In the News:

Near-month futures contract indicates expectations of rising prices

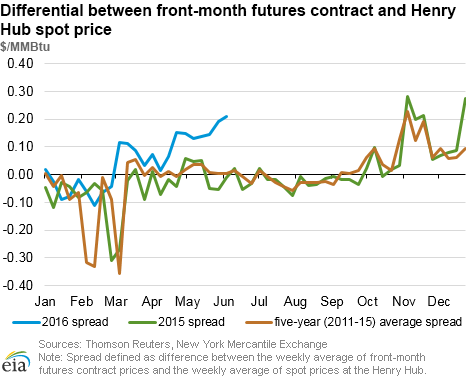

Heading into the summer cooling season, the New York Mercantile Exchange (Nymex) natural gas contract for July has markedly exceeded Henry Hub spot prices, likely reflecting expectations for summer natural gas consumption to increase substantially from current levels. On May 27, the first day the July contract was trading in the front-month position, futures closed at $2.169 per million British thermal unit (MMBtu). This was more than 20¢/MMBtu higher than the expired June contract–an uncommonly high change for a contract rollover at this time of year (in 2015, there was a 9¢/MMBtu drop in the futures contract when the June contract expired). Both spot and futures prices have risen substantially through early June, with the Nymex contract for July averaging $2.432/MMBtu as of June 8, 13¢/MMBtu higher than the average Henry Hub spot price for the same period.

In general, the spread between the front-month futures contract and current spot prices has historically been slightly positive going into summer, as natural gas heating demand evaporates. The five-year (2011-15) weekly spread has been less than 5¢/MMBtu throughout April and May. But this year, the weekly average futures contract has been higher than the weekly average Henry Hub spot price by more than 10¢/MMBtu since late April. Based on the five-year average, this magnitude of futures/spot price spread has traditionally been more common in November, at the beginning of the heating season.

This above-normal differential occurs as increased construction of gas-fired power plants–driven in part by low natural gas prices–is forecast to lead to an annual record high for natural gas power burn in 2016. Additionally, EIA's Short-Term Energy Outlook forecasts relatively flat natural gas production through late 2016, raising prospects of a tighter domestic natural gas market in the near term. Although high underground storage inventories have placed downward pressure on spot prices, the rate of injection into storage has remained below last year. Working stocks in underground storage were 69% above year-ago levels on April 1, the beginning of the cooling season, but this surplus has narrowed to 29% as of June 3. If natural gas production fails to rise along with demand, gas prices may continue to increase as the summer heats up.

Overview:

(For the Week Ending Wednesday, June 8, 2016)

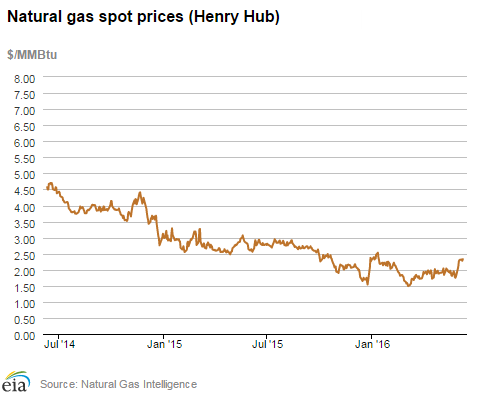

- Outside of the West Coast and Northeast, natural gas spot prices rose at most market locations this report week (Wednesday, June 1, to Wednesday, June 8). The Henry Hub spot price rose by 7¢, from $2.26/MMBtu last Wednesday to $2.33/MMBtu yesterday.

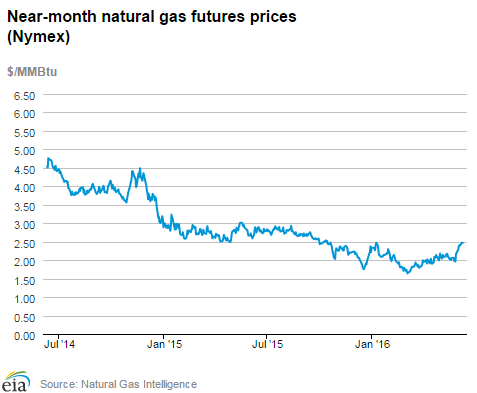

- At the Nymex, the July 2016 contract rose from $2.381/MMBtu last Wednesday to $2.468/MMBtu yesterday, an increase of about 9¢.

- Net injections to working gas totaled 65 billion cubic feet (Bcf) for the week ending June 3. Working gas stocks are 2,972 Bcf, which is 29% above the year-ago level and 32% above the five-year (2011-15) average for this week.

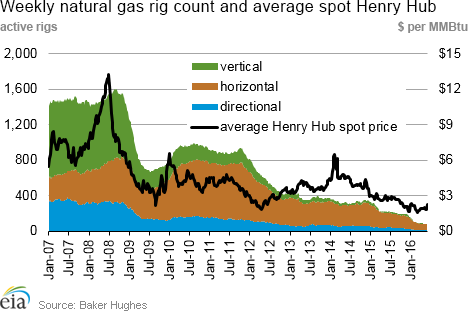

- According to Baker Hughes, for the week ending June 3, the natural gas rig count decreased by 5 to 87. Oil-directed rigs increased by 9 to 325. This is the largest increase in the oil rig count in almost six months, possibly related to the steadily rising crude oil price, which is now close to $50 per barrel. Just six months ago, the crude price reached as low as the mid-$20s per barrel. The total rig count on June 3 increased by four.

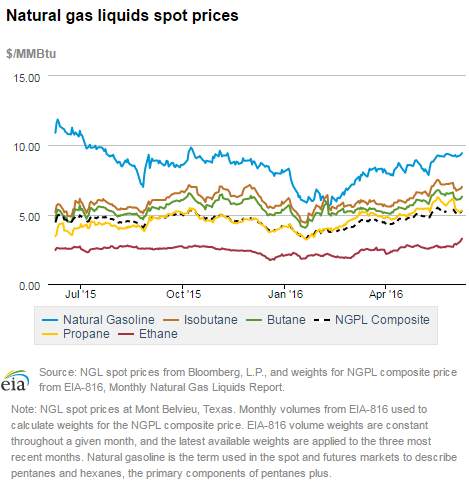

- The natural gas plant liquids composite price at Mont Belvieu, Texas, was essentially flat, closing at $5.24/MMBtu for the week ending Friday, June 3. The prices of propane and natural gasoline each fell by less than 1%. Butane and isobutane prices both fell by more than 3%, and the ethane price increased by nearly 5%.

Prices/Supply/Demand:

Spot prices mixed, but generally rising with temperatures. The Henry Hub spot price increased again this week, rising by 7¢, from $2.26 per MMBtu last Wednesday to $2.33/MMBtu yesterday. Prices at other market locations outside of the West Coast and Northeast saw similar increases, as home cooling demand rose slightly, pushing up natural gas-fired electricity generation. At the Chicago Citygate, prices maintained their gains from the prior report week, increasing by 2¢ over the report week and closing at $2.26/MMBtu yesterday.

On the West Coast, by contrast, the PG&E Citygate price in California fell slightly, from $2.40/MMBtu to $2.37/MMBtu. This may be related to the current low price of pipeline imports from Canada, stemming from mild early-summer weather, high natural gas storage stocks in Canada, and recent wildfires that reduced natural gas consumed in oil sands production and curtailed operation of certain pipelines.

Prices at import points down. Warmer weather along the northern border is reducing home heating demand in both the United States and Canada. Prices at western import points fell substantially this week, and are well below the Henry Hub price. The Northwest Sumas price, which reflects the price of imported gas into northwest Washington, fell from $1.89/MMBtu to $1.59/MMBtu over the report week. Similarly, the price at Kingsgate, which reflects the price of imported gas into Idaho, fell from $2.06/MMBtu to $1.87/MMBtu.

Northeast prices flat to down. Prices in major northeastern market areas fell for the report period, with most of the decrease occurring yesterday. At the Algonquin Citygate, which serves Boston-area consumers, prices fell from $2.01/MMBtu to $1.93/MMBtu, Wednesday to Wednesday. At the Transcontinental Pipeline's Zone 6 trading point for New York, prices fell from $1.71 last Wednesday to $1.66/MMBtu yesterday.

Marcellus prices rise. Marcellus-area prices increased over the week, and are gradually starting to converge with other Northeast prices. The Tennessee Zone 4 Marcellus price rose from $1.42/MMBtu last Wednesday to $1.54/MMBtu yesterday. The price at Dominion South in northwest Pennsylvania rose by 7¢, ending the week at $1.62/MMBtu.

Nymex prices rise. At the Nymex, the July 2016 contract rose from $2.381/MMBtu last Wednesday to $2.468/MMBtu yesterday, an increase of about 9¢. The 12-month strip, which averages the July 2016 through June 2017 futures contracts, rose 10¢ to $2.897/MMBtu yesterday. This is the highest the 12-month strip has been all year. In 2015, it exceeded $3.00/MMBtu for many trading days.

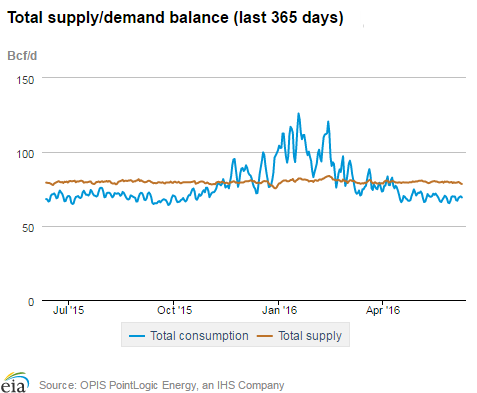

Supply is relatively unchanged. According to data from PointLogic, average total supply for the report period remained flat again this report week. This was driven by little change in dry natural gas production, which averaged 72.9 billion cubic feet per day (Bcf/d) for the week. Net imports from Canada rose 5% and accounted for 6.2 Bcf/d of supply.

Consumption increases slightly. Average consumption for the report week ticked upward slightly, rising 1% according to data from PointLogic, driven by a minor increase in electric-sector gas consumption. Consumption of natural gas for power generation rose 2% week over week, while residential/commercial consumption increased by just over 1%. Industrial consumption remained flat and exports to Mexico rose 3%.

U.S. liquefied natural gas (LNG) exports. According to PointLogic, natural gas pipeline flows to the Sabine Pass liquefaction terminal averaged 0.54 Bcf/d this week, 1% lower than receipts last week. One vessel (with a LNG-carrying capacity of 3.4 Bcf) departed the Sabine Pass terminal on June 3, and one vessel (with LNG-carrying capacity of 3.5 Bcf) is scheduled to dock at the terminal today. A total of three cargoes were exported from the terminal in May.

Storage:

Working gas stocks continue to climb. Working gas in the Lower 48 states posted its eighth straight week of net injections. Net injections into storage totaled 65 Bcf during the storage report week, compared with the five-year (2011-15) average of 96 Bcf and last year's net injection of 117 Bcf during the same week. As a result, the surplus in storage compared with the five-year average declined from the previous week to 722 Bcf, and the surplus compared with year-ago levels decreased to 660 Bcf. The year-over-year storage surplus fell for the ninth consecutive week.

The 2016 refill season shows stocks well ahead of recent injection seasons. Despite a slow start to the refill season, working gas stocks remain near record-highs for this time of year. Working gas stocks as of last Friday were 76 Bcf above the previous five-year (2011-15) maximum for this time of year of 2,896, which occurred in 2012. Cumulative net injections into working gas total 492 Bcf thus far in the 2016 refill season, compared with the five-year average of 644 Bcf and last year's tally of 840 Bcf during the same period. Cumulative net injections totaled 422 Bcf at this point in the 2012 refill season.

January futures price continues to trade at more than $1 above current spot price. During the most recent storage week, the average natural gas spot price at the Henry Hub was $2.11/MMBtu, while the Nymex futures price of natural gas for delivery in January 2017 averaged $3.13/MMBtu, a difference of $1.02/MMBtu. A year ago, the premium was 50¢/MMBtu, suggesting there is more financial incentive this year to buy and store natural gas in the summer for sale in the winter. The average Henry Hub price so far in the injection season this year, from April 1 through the end of the storage week, was $1.93/MMBtu, 29% lower than the average value of $2.70/MMBtu for the same period last year.

Stock change is well below range of expectations. Expected net injections for the week generally ranged from 72 to 91 Bcf, with a median of 76 Bcf. Prices for the Nymex futures contract for July delivery at the Henry Hub gained more than 2¢/MMBtu in vigorous trading, with 1,695 contracts traded at the release. Prices continued to climb in subsequent trading, reaching $2.55/MMBtu–more than 8¢/MMBtu above the pre-release price–within two minutes of the U.S. EIA's Weekly Natural Gas Storage Report (WNGSR) release. The significant divergence between market expectations and EIA's report likely contributed to the robust trading activity.

Rising temperatures boost cooling demand for natural gas. Temperatures in the Lower 48 states averaged 72°F during the storage report week, increasing 10% above the previous week. Temperatures during the report week were 7% above normal and 6% above last year at this time. Cooling degree-days (CDD) in the Lower 48 states hit its highest level since the beginning of 2016, totaling 52 CDD. Temperatures in the South Atlantic, East South Central, and West South Central U.S. Census divisions, where natural gas is a key energy source for electric generation, averaged 76°F.

See also:

| Spot Prices ($/MMBtu) | Thu, 02-Jun |

Fri, 03-Jun |

Mon, 06-Jun |

Tue, 07-Jun |

Wed, 08-Jun |

|---|---|---|---|---|---|

| Henry Hub |

2.30 |

2.31 |

2.32 |

2.28 |

2.33 |

| New York |

1.83 |

1.65 |

1.89 |

1.71 |

1.66 |

| Chicago |

2.19 |

2.20 |

2.23 |

2.23 |

2.26 |

| Cal. Comp. Avg.* |

2.31 |

2.23 |

2.25 |

2.22 |

2.26 |

| Futures ($/MMBtu) | |||||

| July contract |

2.405 |

2.398 |

2.466 |

2.474 |

2.468 |

| August contract |

2.482 |

2.476 |

2.537 |

2.557 |

2.544 |

| *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. natural gas supply - Gas week: (6/2/16 - 6/8/16) | |||

|---|---|---|---|

Average daily values (Bcf/d): |

|||

this week |

last week |

last year |

|

| Marketed production | 80.7 |

81.4 |

82.0 |

| Dry production | 72.9 |

73.5 |

73.9 |

| Net Canada imports | 6.1 |

5.9 |

5.7 |

| LNG pipeline deliveries | 0.2 |

0.2 |

0.2 |

| Total supply | 79.2 |

79.6 |

79.9 |

|

Source: OPIS PointLogic Energy, an IHS Company | |||

| U.S. natural gas consumption - Gas week: (6/2/16 - 6/8/16) | |||

|---|---|---|---|

Average daily values (Bcf/d): |

|||

this week |

last week |

last year |

|

| U.S. consumption | 58.4 |

57.6 |

56.0 |

| Power | 30.3 |

29.6 |

25.6 |

| Industrial | 19.6 |

19.6 |

19.6 |

| Residential/commercial | 8.5 |

8.4 |

10.8 |

| Mexico exports | 3.5 |

3.4 |

2.9 |

| Pipeloss fuel use/losses | 6.5 |

6.5 |

6.2 |

| LNG pipeline receipts | 0.5 |

0.5 |

- |

| Total demand | 68.9 |

68.1 |

65.1 |

|

Source: OPIS PointLogic Energy, an IHS Company | |||

| Rigs | |||

|---|---|---|---|

Fri, June 03, 2016 |

Change from |

||

last week |

last year |

||

| Oil rigs | 325 |

2.8% |

-49.4% |

| Natural gas rigs | 82 |

-5.7% |

-63.1% |

| Miscellaneous | 1 |

0.0% |

-75.0% |

| Rig numbers by type | |||

|---|---|---|---|

Fri, June 03, 2016 |

Change from |

||

last week |

last year |

||

| Vertical | 45 |

-2.2% |

-54.5% |

| Horizontal | 319 |

1.6% |

-52.6% |

| Directional | 44 |

0.0% |

-54.2% |

| Source: Baker Hughes Inc. | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2016-06-03 |

2016-05-27 |

change |

|

| East | 559 |

537 |

22 |

|

| Midwest | 679 |

655 |

24 |

|

| Mountain | 183 |

178 |

5 |

|

| Pacific | 307 |

304 |

3 |

|

| South Central | 1,244 |

1,233 |

11 |

|

| Total | 2,972 |

2,907 |

65 |

|

| Source: U.S. Energy Information Administration | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (6/3/15) |

5-year average (2011-2015) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 461 |

21.3 |

490 |

14.1 |

|

| Midwest | 455 |

49.2 |

492 |

38.0 |

|

| Mountain | 140 |

30.7 |

131 |

39.7 |

|

| Pacific | 320 |

-4.1 |

271 |

13.3 |

|

| South Central | 936 |

32.9 |

867 |

43.5 |

|

| Total | 2,312 |

28.5 |

2,250 |

32.1 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- heating & cooling degree days (week ending Jun 02) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 5

|

-28

|

-38

|

26

|

22

|

11

|

||

| Middle Atlantic | 0

|

-24

|

-24

|

57

|

45

|

32

|

||

| E N Central | 2

|

-28

|

-35

|

50

|

30

|

34

|

||

| W N Central | 12

|

-14

|

-20

|

30

|

3

|

17

|

||

| South Atlantic | 0

|

-9

|

-3

|

78

|

22

|

6

|

||

| E S Central | 0

|

-8

|

-5

|

76

|

28

|

25

|

||

| W S Central | 0

|

-1

|

-2

|

75

|

-3

|

5

|

||

| Mountain | 35

|

-3

|

15

|

30

|

-4

|

-13

|

||

| Pacific | 7

|

-19

|

3

|

20

|

6

|

7

|

||

| United States | 5

|

-17

|

-14

|

52

|

18

|

15

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Jun 02, 2016

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Jun 02, 2016

Source: NOAA/National Weather Service