In the News:

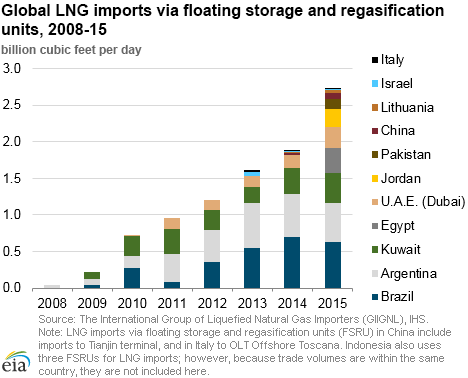

Global LNG imports using floating storage and regasification units increase 46% in 2015 over 2014 levels

Earlier this month, Pakistan announced plans to build infrastructure for a second floating storage and regasification unit (FSRU) to import liquefied natural gas (LNG), doubling its current regasification capacity. Pakistan is one of several countries that experienced strong growth in natural gas demand in recent years, primarily for gas-fired electric generation, and have limited options to import natural gas by pipeline or produce it domestically. FSRU technology allows a flexible, cost-effective, and relatively quick way to import LNG to address supply shortages. In 2015, global imports of LNG using FSRU increased by 46% as compared to 2014, primarily as a result of three new countries that began LNG imports via FSRU—Egypt, Pakistan, and Jordan.

FSRU technology is increasingly used worldwide, particularly in smaller, emerging markets that have either supply shortages or a highly seasonal demand. FSRU typically involves a specialized vessel, which is capable of transporting, storing, and regasifying LNG onboard. Currently, there are 24 operating FSRU vessels: 18 are moored in ports worldwide on a short-term basis and can be relocated if a country's demand requirements change, three are engaged in LNG trade, and three are permanently moored. Seven more FSRUs are currently under construction, with expected delivery dates in 2016-18, according to the International Group of Liquefied Natural Gas Importers (GIIGNL).

Global LNG imports received by FSRU terminals in 2015 amounted to 2.7 billion cubic feet per day (Bcf/d) and accounted for 8% of global LNG imports, according to EIA's calculations based on GIIGNL data. In 2015, FSRUs represented 9% of the global regasification capacity, based on data by the International Gas Union. Three new importers in 2015—Pakistan, Jordan, and Egypt—have collectively imported 0.7 Bcf/d, accounting for 27% of the total imports using FSRUs and 85% of the year-on-year increase in FSRU imports. Two more countries are expected to begin imports using FSRUs this year: Ghana and Colombia. In its recently released International Energy Outlook, EIA assumed that in 2017-18, several other countries will add FSRUs, including Uruguay, Chile, Puerto Rico, Bangladesh, India, and Russia, increasing total global FSRU capacity to 13.5 Bcf/d.

Overview:

(For the Week Ending Wednesday, June 15, 2016)

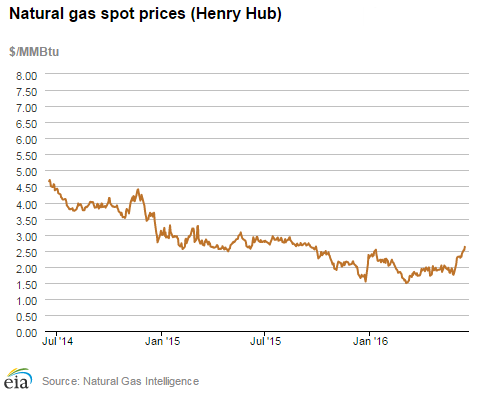

- Outside of the West Coast and Northeast, natural gas spot prices rose at most market locations this report week (Wednesday, June 8, to Wednesday, June 15) The Henry Hub spot price continued its recent increases, rising by 29¢ from $2.33 per million British thermal unit (MMBtu) last Wednesday to $2.62/MMBtu yesterday.

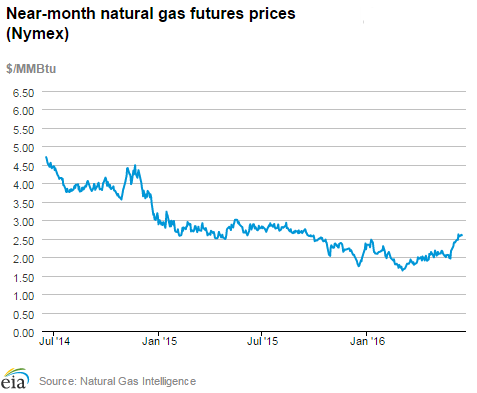

- At the New York Mercantile Exchange (Nymex), the July 2016 contract rose from $2.468/MMBtu last Wednesday to $2.595/MMBtu yesterday, an increase of about 13¢.

- Net injections to working gas totaled 69 billion cubic feet (Bcf) for the week ending June 10. Working gas stocks are 3,041 Bcf, which is 26% above the year-ago level and 30% above the five-year (2011-15) average for this week.

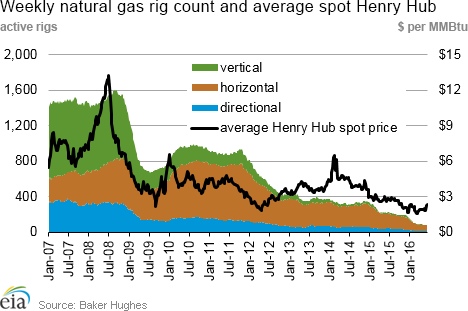

- According to Baker Hughes, for the week ending June 10, the natural gas rig count increased by 3 to 85. Oil-directed rigs increased by 3 to 328. This is the second consecutive weekly increase in the oil rig count. The total rig count increased by 6 over the week.

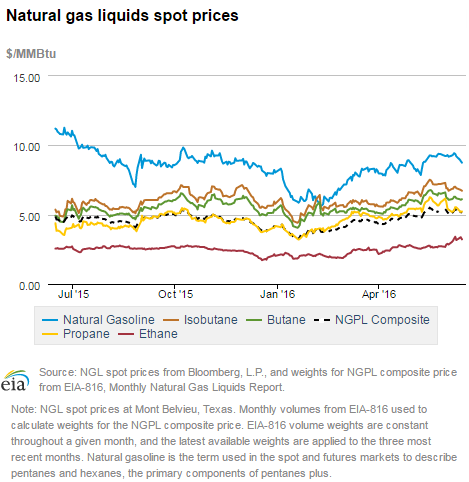

- The natural gas plant liquids composite price at Mont Belvieu, Texas, rose by 2¢, closing at $5.26/MMBtu for the week ending Friday, June 10. The price of natural gasoline and ethane rose 1% and 14%, respectively. These increases were offset by declines in the other plants liquids. Butane prices fell by 1%, and propane prices fell by 6%. Isobutane prices remained essentially flat.

Prices/Supply/Demand:

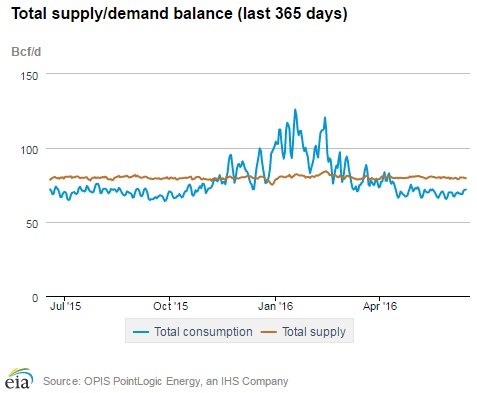

Spot prices rise across the board. The Henry Hub spot price increased again this week, for the third week in a row, rising by 29¢, from $2.33/MMBtu last Wednesday to $2.62/MMBtu yesterday, its highest level since September 2015. Prices around the country saw similar increases. At the Chicago Citygate, prices increased by 27¢ from the previous report week and closed at $2.53/MMBtu yesterday. On the West Coast, the PG&E Citygate price in California rose by 15¢, from $2.37/MMBtu to $2.52/MMBtu. Prices likely rose in response to warmer temperatures and increases in consumption of natural gas for power generation. Additionally, PointLogic Energy data indicate that dry gas production this week was lower year-over-year. This decline in production may be supporting price increases as well.

Northeast prices post gains this week. Prices in major northeastern market areas also rose during the report period. At the Algonquin Citygate, which serves Boston-area consumers, prices rose 22¢ from $1.93/MMBtu to $2.15/MMBtu, Wednesday to Wednesday. At the Transcontinental Pipeline's Zone 6 trading point for New York, prices rose 19¢ from $1.66 last Wednesday to $1.85/MMBtu yesterday.

Marcellus prices tick up. Marcellus-area prices increased over the week, but generally by a lesser amount than other major price points. The Tennessee Zone 4 Marcellus price rose 7¢ from $1.54/MMBtu last Wednesday to $1.61/MMBtu yesterday. The price at Dominion South in northwest Pennsylvania rose by 10¢, ending the week at $1.72/MMBtu. Marcellus prices still trade at a discount to the major Northeast market areas of New York and Boston, but the differential has narrowed in recent months.

Nymex prices increase. At the Nymex, the July 2016 contract rose from $2.468/MMBtu last Wednesday to $2.595/MMBtu yesterday, an increase of about 13¢. The 12-month strip, which averages the July 2016 through June 2017 futures contracts, rose 3¢ from last Wednesday, closing yesterday at $2.923/MMBtu.

Production flat but imports rise. According to data from PointLogic, average total supply for the report period rose by 1% this report week. This was driven by a 9% increase in imports from Canada, which averaged 6.8 billion cubic feet (Bcf) this week. Dry production was flat at 80.6 Bcf/d.

Consumption increases. Average consumption for the report week rose 2% according to data from PointLogic. This increase was driven by a 5% increase in consumption of natural gas for electric power generation. Power burn this week was 4% greater than year-ago levels. In the residential and commercial sectors, consumption fell by 2%. Industrial consumption and exports to Mexico both fell by 1%.

U.S. liquefied natural gas (LNG) exports. The natural gas pipeline flows to the Sabine Pass liquefaction terminal averaged 0.6 Bcf/d, 12% higher than receipts last week. Two vessels (LNG-carrying capacity 3.5 Bcf and 3.6 Bcf) departed the terminal on June 10 and 13.

Storage:

Working gas stocks climb past 3,000 Bcf earlier than usual. Working gas in the Lower 48 states posted its ninth straight week of net injections. Net injections into storage totaled 69 Bcf during the storage report week, compared with the five-year (2011-15) average of 87 Bcf and last year's net injection of 96 Bcf during the same week. As a result, the surplus in storage compared with the five-year average declined from the previous week to 704 Bcf, and the surplus compared with year-ago levels decreased to 633 Bcf. The year-over-year storage surplus fell for the tenth consecutive week. This report marks the earliest week that working gas stocks surpassed the 3,000 Bcf threshold, which typically isn't reached until mid-August or early September.

The 2016 refill season shows stocks well ahead of recent injection seasons. Despite injections smaller than in previous years, working gas stocks remain near record highs for this time of year. Working gas stocks as of last Friday were 79 Bcf above the previous five-year (2011-15) maximum for this time of year of 2,962 Bcf, which occurred in 2012. Cumulative net injections into working gas total 561 Bcf thus far in the 2016 refill season, compared with the five-year average of 731 Bcf and last year's tally of 936 Bcf during the same period. Although cumulative net injections into working gas this year are significantly below historical levels, they remain ahead of the pace set in 2012, when they totaled 488 Bcf the last time working gas stocks were this high at this point in the 2012 refill season.

The January futures price premium over the current spot price falls below $1. During the most recent storage week, the average natural gas spot price at the Henry Hub was $2.31/MMBtu, while the Nymex futures price of natural gas for delivery in January 2017 averaged $3.23/MMBtu, a difference of 92¢/MMBtu. This marks the first time in eight weeks that the January futures contract premium over the spot price was less than $1. A year ago, the premium was 52¢/MMBtu. Despite falling below a $1 differential, the higher value than a year ago suggests there is more financial incentive this year to buy and store natural gas in the summer for sale in the winter. The average Henry Hub price so far in the injection season this year, from April 1 to June 10, was $1.97/MMBtu, 27% lower than the average value of $2.70/MMBtu for the same period last year.

Stock change is within the range of expectations. Expected net injections for the week generally ranged from 57 to 70 Bcf, with a median of 65 Bcf. Prices for the Nymex futures contract for July delivery at the Henry Hub fell about 1¢/MMBtu, with 306 contracts traded at the release. Prices continued to fall in subsequent trading, reaching $2.58/MMBtu within two minutes of EIA's Weekly Natural Gas Storage Report (WNGSR) release.

Rising temperatures boost cooling demand for natural gas. Temperatures in the Lower 48 states averaged 71°F during the storage report week, falling 1% from the previous week. Temperatures during the report week were 4% above normal and about equal to last year at this time. Cooling degree-days (CDD) in the Lower 48 states totaled 51.

See also:

| Spot Prices ($/MMBtu) | Thu, 09-Jun |

Fri, 10-Jun |

Mon, 13-Jun |

Tue, 14-Jun |

Wed, 15-Jun |

|---|---|---|---|---|---|

| Henry Hub |

2.31 |

2.41 |

2.52 |

2.52 |

2.62 |

| New York |

1.55 |

1.62 |

1.74 |

1.85 |

1.85 |

| Chicago |

2.25 |

2.37 |

2.47 |

2.47 |

2.53 |

| Cal. Comp. Avg.* |

2.23 |

2.24 |

2.34 |

2.33 |

2.39 |

| Futures ($/MMBtu) | |||||

| July contract |

2.617 |

2.556 |

2.585 |

2.604 |

2.595 |

| August contract |

2.690 |

2.624 |

2.652 |

2.666 |

2.652 |

| *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. natural gas supply - Gas week: (6/9/16 - 6/15/16) | |||

|---|---|---|---|

Average daily values (Bcf/d): |

|||

this week |

last week |

last year |

|

| Marketed production | 80.6 |

80.7 |

81.0 |

| Dry production | 72.9 |

72.9 |

73.1 |

| Net Canada imports | 6.8 |

6.1 |

5.9 |

| LNG pipeline deliveries | 0.2 |

0.2 |

0.2 |

| Total supply | 79.9 |

79.2 |

79.2 |

|

Source: OPIS PointLogic Energy, an IHS Company | |||

| U.S. natural gas consumption - Gas week: (6/9/16 - 6/15/16) | |||

|---|---|---|---|

Average daily values (Bcf/d): |

|||

this week |

last week |

last year |

|

| U.S. consumption | 59.4 |

58.4 |

58.7 |

| Power | 31.6 |

30.3 |

30.5 |

| Industrial | 19.5 |

19.6 |

19.4 |

| Residential/commercial | 8.4 |

8.5 |

8.8 |

| Mexico exports | 3.6 |

3.5 |

3.0 |

| Pipeloss fuel use/losses | 6.6 |

6.5 |

6.5 |

| LNG pipeline receipts | 0.6 |

0.5 |

- |

| Total demand | 70.2 |

68.9 |

68.2 |

|

Source: OPIS PointLogic Energy, an IHS Company | |||

| Rigs | |||

|---|---|---|---|

Fri, June 10, 2016 |

Change from |

||

last week |

last year |

||

| Oil rigs | 328 |

0.9% |

-48.3% |

| Natural gas rigs | 85 |

3.7% |

-61.5% |

| Miscellaneous | 1 |

0.0% |

-66.7% |

| Rig numbers by type | |||

|---|---|---|---|

Fri, June 10, 2016 |

Change from |

||

last week |

last year |

||

| Vertical | 46 |

2.2% |

-54.5% |

| Horizontal | 323 |

1.3% |

-51.3% |

| Directional | 45 |

2.3% |

-52.6% |

| Source: Baker Hughes Inc. | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2016-06-10 |

2016-06-03 |

change |

|

| East | 585 |

559 |

26 |

|

| Midwest | 703 |

679 |

24 |

|

| Mountain | 188 |

183 |

5 |

|

| Pacific | 312 |

307 |

5 |

|

| South Central | 1,253 |

1,244 |

9 |

|

| Total | 3,041 |

2,972 |

69 |

|

| Source: U.S. Energy Information Administration | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (6/10/15) |

5-year average (2011-2015) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 491 |

19.1 |

517 |

13.2 |

|

| Midwest | 485 |

44.9 |

519 |

35.5 |

|

| Mountain | 146 |

28.8 |

135 |

39.3 |

|

| Pacific | 326 |

-4.3 |

280 |

11.4 |

|

| South Central | 962 |

30.2 |

885 |

41.6 |

|

| Total | 2,408 |

26.3 |

2,337 |

30.1 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- heating & cooling degree days (week ending Jun 09) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 13

|

-11

|

-18

|

14

|

7

|

9

|

||

| Middle Atlantic | 10

|

-6

|

-4

|

26

|

9

|

12

|

||

| E N Central | 17

|

-4

|

9

|

17

|

-9

|

-12

|

||

| W N Central | 12

|

-6

|

9

|

34

|

0

|

-22

|

||

| South Atlantic | 1

|

-4

|

-2

|

84

|

21

|

14

|

||

| E S Central | 1

|

-3

|

1

|

68

|

11

|

-5

|

||

| W S Central | 0

|

0

|

0

|

83

|

-5

|

-23

|

||

| Mountain | 3

|

-28

|

-6

|

77

|

36

|

34

|

||

| Pacific | 1

|

-21

|

-2

|

47

|

30

|

18

|

||

| United States | 8

|

-9

|

1

|

51

|

11

|

3

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Jun 09, 2016

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Jun 09, 2016

Source: NOAA/National Weather Service