In the News:

November cold snap led to larger- than- average withdrawals from natural gas storage

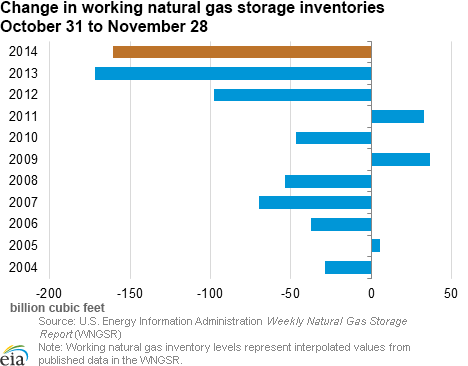

During the first four weeks of November, working natural gas storage inventories fell 161 billion cubic feet (Bcf), representing the second largest net withdrawal for that period in more than 10 years, according to EIA's Weekly Natural Gas Storage Report (WNGSR.) This decline was driven by a larger-than-normal natural gas storage withdrawal for the week ending November 21, when inventories decreased by 162 Bcf.

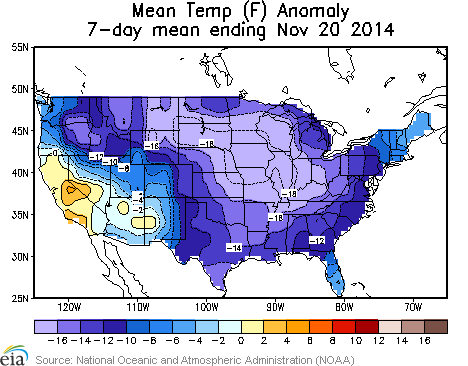

After inventories increased during the first week in November, which is fairly common, the first net storage withdrawal of the 2014-15 heating season occurred during the week ending November 14, when inventories fell 17 Bcf. Although unseasonably cold weather occurred in some regions of the country during the second week in November, it was not until the week ending November 21 that the entire nation had temperatures well below the seasonal averages.

This cold weather resulted in residential and commercial consumption that was 110 Bcf above the previous week, according to data from Bentek Energy. The cold weather also contributed to a 23 Bcf week-over-week increase in the use of natural gas for power generation (power burn). The highest power burn increases occurred in the Southeast, where the primary source of heating is electricity. In that region, power burn increased by 24%, or 10 Bcf, week-to-week. Total U.S. consumption of natural gas increased by 144 Bcf from the previous week, and it reached a record-high daily level for November on Tuesday, November 18 at 104 Bcf.

The 162 Bcf withdrawal for the week ending November 21 tied for the largest weekly November storage withdrawal on record. It was 156 Bcf larger than the five-year average for the same week, and 145 Bcf larger than the withdrawal reported for that week last year.

The large withdrawal for the week ending November 21 is comparable with inventory pulls that occur deeper into winter. The largest monthly withdrawals typically occur during January, and have had a weekly average of 177 Bcf over the past five years. The record weekly natural gas withdrawal occurred last winter, for the week ending January 14, when 287 Bcf of gas was pulled from storage.

Overview:

(For the Week Ending Wednesday, December 3, 2014)

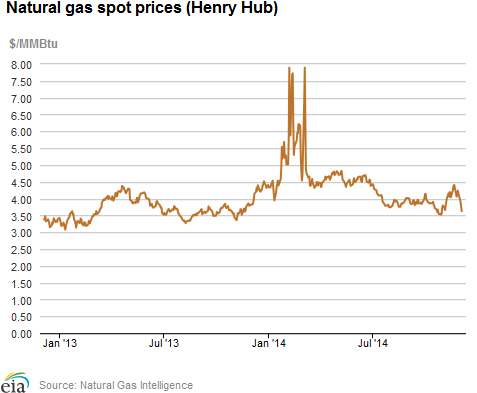

- Spot markets were closed on Thursday and Friday of the report week (Wednesday to Wednesday), due to the Thanksgiving holiday. Outside of the Northeast, spot prices fell at market locations across the country during the report week with closer-to-average temperatures in many locations during the last half of the report week. The Henry Hub spot price decreased from $4.24 per million British thermal units (MMBtu) last Wednesday, November 26, to $3.63/MMBtu yesterday, December 3.

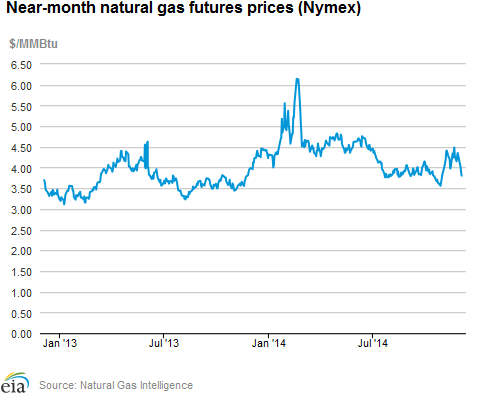

- At the New York Mercantile Exchange (Nymex), the January 2015 contract fell steadily over the week, beginning at $4.355/MMBtu last Wednesday and ending at $3.805/MMBtu yesterday.

- Working natural gas in storage decreased to 3,410 Bcf as of Friday, November 28, according to the U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report (WNGSR). A net withdrawal from storage of 22 Bcf for the week resulted in storage levels 6.2% below year-ago levels and 9.8% below the five-year average for this week.

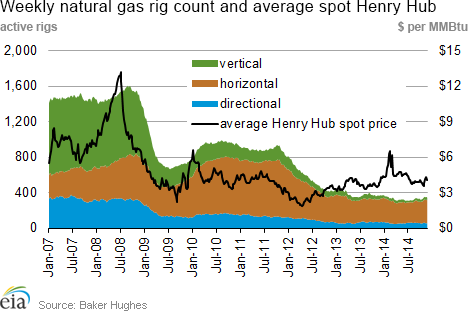

- The total U.S. rotary rig count for the week ending November 26 fell by 12 units to 1,917 rigs, according to data from Baker Hughes Inc. The natural gas rig count decreased by 11 units to 344, while oil rigs fell by 2 units to 1,572.

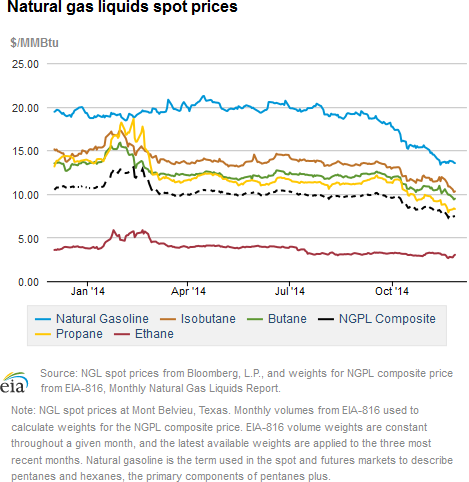

- The Mont Belvieu natural gas plant liquids composite price fell by 3.8% to $7.43/MMBtu for the week of November 24-28. With the exception of ethane, which remained flat, all of the other component prices fell. The price of natural gasoline, propane, isobutane, and butane declined by 0.1%, 3.9%, 9.7%, and 8.2%, respectively.

Prices/Demand/Supply:

Prices fall at market locations outside the Northeast. Natural gas prices at most market locations outside the Northeast fell in each day of trading, supported by weaker power sector demand and forecasts of more moderate temperatures. With well-below-normal temperatures forecast in many areas over the holiday weekend (Thursday through Sunday), prices in the Midwest and Midcontinent regions rose 10 to 15 cents/MMBtu in trading on Wednesday, but fell 30 to 40 cents on Monday. Similar price movements occurred at market locations in the West, as well as at the Henry Hub in Louisiana. After increasing 12 cents/MMBtu in trading last Wednesday, the Henry Hub spot price started the report week at $4.24/MMBtu, and then declined 34 cents/MMBtu on Monday. Spot prices at the Henry Hub declined further in trading Tuesday and Wednesday, ending the report week at $3.63/MMBtu.

Northeast spot prices show seasonal volatility. Reflecting daily temperature swings, spot prices at the Algonquin Citygate, which serves Boston, fluctuated more than $1/MMBtu in day-to-day trading for most of the report week. Prices at Algonquin began the week at $5.55/MMBtu, after falling more than $1/MMBtu in Wednesday trading. Prices continued to decline, closing on Tuesday at $3.72/MMBtu. Prices increased $2.20/MMBtu from Tuesday to Wednesday, with the arrival of colder-than-normal weather, ending the report week at $5.92/MMBtu. Although prices at the Transcontinental Pipeline's Zone 6 (Transco Z6 NY) trading point for delivery to New York City showed similar directional daily movements to Algonquin, the price changes were much more modest. Prices at Transco Z6 NY started the report week at $4.00/MMBtu last Wednesday, fell to $3.54/MMBtu on Tuesday, and rose to $3.74/MMBtu yesterday.

Most Marcellus-area prices increase. The largest price increase in the Marcellus area occurred at Transcontinental's Leidy Line trading point in northeastern Pennsylvania, where prices rose from $2.02/MMBtu last Wednesday to $2.40/MMBtu yesterday, an increase of 38 cents/MMBtu. Price movements at Tennessee's Zone 4 Marcellus location and Dominion South were mixed, with Tennessee's Zone 4 Marcellus increasing 11 cents/MMBtu and Dominion South decreasing 15 cents/MMBtu, from Wednesday to Wednesday. Prices at Tennessee's Zone 4 Marcellus closed the week yesterday at $2.13/MMBtu, while prices at Dominion South ended the week at $2.85/MMBtu.

January futures contract price falls over the report week. The January futures contract price fell during each day of trading in the report week. The January contract started the report week at $4.355/MMBtu. Prices fell 27 cents/MMBtu in limited trading on Friday, despite the report of a significantly larger-than-average inventory withdrawal. Prices continued to fall in trading at the end of the report week, and closed at $3.805/MMBtu yesterday, a decrease of 55 cents from Wednesday to Wednesday. The 12-month strip, the average of January 2015 through December 2015 futures contracts, ended the week down 30 cents, at $3.623/MMBtu.

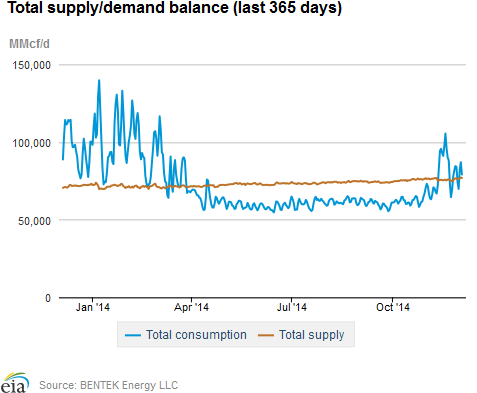

Dry gas production sets single-day record during the report week. According to data from Bentek Energy, dry gas production exceeded 71.8 billion cubic feet per day (Bcf/d) on Tuesday, December 2. Production was more than 71 Bcf/d for all days in the report week, and for the entire report week, production was 2% higher compared to the previous week. Imports of natural gas from Canada decreased slightly, driven by lower imports into the West and Midwest regions, while LNG sendout remained minimal.

Demand increases with seasonal temperatures. Cooler temperatures during the report week led to a 3% increase in total natural gas consumption week-over-week. Natural gas consumption increased in all demand sectors with the exception of the electric power sector. A 7% increase in residential and commercial consumption drove the overall increase in U.S. gas consumption. Power burn fell 2%, largely as a result of more moderate weather in the Southeast and Southwest, which caused consumption in those regions to fall 4% and 17%, respectively. Industrial consumption rose 1%, and U.S. exports of natural gas to Mexico increased 8%, although U.S. exports to Mexico only contributed 2% to 3% to total daily gas demand.

Storage

Net withdrawal is significantly lower than the five-year average and last year's withdrawal. The net withdrawal reported for the week ending November 28 was 22 Bcf, 28 Bcf lower than the five-year average net withdrawal of 50 Bcf and 119 Bcf lower than last year's net withdrawal of 141 Bcf. Working gas inventories as of November 28 totaled 3,410 Bcf, 227 Bcf (6.2%) lower than last year at this time and 372 Bcf (9.8%) lower than the five-year (2009-13) average.

Storage withdrawals are smaller than market expectations. Market expectations called for an average pull of 38 Bcf. When the EIA storage report was released at 10:30 a.m. on December 4, the price for the January natural gas futures contract fell 4 cents to $3.69/MMBtu in trading on the Nymex.

The West and Producing regions post injections. The East region had a net withdrawal of 34 Bcf (equal to its five-year average pull). The West and the Producing regions had net injections of 1 Bcf (compared with its five-year average withdrawal of 7 Bcf) and 11 Bcf (compared with its five-year average withdrawal of 10 Bcf), respectively. Storage levels for all three regions remain below their year-ago and five-year average levels.

Temperatures during the storage report week are slightly warmer than normal. Temperatures in the Lower 48 states averaged 43.3° for the storage report week, 0.6° warmer than the 30-year normal temperature and 5.0° warmer than the temperatures during the same week last year. There were 155 population-weighted heating degree days during the storage report week, 3 less than the 30-year normal and 35 less than during the same period last year.

See also:

| Spot Prices ($/MMBtu) | Thu, 27-Nov |

Fri, 28-Nov |

Mon, 1-Dec |

Tue, 2-Dec |

Wed, 3-Dec |

|---|---|---|---|---|---|

| Henry Hub | Holiday |

Closed |

3.90 |

3.75 |

3.63 |

| New York | Holiday |

Closed |

3.76 |

3.54 |

3.74 |

| Chicago | Holiday |

Closed |

4.16 |

3.95 |

3.72 |

| Cal. Comp. Avg,* | Holiday |

Closed |

4.11 |

4.00 |

3.88 |

| Futures ($/MMBtu) | |||||

| January Contract | Holiday |

4.088 |

4.007 |

3.874 |

3.805 |

| February Contract | Holiday |

4.085 |

4.009 |

3.877 |

3.808 |

| *Avg. of NGI's reported prices for: Malin, PG&E citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| Spot Prices ($/MMBtu) | Thu, 20-Nov |

Fri, 21-Nov |

Mon, 24-Nov |

Tue, 25-Nov |

Wed, 26-Nov |

|---|---|---|---|---|---|

| Henry Hub | 4.41 |

4.31 |

4.06 |

4.12 |

4.24 |

| New York | 5.19 |

3.19 |

3.36 |

4.12 |

4.00 |

| Chicago | 5.00 |

4.79 |

4.54 |

4.47 |

4.59 |

| Cal. Comp. Avg,* | 4.64 |

4.47 |

4.34 |

4.30 |

4.47 |

| Futures ($/MMBtu) | |||||

| December Contract | 4.489 |

4.266 |

4.151 |

4.282 |

Expired |

| January Contract | 4.649 |

4.417 |

4.304 |

4.403 |

4.355 |

| February Contract | 4.611 |

4.387 |

4.281 |

4.377 |

4.334 |

| *Avg. of NGI's reported prices for: Malin, PG&E citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. Natural Gas Supply - Gas Week: (11/26/14 - 12/3/14) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| Gross Production | 8.01%

|

1.64%

|

| Dry Production | 7.93%

|

1.63%

|

| Canadian Imports | -4.36%

|

-2.19%

|

| West (Net) | 3.61%

|

-11.25%

|

| MidWest (Net) | -7.82%

|

-1.21%

|

| Northeast (Net) | -21.90%

|

66.20%

|

| LNG Imports | -41.91%

|

5.21%

|

| Total Supply | 6.90%

|

1.36%

|

| Source: BENTEK Energy LLC | ||

| U.S. Consumption - Gas Week: (11/26/14 - 12/3/14) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| U.S. Consumption | -4.2%

|

2.9%

|

| Power | -9.6%

|

-2.2%

|

| Industrial | 2.4%

|

1.1%

|

| Residential/Commercial | -5.2%

|

6.7%

|

| Total Demand | -3.6%

|

3.1%

|

| Source: BENTEK Energy LLC | ||

| Rigs | |||

|---|---|---|---|

Fri, November 28, 2014 |

Change from |

||

last week |

last year |

||

| Oil Rigs | 1,572 |

-0.13% |

13.01% |

| Natural Gas Rigs | 344 |

-3.10% |

-6.27% |

| Miscellaneous | 1 |

0.00% |

-80.00% |

| Rig Numbers by Type | |||

|---|---|---|---|

Fri, November 28, 2014 |

Change from |

||

last week |

last year |

||

| Vertical | 352 |

0.00% |

-14.98% |

| Horizontal | 1,371 |

-0.07% |

21.65% |

| Directional | 194 |

-5.37% |

-12.61% |

| Source: Baker Hughes Inc. | |||

| Working Gas in Underground Storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2014-11-28 |

2014-11-21 |

change |

|

| East | 1,830 |

1,864 |

-34 |

|

| West | 478 |

477 |

1 |

|

| Producing | 1,102 |

1,091 |

11 |

|

| Total | 3,410 |

3,432 |

-22 |

|

| Source: U.S. Energy Information Administration | ||||

| Working Gas in Underground Storage | |||||

|---|---|---|---|---|---|

Historical Comparisons |

|||||

Year ago (11/28/13) |

5-year average (2009-2013) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 1,872 |

-2.2 |

2,013 |

-9.1 |

|

| West | 532 |

-10.2 |

522 |

-8.4 |

|

| Producing | 1,233 |

-10.6 |

1,247 |

-11.6 |

|

| Total | 3,637 |

-6.2 |

3,782 |

-9.8 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- Heating & Cooling Degree Days (week ending Nov 27) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 168

|

-15

|

-40

|

0

|

0

|

0

|

||

| Middle Atlantic | 174

|

-1

|

-33

|

0

|

0

|

0

|

||

| E N Central | 222

|

21

|

-27

|

0

|

0

|

0

|

||

| W N Central | 246

|

20

|

-37

|

0

|

0

|

0

|

||

| South Atlantic | 121

|

1

|

-25

|

13

|

2

|

-1

|

||

| E S Central | 126

|

3

|

-36

|

0

|

-1

|

0

|

||

| W S Central | 79

|

-9

|

-69

|

5

|

1

|

1

|

||

| Mountain | 171

|

-23

|

-30

|

0

|

0

|

0

|

||

| Pacific | 62

|

-38

|

-35

|

0

|

-1

|

0

|

||

| United States | 155

|

-3

|

-35

|

3

|

1

|

0

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Nov 27, 2014

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Nov 27, 2014

Source: NOAA/National Weather Service