March 14, 2016: Correction in the text.

In the News:

Australia's Gorgon, one of the world's LNG megaprojects, prepares to ship first cargo

Gorgon LNG project is one of the largest natural gas developments in Australia and one of the larger natural gas projects in the world. It includes a domestic natural gas plant, a carbon dioxide injection project, and a liquefied natural gas (LNG) export facility, which is preparing to ship its first cargo next week. Gorgon, which will supply gas domestically and internationally, is located on Barrow Island, offshore Western Australia, and has a total liquefaction capacity of 2.1 billion cubic feet per day (Bcf/d), slightly lower than the capacity at Australia's largest existing liquefaction project, the North West Shelf. The Gorgon project's three liquefaction trains (each with a capacity of 0.69 Bcf/d) will be commissioned in six-month intervals, with two trains expected to become operational by the end of this year.

While Gorgon LNG was initially envisioned more than 20 years ago, the final investment decision was not reached until 2009. The project took more than six years to complete, with the original estimated capital costs of $37 billion U.S. dollars in 2009 growing to $54 billion by 2013. Many upward cost revisions followed increasing labor costs, logistical challenges, and appreciation of the Australia dollar against the U.S. dollar. The project's location on Barrow Island, which is classified as a Class A natural reserve, required implementation of various environmental protection measures, which also contributed to cost increases. For example, Gorgon LNG is one of the first LNG projects in the world developing a carbon sequestration project, because of the high carbon emissions in the fields that provide feedstock gas for the project. This project is estimated to reduce greenhouse gas emissions by 40% at a cost of around $2 billion.

Since 2014, Australia has commissioned three of the seven liquefaction projects that are being developed—Queensland Curtis Trains 1 and 2, Gladstone LNG Train 1, and Australia Pacific LNG Train 1—totaling 2.25 Bcf/d of capacity. In addition to Gorgon, three other projects currently under construction—Ichthys, Wheatstone, and Prelude Floating Liquefaction—will be commissioned between 2016 and 2018. Once all these projects become operational, Australia's liquefaction capacity additions are slated to reach 8.2 Bcf/d. Combined with the existing capacity, Australia will overtake Qatar as the world's largest global liquefaction capacity holder with a total capacity of 11.5 Bcf/d by 2019.

Most of Gorgon's liquefaction volumes are to be sold under long-term contracts to Asian buyers.

The first shipment from Gorgon LNG follows the first shipment from the United States, on February 24, with Cheniere's Sabine Pass export.

Overview:

(For the Week Ending Wednesday, March 9, 2016)

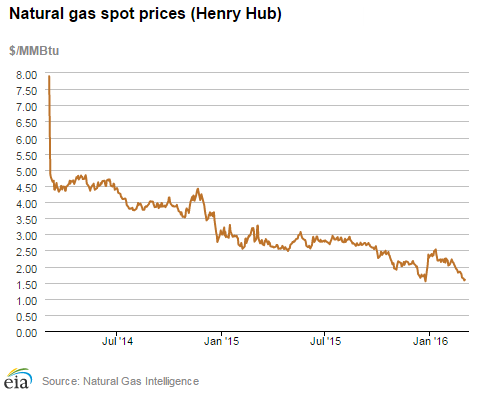

- Natural gas spot prices remained at historic lows this report week (Wednesday, March 2, to Wednesday, March 9) as Henry Hub spot prices dropped to their lowest level in 20 years. Henry Hub spot prices during the report week posted a net loss of 2¢ as they fell from $1.59 per million British thermal unit (MMBtu) last Wednesday to $1.57/MMBtu yesterday.

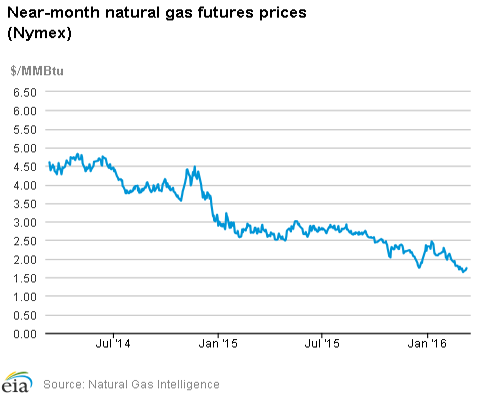

- At the New York Mercantile Exchange (Nymex), the price of the near-month (April 2016) contract rose from $1.678/MMBtu last Wednesday to $1.752/MMBtu yesterday.

- Net withdrawals from storage totaled 57 billion cubic feet (Bcf) for the week ending March 4. Working gas stocks are 2,479 Bcf–58% and 42% above the year-ago and five-year (2011-15) average levels, respectively.

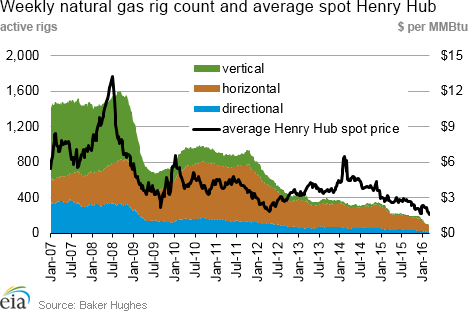

- The natural gas rotary rig count fell below 100 this week, with 97 active units in service as of March 4, 2016. This is the lowest level in Baker Hughes's recorded history. The total rig count fell by 13 units to 489, with oil rigs falling by 8 units to 392.

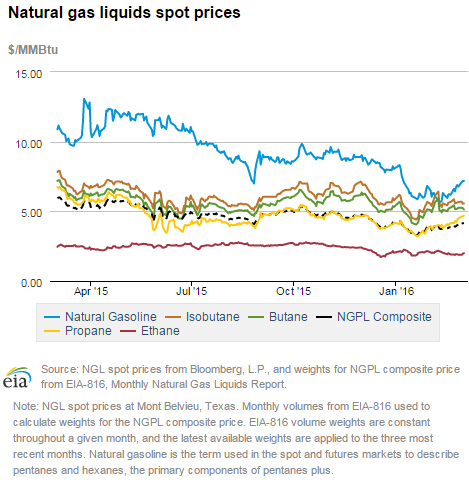

- The natural gas plant liquids (NGPL) composite price at Mont Belvieu, Texas, increased by 22¢ to $4.17/MMBtu for the week ending Friday, March 4. The spot price movements were mixed this week, with ethane rising 5.9%, natural gasoline rising 7.9%, and propane rising 8.5%. The spot price of butane fell 0.5% and the price of isobutane fell 0.6%.

Prices/Demand/Supply:

Henry Hub prices drop to historic lows. The national benchmark Henry Hub spot price in southern Louisiana posted a 2¢ decline this week, ending at $1.57/MMBtu. On Friday, March 4, the spot price dropped to $1.49/MMBtu, its lowest level since 1995. Prices changes at other trading locations were mixed, and most prices dropped to their weekly lows on Friday. In California, prices fell slightly at most spot locations around the state, with the exception of the PG&E Citygate, where prices rose 10¢ Wednesday to Wednesday. At the Chicago Citygate, prices rose 5¢ week over week, ending the week at $1.77/MMBtu.

Northeast prices fall substantially. Prices serving major market locations in the Northeast fell week over week. At the Algonquin Citygate, which serves Boston-area consumers, prices fell from $4.30/MMBtu last Wednesday to $1.08/MMBtu yesterday as temperatures warmed up over the report week. While very low, Algonquin Citygate prices remain above their record low of 82¢/MMBtu reached in July 2015. At Transcontinental Pipeline's Zone 6 delivery point serving New York City customers, prices fell from $1.71/MMBtu last Wednesday to $1.00/MMBtu yesterday.

Marcellus prices slide. At Dominion South in northwest Pennsylvania, prices began at $1.02/MMBtu last Wednesday and ended the report week at 87¢/MMBtu yesterday. On Transco's Leidy Line in northern Pennsylvania, prices fell similarly, declining from $1.02/MMBtu last Wednesday to 85¢/MMBtu yesterday.

Nymex prices up slightly. In contrast to spot markets, prices in the futures market increased slightly this week. The April 2016 near-month contract rose from $1.678/MMBtu last Wednesday to $1.752/MMBtu yesterday. Despite this week's increase, Nymex prices remain relatively low. The price of the 12-month strip (the average price of the 12 contracts between April 2016 and March 2017) rose from $2.253/MMBtu last Wednesday to $2.304/MMBtu yesterday.

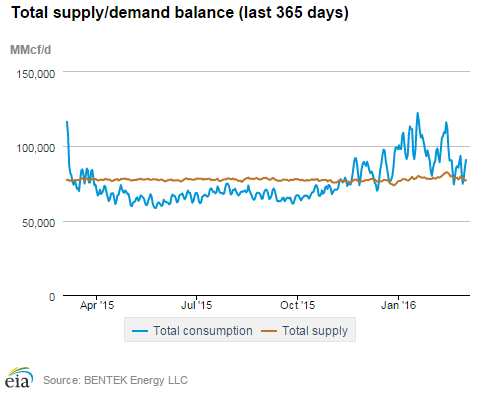

Supply declines. Total supply fell by 0.8% as a slight increase in domestic production was offset by declines in imports. Dry production rose by 0.1% this week, and remains 2.4% greater than year-ago levels. Pipeline imports to the United States from Canada fell by 4.7%, and LNG sendout, already very low, dropped to minimal levels.

Warmer weather leads to declines in consumption. According to Bentek Energy data, residential and commercial sector natural gas consumption fell 11.4% week over week, the result of mild temperatures this week. Industrial sector consumption fell 2.7%. Consumption of natural gas for power generation rose 1.4%, and pipeline exports to Mexico rose 3.7%. Total U.S. consumption posted a net decline of 5.2%.

Storage:

Net withdrawals are significantly below the five-year average and last year's withdrawals. Net withdrawals from storage totaled 57 Bcf, compared with the five-year average of 118 Bcf, and last year's pull of 174 Bcf.

Working gas stocks could finish the heating season near record-high levels. If withdrawals from storage follow the five-year average for the remainder of the heating season, working gas stocks will total 2,336 Bcf on March 31–the traditional end of the heating season. The record high for stock levels at the end of the heating season occurred in 2012, when working gas stocks totaled 2,473 Bcf on March 31, 2012, following a much warmer-than-normal winter. Working gas stocks are 727 Bcf above the five-year average and 911 Bcf above last year at this time.

Net withdrawals from storage were within the range of expectations for the storage report. Analyst expectations for this week's storage figure ranged between 35 to 63 Bcf, with a median of 58 Bcf. Immediately following the release of the EIA Weekly Natural Gas Storage Report (WNGSR), prices on the Nymex for the futures contract for April delivery at the Henry Hub fell 3¢/MMBtu, to $1.76/MMBtu.

Temperatures were higher than normal during the storage week. Temperatures in the Lower 48 states averaged 44°F during the report week, 10% higher than normal, and 44% above last year at this time. These above-normal temperatures continued an ongoing pattern during the 2015-16 heating season (November 1, 2015-March 31, 2016). Temperatures have been above normal levels during 15 out of 18 weeks in the 2015-16 heating season. Cumulative heating degree-days during this period are 15% below normal.

See also:

")

| Spot Prices ($/MMBtu) | Thu, 03-Mar |

Fri, 04-Mar |

Mon, 07-Mar |

Tue, 08-Mar |

Wed, 09-Mar |

|---|---|---|---|---|---|

| Henry Hub |

1.56 |

1.49 |

1.52 |

1.55 |

1.57 |

| New York |

1.82 |

1.24 |

1.10 |

1.02 |

1.00 |

| Chicago |

1.66 |

1.57 |

1.61 |

1.68 |

1.77 |

| Cal. Comp. Avg,* |

1.57 |

1.47 |

1.60 |

1.60 |

1.62 |

| Futures ($/MMBtu) | |||||

| March contract |

1.639 |

1.666 |

1.690 |

1.712 |

1.752 |

| April contract |

1.767 |

1.787 |

1.789 |

1.803 |

1.846 |

| *Avg. of NGI's reported prices for: Malin, PG&E citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. natural gas supply - Gas Week: (3/2/16 - 3/9/16) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| Gross production | 2.40%

|

0.11%

|

| Dry production | 2.37%

|

0.11%

|

| Canadian imports | -13.50%

|

-4.74%

|

| West (net) | 1.95%

|

-0.25%

|

| Midwest (net) | 26.75%

|

-20.73%

|

| Northeast (net) | -78.16%

|

54.46%

|

| LNG imports | -68.52%

|

-82.01%

|

| Total supply | 0.96%

|

-0.79%

|

| Source: BENTEK Energy LLC | ||

| U.S. consumption - Gas Week: (3/2/16 - 3/9/16) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| U.S. consumption | -13.5%

|

-5.2%

|

| Power | 6.8%

|

1.4%

|

| Industrial | -6.0%

|

-2.7%

|

| Residential/commercial | -28.8%

|

-11.4%

|

| Total demand | -12.2%

|

-4.9%

|

| Source: BENTEK Energy LLC | ||

| Rigs | |||

|---|---|---|---|

Fri, March 04, 2016 |

Change from |

||

last week |

last year |

||

| Oil rigs | 392 |

-2.00% |

-57.48% |

| Natural gas rigs | 97 |

-4.90% |

-63.81% |

| Miscellaneous | 0 |

0.00% |

-100.00% |

| Rig numbers by type | |||

|---|---|---|---|

Fri, March 04, 2016 |

Change from |

||

last week |

last year |

||

| Vertical | 58 |

0.00% |

-67.23% |

| Horizontal | 389 |

-2.02% |

-56.54% |

| Directional | 42 |

-10.64% |

-65.00% |

| Source: Baker Hughes Inc. | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2016-03-04 |

2016-02-26 |

change |

|

| East | 464 |

495 |

-31 |

|

| Midwest | 587 |

621 |

-34 |

|

| Mountain | 146 |

145 |

1 |

|

| Pacific | 258 |

255 |

3 |

|

| South Central | 1,024 |

1,020 |

4 |

|

| Total | 2,479 |

2,536 |

-57 |

|

| Source: U.S. Energy Information Administration | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (3/4/15) |

5-year average (2011-2015) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 322 |

44.1 |

363 |

27.8 |

|

| Midwest | 320 |

83.4 |

400 |

46.8 |

|

| Mountain | 113 |

29.2 |

120 |

21.7 |

|

| Pacific | 263 |

-1.9 |

202 |

27.7 |

|

| South Central | 550 |

86.2 |

667 |

53.5 |

|

| Total | 1,568 |

58.1 |

1,752 |

41.5 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- heating & cooling degree days (week ending Mar 03) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 199

|

-34

|

-115

|

0

|

0

|

0

|

||

| Middle Atlantic | 196

|

-25

|

-100

|

0

|

0

|

0

|

||

| E N Central | 217

|

-18

|

-121

|

0

|

0

|

0

|

||

| W N Central | 201

|

-34

|

-147

|

0

|

0

|

0

|

||

| South Atlantic | 132

|

-5

|

-45

|

5

|

-4

|

-7

|

||

| E S Central | 132

|

-1

|

-37

|

0

|

-3

|

-1

|

||

| W S Central | 61

|

-23

|

-97

|

9

|

1

|

8

|

||

| Mountain | 117

|

-62

|

-108

|

5

|

4

|

5

|

||

| Pacific | 46

|

-50

|

-61

|

0

|

-1

|

0

|

||

| United States | 147

|

-28

|

-95

|

2

|

-1

|

0

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Mar 03, 2016

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Mar 03, 2016

Source: NOAA/National Weather Service