build, operate, and maintain a new wind or solar plant would have to be lower than the short-run marginal cost to operate an existing conventional plant (i.e., average variable operations and maintenance costs). As such, the analysis in this region is organized as a series of cases with decreasing capital costs relative to the Reference case, addressing the question: How sensitive is solar and wind technology growth to reduced estimates of future capital costs in a relatively low demand growth region?

The cases prepared for this analysis incorporate the assumptions from the IEO2019 Reference case but vary capital costs through changes in learning factors. This paper discusses nine additional cases, which can be grouped into four categories (Table 1).

| Region | Cases | Description |

|---|---|---|

| Other non-OECD Asia Other non-OECD Europe |

Reference case | Capital cost learning assumptions from the IEO2019 Reference case |

| Other non-OECD Asia Other non-OECD Europe |

Frozen Cost case | Capital costs do not decrease as a result of learning-by-doing and remain at 2017 level |

| Other non-OECD Asia | Increased Cost cases (16%, 12%, 8%, and 4%) | Capital costs are assumed higher as a result of a lesser impact of learning-by-doing. These cases have higher capital costs than the Reference case and lower capital costs than the Frozen cost. |

| Other non-OECD Europe | Decreased Cost cases (20%, 40%, and 60%) | Capital costs are assumed lower as a result of a greater impact of learning-by-doing. These cases have lower capital costs thanboththe Reference and the Frozen Cost cases. |

Analysis results

General

Across all cases, capital cost assumptions had minimal impact on end-use consumption. Through changes to electricity prices and resulting feedback from other WEPS+ modules, changes in capital cost assumptions modestly affect total primary energy consumption relative to the Reference case, varying from a 1% decrease in the Frozen Cost case to a 2% increase in the 60% Decreased Capital Cost case. Total net electricity generation, which tracks electricity demand, fluctuates minimally across the cost cases and varies similarly.

Changes in capital cost assumptions and the profile of technology-specific capacity factors that comprise the least cost generation mix result in larger effects in total installed electricity generating capacity. These effects range from an 8% decrease to a 16% increase in total installed capacity by region relative to the Reference case. Wind and solar technologies have relatively lower capacity factors than typical baseload conventional generating technologies. The highest cost case (Frozen Cost) has the least amount of total installed capacity across technologies; conversely, total installed capacity is greatest in the Decreased Cost cases.

Other Non-OECD Asia: a High Demand Growth Region

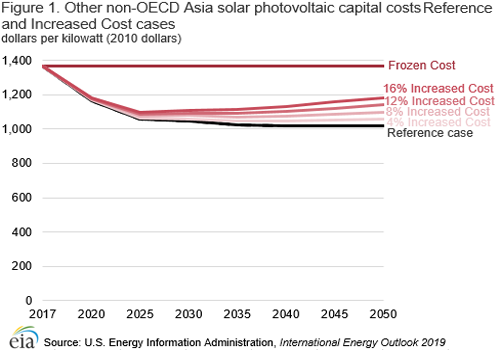

The projection period capital cost trajectories used in the IEO2019 Reference case, the Frozen Cost case, and the four Increased Cost cases (Figure 1) represent a range of capital costs where wind and solar generation technologies become less competitive in regions with substantial Reference case renewables growth.

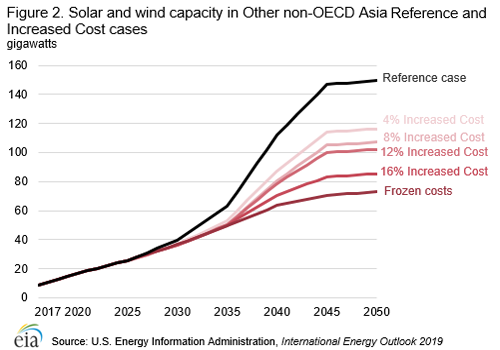

In the IEO2019 Reference case, installed solar capacity increases from 7.4 gigawatts (GW) in 2017 to 98 GW in 2050 (Figure 2), an average annual increase of 8.1%. Wind capacity also increases, from 3.2 GW in 2017 to 52 GW in 2050—a growth rate of 8.8% per year. Installations of wind capacity in the Increased Cost cases are less than the level in the Reference case (Figure 3). However, the industry will continue to build solar and wind capacity in all capital cost cases examined.

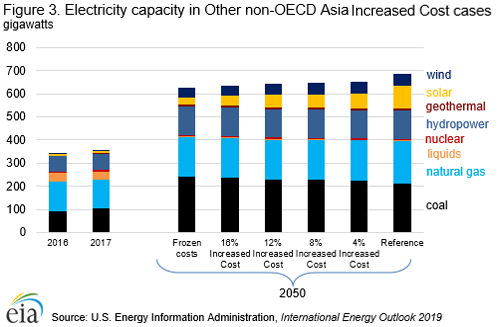

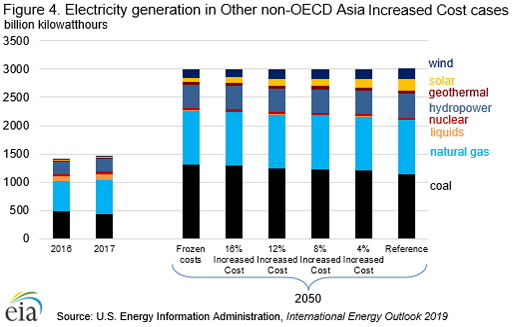

In the Frozen Cost case, which features the highest wind and solar capital costs, wind and solar technology additions are lower relative to the Reference case. More coal and natural gas generation capacity are built instead of the higher cost renewables, and coal capacity more than doubles. Coal capacity increases from 103 GW in 2017 to 242 GW in 2050, an annual growth rate of 2.6%. Likewise, coal generation increases from 446 billion kilowatthours (kWh) in 2017 to 1,314 billion kWh in 2050, an annual growth rate of 3.3%. Natural gas also sees growth in the Frozen Cost case but not at the level that coal experiences. During the projection period, natural gas capacity and generation increase at 0.9% per year and 1.4% per year, respectively (Figure 4).

In the Increased Cost cases in Other non-OECD Asia, increasing capital costs by as little as 4% makes wind and solar proportionately less competitive and less capacity is built. In 2050, solar capacity totals 64.8 GW in the 4% Increased Cost case, a 34% decrease compared with the Reference case 2050 level of 97.6 GW. Although wind and solar builds decrease in the 4% Increased Cost case relative to the Reference case, coal capacity increases 6% by 2050. Generation trends generally follow the capacity trends.

As the projected cost path for technologies increases relative to Reference case assumptions, installations decline. Electricity demand is increasingly met with coal, because of its lower relative cost, as solar and wind costs become more expensive across the Increased Cost cases. However, even with solar and wind costs remaining frozen at estimated current levels, some modest growth remains higher than policy-induced minimums. These results indicate that wind and solar generation remain largely competitive to meet growing demand even if costs do not decline as fast as projected in the Reference case.

Other Non-OECD Europe and Eurasia: a Low Demand Growth Region

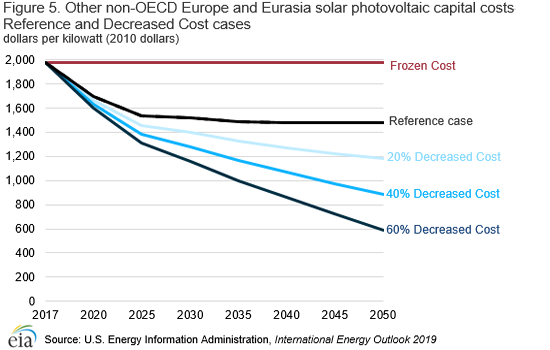

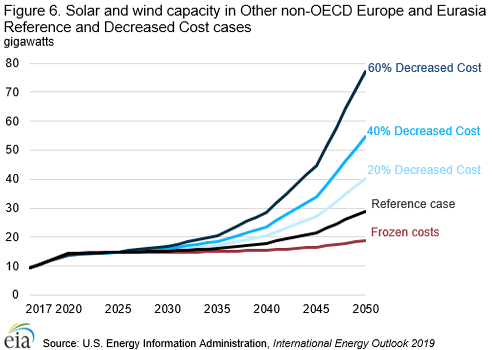

In the Decreased Cost cases, the 2017–50 capital cost trajectory used in the IEO2019 Reference case for wind and solar technologies is decreased by 20%, 40%, and 60%. Increasing the learning factor causes the capital costs to decrease at a faster rate than in the IEO2019 Reference case (Figure 5). These values represent a range of capital costs where wind and solar generation technologies start to become noticeably competitive in regions that show limited Reference case renewables growth (Figure 6).

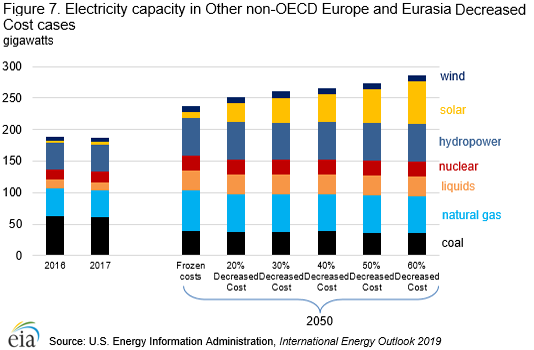

In the Reference case, installed solar capacity increases from 4.2 GW in 2017 to 20 GW in 2050, an annual growth rate of 4.8% (Figure 7). Solar capital cost reductions drive capacity increases relative to the Reference case and become noticeable starting in 2030. By 2050, in the Decreased Cost cases, solar capacity across the cases ranges from 11 GW to 48 GW (54% to 239%) greater than the Reference case.

As modeled in IEO2019, wind resources in this region are limited and are not necessarily located near the electric transmission system. Therefore, wind technologies in Other non-OECD Europe and Eurasia have a limited response to capital cost reductions. Even in the case with the steepest wind cost reduction (60% Decreased Cost), wind capacity grows modestly at 1.4% per year, totaling 9.8 GW in 2050—less than 1 GW greater than the Reference case wind capacity in 2050 at 9.1 GW (a growth rate of 1.1% per year). A 20% decrease in capital cost results in 9.5 GW of wind capacity in 2050, a 4% increase from the Reference case. Although modest, both technologies respond to decreases in capital costs and exceed Reference case levels starting with as little as a 20% decrease in capital costs.

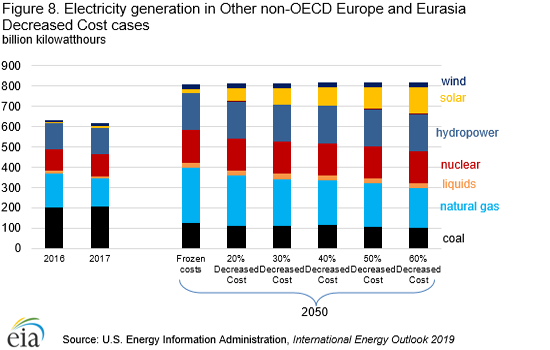

A 20% decrease in capital costs makes new wind and solar plants economically competitive with existing fossil fuel-powered plants in this region. Because the solar resource is somewhat more competitive than the wind resource for this region, decreasing wind and solar capital costs tends to shift the generation mix toward an increasing share of solar, which displaces natural gas and, to a lesser extent, coal generation. This shift is seen across all reduced cost cases. In the lowest cost reduction case (20% decrease), solar generation grows to 64 billion kWh by 2050, 51% higher than the 2050 Reference case level of 43 billion kWh. Meanwhile, coal and natural gas generation only reach 110 billion kWh and 248 billion kWh, respectively, by 2050 in the same case, a 9.4% and 2.8% decrease from the 2050 Reference case levels, respectively (Figure 8)[7].

In Other non-OECD Europe and Eurasia, renewables are not cost competitive without significant capital cost decreases as a result of three factors: affordable fossil fuel plants, weak load growth, and modest renewables policies. Although even current levels of renewable technology costs result in some growth in the amount of wind and solar generation, renewables penetration rates in regions with high demand growth and/or strong renewables policies do not appear in Other non-OECD Europe and Eurasia until technology costs decline significantly from Reference case projected levels.

Appendix A. IEO Regions

Figure A1. IEO Regions

Source: U.S. Energy Information Administration, International Energy Outlook 2019

Source: U.S. Energy Information Administration, International Energy Outlook 2019

Footnotes

- OECD is the Organization for Economic Cooperation and Development.

- Other non-OECD Asia includes countries in non_OECD Asia other than China and India, including Indonesia, Thailand, Vietnam, Malaysia, etc. Other non-OECD Europe and Asia includes countries in non-OECD Europe and Eurasia including Ukraine, Bulgaria, Armenia, Romania, etc. Full regional definitions used in the IEO appear in Appendix A.

- For more information see the International Electricity Market Model Fact Sheet.

- For more information see the World Energy Projection System Plus Overview.

- For a more detailed description, see U.S. Energy Information Administration, NEMS Component Design Report Modeling Technology Penetration (Washington, DC, March 1993).

- Learning factors do not directly correlate to the reductions in cost (i.e. a 4% reduction in learning-by-doing is typically not equivalent to a 4% increase in cost). Changes in learning factors may not produce linear changes in costs.

- Because electricity demand, and hence total generation, is relatively flat across the cases, capacity increases between cases result from the increased solar penetration over natural gas technologies, which have higher capacity factors and require less capacity for the same levels of generation. Depressed growth in this region’s electricity demand further demonstrates the relative insensitivity of electricity demand as a result of decreases in solar and wind capital costs.