In the News:

New gas-fired power plants are concentrated near major shale plays

In 2015, a combination of low natural gas prices, increases in gas-fired generation capacity, and coal power plant retirements led to a 19% annual increase in gas-fired power generation, with the gas share of total generation increasing from 28% in 2014 to 33% in 2015. The April 2016 Short-Term Energy Outlook forecasts that this year, for the first time, natural gas-fired generation will exceed coal generation in the United States on an annual basis. Growth in gas-fired generation capacity is expected to continue over the next several years as 18.7 gigawatts (GW) of capacity, completed in 2016 or currently under construction, comes online between 2016 and 2018. This represents a 4% increase over the gas-fired capacity level at the end of 2015.

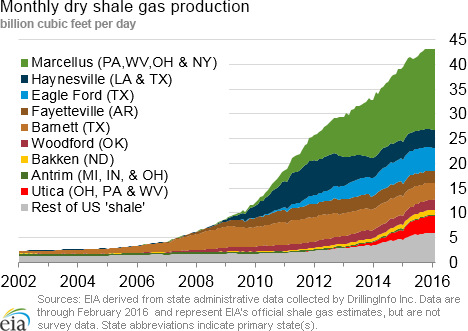

Many of these additions are concentrated around the prolific Marcellus and Utica shale region, largely located in Pennsylvania, West Virginia, and Ohio, which have been leading the growth in U.S. natural gas production over the past several years. Among the states in relatively close proximity to the Marcellus and Utica, Virginia will account for the largest cumulative additions of gas-fired capacity over the 2016-18 period, with 2.3 GW of gas-fired capacity under construction, followed by Ohio with 1.9 GW, Pennsylvania with 1.8 GW, and Massachusetts with 0.7 GW, according to EIA's Electric Power Monthly.

Natural gas production from the Eagle Ford and Haynesville shale resources, located in Texas and Louisiana, has also grown, and there are notable levels of gas-fired capacity under construction in those areas. Texas has the second largest cumulative additions of gas-fired capacity, at 3.2 GW over the 2016-18 period, with neighboring Louisiana at 0.8 GW. In addition for the same period, Texas far exceeds the other states in planned gas-fired capacity with received and pending permits to construct 6.6 GW (cumulatively) over 2016-18.

New gas-fired capacity additions, particularly those located around Marcellus and Utica shales, are being built in part to replace retired coal generation capacity. Since 2015, after the Environmental Protection Agency's Mercury and Air Toxics Standards rules went into effect, more than 18 GW of electric generating capacity was retired, of which coal plant retirements accounted for more than 80%. Almost one half of retired coal capacity was located in Ohio, Georgia, and Kentucky, while other states with traditionally high levels of coal-fired electricity generation, such as Virginia, West Virginia, and Indiana, each retired at least one GW of coal capacity in 2015.

Florida has the largest cumulative additions of gas-fired capacity, at 3.8 GW in 2016-18. This expansion is driven by retirements of older less efficient coal units, and replacement and modernization of oil-fired capacity.

Overview:

(For the Week Ending Wednesday, April 6, 2016)

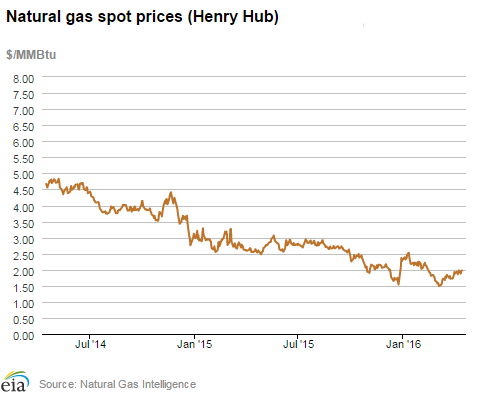

- Natural gas spot prices increased at most locations this report week (Wednesday, April 6, to Wednesday, April 13). The Henry Hub spot price rose during the report week from $1.86 per million British thermal units (MMBtu) to $1.98/MMBtu yesterday.

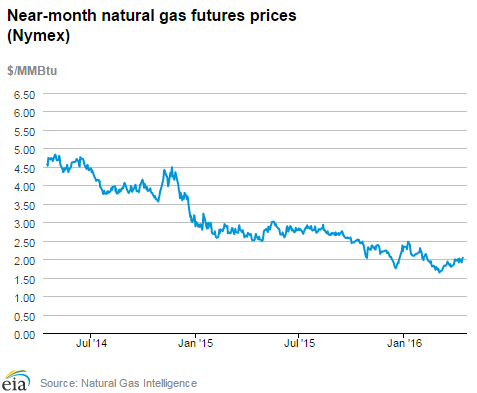

- At the New York Mercantile Exchange (Nymex), the May 2016 contract rose over the report week from $1.911/MMBtu last Wednesday to $2.036/MMBtu yesterday.

- Net withdrawals from working gas totaled 3 billion cubic feet (Bcf) for the week ending April 8. Working gas stocks are 2,477 Bcf, which is 62.9% above the year-ago level and 52.1% above the five-year (2011-15) average for this week.

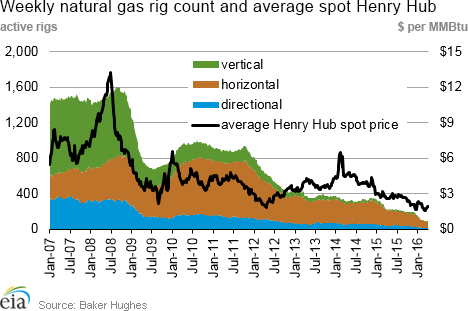

- For the week ending April 8, the natural gas rig count rose by 1 to 89, according to Baker Hughes data, and oil-directed rigs fell by 8, to 354. The total rig count fell by 7, and now stands at 443.

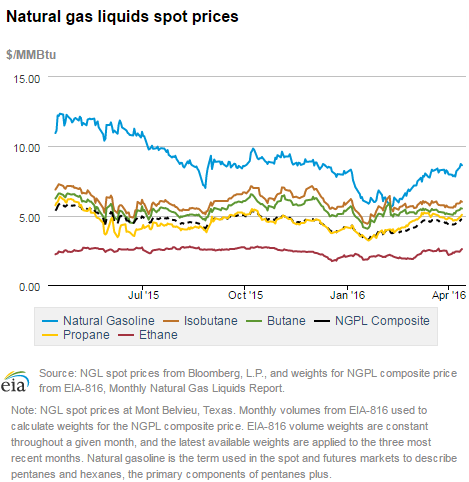

- The natural gas plant liquids (NGPL) composite price at Mont Belvieu, Texas, decreased by 1.6% to $4.39/MMBtu for the week ending Friday, April 8. The prices of ethane, propane, and natural gasoline fell by 1.2%, 2.3%, and 2.6%, respectively. The price of butane rose 0.3%, and isobutane remained flat week over week.

Prices/Demand/Supply:

Despite cooler weather in the East, many prices remain below $2/MMBtu. Compared to the previous report period, weather for this week was slightly colder than normal east of the Rockies. The Henry Hub spot price rose from $1.86/MMBtu to $1.98/MMBtu Wednesday to Wednesday. At the Chicago Citygate, prices remained flat Wednesday to Wednesday at $1.92/MMBtu. On the West Coast, temperatures were somewhat warmer than normal, but still mild. At the PG&E Citygate in California, the spot price rose from $1.91/MMBtu last Wednesday to $1.97/MMBtu yesterday.

Northeast prices mixed. At the Algonquin Citygate, which serves Boston-area consumers, prices rose week over week from $2.52/MMBtu last Wednesday to $3.57/MMBtu yesterday. Because of maintenance on its system, Algonquin restricted interruptible transportation this week, limiting nominations to maintain system integrity. Prices at Transcontinental Pipeline's Zone 6 trading point for New York, on the other hand, fell this week from $1.84/MMBtu to $1.65/MMBtu.

Marcellus prices slightly down to flat. At Dominion South in northwest Pennsylvania, prices remained flat at $1.47/MMBtu week over week. The Tennessee Zone 4 Marcellus price barely moved from $1.44/MMBtu last Wednesday to $1.41/MMBtu yesterday. Marcellus prices remain at a substantial discount to Henry Hub, but the spread has been narrowing largely owing to new infrastructure coming online.

Nymex prices rise. At the Nymex, the May 2016 contract rose over the report week from $1.911/MMBtu last Wednesday to $2.036/MMBtu yesterday. The 12-month strip, which is the average of the 12 Nymex contracts from May 2016 through April 2017, rose from $2.410/MMBtu to $2.511/MMBtu from Wednesday to Wednesday.

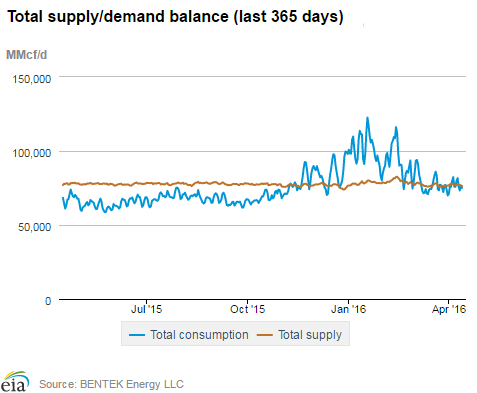

Supply down. Total supply fell by 0.4% for the report period, according to data from Bentek Energy. Dry production fell by 0.3%, which was likely the result of seasonal maintenance on several pipeline systems. Tennessee Gas Pipeline, which runs through the Marcellus and Utica areas, has been conducting maintenance this week. Several other major pipeline systems around the country also were performing maintenance, particularly in the Northeast and Midcontinent. Imports from Canada fell 1.1% this week, with declines in the West and Northeast offsetting an increase in imports to the Midwest. LNG sendout declined, but is a minor contributor to overall supply.

Consumption increases slightly. Overall consumption this week increased by 1.3%. Residential and commercial consumption increased by 2.7%. Consumption of natural gas for electric power generation rose 0.7%, and industrial consumption rose 0.4%. Exports to Mexico increased by 3.1%.

Storage:

Working gas stocks post net withdrawals during the first week of the 2016 refill season. Net withdrawals from storage totaled 3 Bcf during the storage report week. These withdrawals contrast with the five-year (2011-15) average net injection of 22 Bcf and last year's net injection 49 Bcf during the storage report week—the first full week of the injection season, which traditionally begins on April 1. As a result, the surplus compared with the five-year average declined 25 Bcf to 849 Bcf, and the surplus compared with year-ago levels decreased by 52 Bcf to 956 Bcf.

Widespread injections occurred in large sections of the Lower 48 states. Despite a total net storage withdrawal on a national basis, significant injections prevailed in the South Central, Mountain, and Pacific regions. Net withdrawals reported for the Lower 48 states were driven by withdrawal activity in the East and Midwest regions netting to 25 Bcf, more than offsetting the net injections totaling 22 Bcf reported in the other regions. The five-year average net injections for the report week in the East and Midwest regions totaled 4 Bcf.

Storage withdrawals for the week are within the range of expectations. The median expectation of market analysts was a net injection of 2 Bcf, with predictions ranging from a net withdrawal of 14 Bcf to a net injection of 10 Bcf. At the release of the Weekly Natural Gas Storage Report, the price of the natural gas futures contract on the Nymex for May delivery at the Henry Hub gained almost 2¢/MMBtu, with 1,012 executed trades. Prices continued to climb in subsequent trading, averaging $2.02/MMBtu and gaining 4¢/MMBtu within two minutes of the release.

National temperatures higher than normal, but significantly lower than normal in Midwest and Northeast. Temperatures in the Lower 48 states averaged 50°F during the report week, 1% higher than normal and 6% below last year at this time. However, temperatures were significantly less than normal in key heating demand regions of the country, including the Northeast, Middle Atlantic, and East and West South Central U.S. Census regions, which roughly coincide with the East and Midwest storage regions, which saw gas storage withdrawals.

See also:

")

| Spot Prices ($/MMBtu) | Thu, 07-Apr |

Fri, 08-Apr |

Mon, 11-Apr |

Tue, 12-Apr |

Wed, 13-Apr |

|---|---|---|---|---|---|

| Henry Hub |

1.93 |

1.98 |

1.88 |

1.94 |

1.98 |

| New York |

1.74 |

1.70 |

1.68 |

1.77 |

1.65 |

| Chicago |

1.97 |

2.00 |

1.90 |

1.91 |

1.92 |

| Cal. Comp. Avg,* |

1.83 |

1.83 |

1.79 |

1.83 |

1.85 |

| Futures ($/MMBtu) | |||||

| May contract | 2.018

|

1.990

|

1.912

|

2.004

|

2.036

|

| June contract |

2.101 |

2.077 |

2.001 |

2.083 |

2.119 |

| *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. natural gas supply - Gas Week: (4/6/16 - 4/13/16) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| Gross production | -1.5%

|

-0.3%

|

| Dry production | -1.4%

|

-0.3%

|

| Canadian imports | 0.8%

|

-1.1%

|

| West (net) | -2.6%

|

-4.1%

|

| Midwest (net) | 1.5%

|

7.0%

|

| Northeast (net) | 53.9%

|

-22.5%

|

| LNG imports | 186.5%

|

-18.9%

|

| Total supply | -1.1%

|

-0.4%

|

| Source: BENTEK Energy LLC | ||

| U.S. consumption - Gas Week: (4/6/16 - 4/13/16) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| U.S. consumption | 11.8%

|

1.3%

|

| Power | 0.9%

|

0.7%

|

| Industrial | 3.7%

|

0.4%

|

| Residential/commercial | 28.4%

|

2.7%

|

| Total demand | 12.8%

|

1.4%

|

| Source: BENTEK Energy LLC | ||

| Rigs | |||

|---|---|---|---|

Fri, April 08, 2016 |

Change from |

||

last week |

last year |

||

| Oil rigs | 354 |

-2.21% |

-53.42% |

| Natural gas rigs | 89 |

1.14% |

-60.44% |

| Miscellaneous | 0 |

0.00% |

-100.00% |

| Rig numbers by type | |||

|---|---|---|---|

Fri, April 08, 2016 |

Change from |

||

last week |

last year |

||

| Vertical | 50 |

-9.09% |

-60.94% |

| Horizontal | 341 |

-1.45% |

-55.71% |

| Directional | 52 |

6.12% |

-42.22% |

| Source: Baker Hughes Inc. | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2016-04-08 |

2016-04-01 |

change |

|

| East | 419 |

434 |

-15 |

|

| Midwest | 538 |

548 |

-10 |

|

| Mountain | 150 |

149 |

1 |

|

| Pacific | 269 |

265 |

4 |

|

| South Central | 1,101 |

1,084 |

17 |

|

| Total | 2,477 |

2,480 |

-3 |

|

| Source: U.S. Energy Information Administration | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (4/8/15) |

5-year average (2011-2015) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 248 |

69.0 |

301 |

39.2 |

|

| Midwest | 261 |

106.1 |

332 |

62.0 |

|

| Mountain | 117 |

28.2 |

113 |

32.7 |

|

| Pacific | 273 |

-1.5 |

209 |

28.7 |

|

| South Central | 623 |

76.7 |

673 |

63.6 |

|

| Total | 1,521 |

62.9 |

1,628 |

52.1 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- heating & cooling degree days (week ending Apr 07) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 183

|

23

|

19

|

0

|

0

|

0

|

||

| Middle Atlantic | 156

|

13

|

32

|

0

|

0

|

0

|

||

| E N Central | 178

|

30

|

58

|

0

|

0

|

0

|

||

| W N Central | 144

|

2

|

23

|

0

|

-1

|

-1

|

||

| South Atlantic | 68

|

-8

|

20

|

19

|

6

|

-7

|

||

| E S Central | 67

|

-3

|

25

|

0

|

-5

|

-13

|

||

| W S Central | 36

|

-1

|

20

|

13

|

-2

|

-29

|

||

| Mountain | 94

|

-37

|

-18

|

8

|

3

|

3

|

||

| Pacific | 29

|

-47

|

-49

|

2

|

0

|

2

|

||

| United States | 110

|

-2

|

16

|

6

|

2

|

-5

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Apr 07, 2016

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Apr 07, 2016

Source: NOAA/National Weather Service