In the News:

New chemical plants expected to boost industrial natural gas demand by 4% in 2015

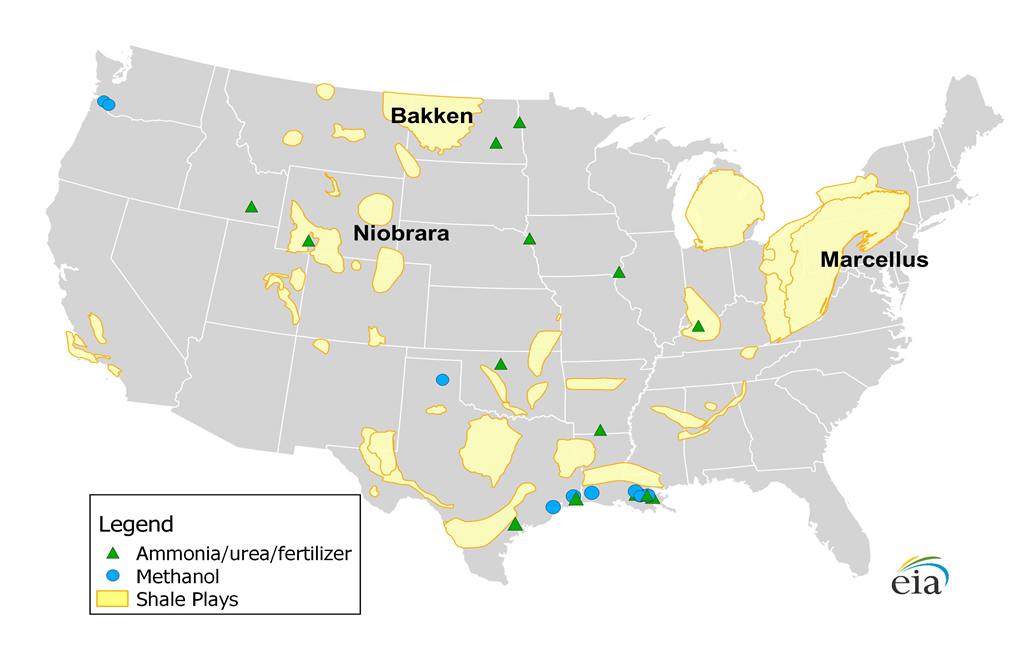

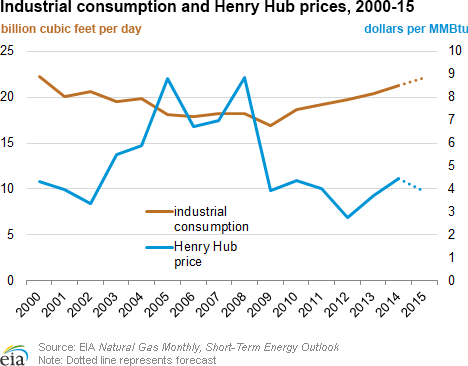

Industrial natural gas consumption has grown steadily since 2009, as relatively low prices have been attractive to customers who use natural gas as a feedstock for chemical production. Methanol plants and ammonia- or urea-based fertilizer plants are among the most natural gas-intensive industrial end users, with many using 100 million cubic feet per day (MMcf/d) or more. Low gas prices and proximity to shale resources have led to proposals for several new industrial facilities.

Two methanol plants are set to begin service this year — a small facility in Pampa, Texas, and one in Geismar, Louisiana. A handful of fertilizer plants have begun service, and an expansion is planned at a plant near Beaumont, Texas, later this year.

Many plants are on the Gulf Coast, but proximity to shale development in the Marcellus, Bakken, and Niobrara areas have led to proposals for facilities outside of Texas and Louisiana. Two large facilities coming online in 2015, a methanol plant in Clear Lake, Texas, and a fertilizer/urea plant in Wever, Iowa, will support continued growth in industrial demand. EIA projects growth in industrial demand will continue through 2015, with consumption averaging 21.3 billion cubic feet per day in 2014 and 22.1 Bcf/d in 2015, a 4% increase.

Developers hope to take advantage of abundant natural gas in the Bakken Shale. Two ammonia-based fertilizer plants are proposed for North Dakota for 2018. Farm-owned cooperative CHS Inc.'s proposed plant in Spiritwood and Northern Plains Nitrogen's proposed plant for Grand Forks are both in permitting stages. Both have expected production of 2,400 tons of ammonia per day and would use close to 100 MMcf/d of natural gas each, according to Bentek Energy estimates.

While most of the proposed methanol plants are on the Gulf Coast, two are proposed for 2018 in the Pacific Northwest. Northwest Innovation Works, a Chinese company, is planning two methanol facilities on the Columbia River in Washington and Oregon. The company hopes to export methanol produced in the United States to Asian markets.

Overview:

(For the Week Ending Wednesday, October 1, 2014)

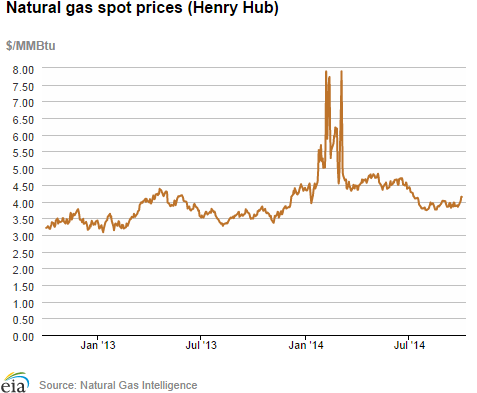

- Spot prices increased at most trading locations during the report week of September 24-October 1 as cooler weather moved in throughout much of the country. The Henry Hub spot price increased from $3.84 per million British thermal units (MMBtu) last Wednesday to $4.14/MMBtu yesterday. Spot prices in all markets across the country posted steady increases, ranging from $0.07/MMBtu to $0.30/MMBtu, while prices at several northeastern locations fluctuated considerably.

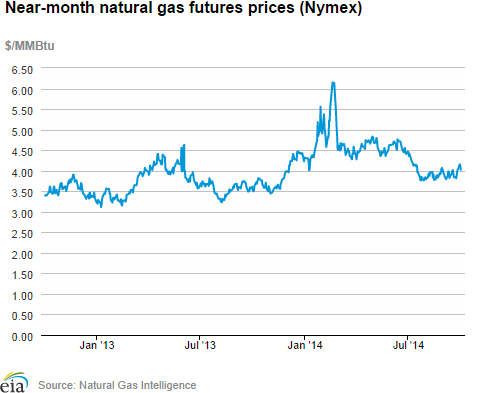

- At the New York Mercantile Exchange (Nymex), the price of the near-month (November 2014) contract increased by a dime from $3.911/MMBtu last Wednesday to $4.023/MMBtu yesterday.

- Working natural gas in storage rose to 3,100 Bcf as of Friday, September 26, according to the U.S. Energy Information Administration (EIA) Weekly Natural Gas Storage Report (WNGSR). A net increase in storage of 112 billion cubic feet (Bcf) for the week resulted in storage levels 10.7% below year-ago levels and 11.4% below the five-year average for this week.

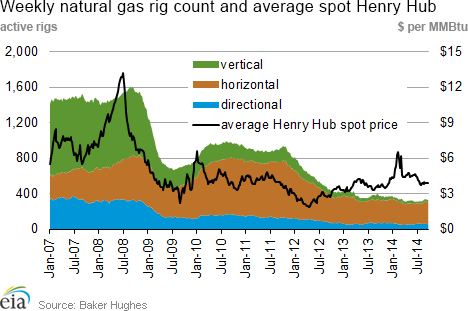

- The total U.S. rig count for the week ending September 26 remained unchanged from the previous two weeks (ending September 12 and 19) at 1,931 units, according to data from Baker Hughes Inc. The natural gas rig count increased by 9 to 338 units while oil rigs declined by 9 to 1,592 units. Natural gas rigs are 38 units below year-ago levels, while oil rig counts are 230 units greater than their levels last year.

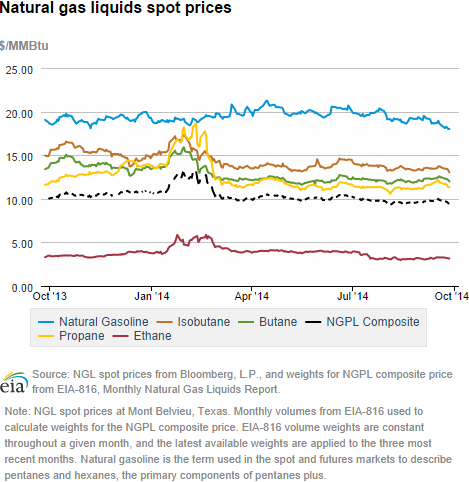

- The Mont Belvieu natural gas plant liquids composite price decreased by 2.9% to $9.58/MMBtu for the week of September 22-26. All other product prices also declined. The ethane price decreased 2.5%, while the prices of natural gasoline, propane, butane, and isobutane declined by 2.9%, 3.5%, 2.2%, and 2.3%, respectively.

Prices/Demand/Supply:

Natural gas prices increase across the country amid cooler weather. Natural gas prices increased on average by 5% in all markets except several New England trading locations. Prices continued to fluctuate at Algonquin Citygate, serving Boston, and Tennessee Zone 6 200 line, serving Rhode Island, Massachusetts, and New Hampshire, after increasing by approximately 80% in the previous week, then declining by 11% and 26%, respectively, by yesterday. Overall, prices across the country posted steady gains week-over-week, with the Henry Hub spot price increasing from $3.84/MMBtu last Wednesday to $4.14/MMBtu yesterday. Prices in western markets increased by 2%-6%, with the California regional average ending the week at $4.36/MMBtu. Midwestern and Midcontinent prices gained $0.17-$0.28/MMBtu, with regional averages closing the week at $4.12/MMBtu and $3.94/MMBtu, respectively. Spot prices in the producing region of Texas and Louisiana followed a similar pattern, gaining a few cents each day of the week, for a cumulative increase of $0.17-$0.30/MMBtu across the region's trading locations. Prices in the Rocky Mountains gained on average $0.16/MMBtu to close the week at $3.93/MMBtu at Opal and $3.92/MMBtu at Kern River markets.

Prices in several New England markets continue to fluctuate. Prices at Algonquin Citygate continued choppy trading throughout the week. After initially spiking to $4.77/MMBtu on the previous Wednesday, prices declined to $3.04/MMBtu on Friday, then traded at $3.83/MMBtu on Monday and settled at $4.24/MMBtu yesterday. Prices at Tennessee Zone 6 Line 200 also fluctuated widely, spiking last Wednesday to $5.68/MMBtu, dropping to $3.22/MMBtu on Friday, and then increasing again to close the week at $4.23/MMBtu. On-going scheduled outages and flow restrictions on the Algonquin Gas Transmission Pipeline and Tennessee Gas Pipeline likely contributed to price fluctuations.

Northeastern prices post gains. Prices at most northeastern points increased during the week as colder temperatures settled in the area. At Transcontinental Pipeline's Zone 6 (Transco Z6) delivery point, which serves New York City, prices started the week at $1.86/MMBtu, then increased throughout the week and closed at $2.24/MMBtu yesterday. Prices at other northeastern trading locations also gained on average around $0.30/MMBtu, with Texas Eastern Zone 3, which serves customers in Pennsylvania and New York, finishing the week at $2.20/MMBtu yesterday.

Marcellus prices gain over the week, but remain low. Prices in the Marcellus production region remained low compared to most markets. At Tennessee Pipeline's Zone 4 Marcellus trading point, located in northeast Pennsylvania, prices fell from $1.73 on Wednesday to $1.61 on Friday, then increased moderately by the end of the report week to settle at $1.97/MMBtu yesterday. Prices at other Marcellus trading points were at multiyear lows because of constraints on take-away capacity out of the region. Dominion South traded at $1.58/MMBtu on Friday, its lowest price since December 1998. Prices at Millennium East Pool and Transco-Leidy Line also declined to some of their lowest levels, trading at $1.63/MMBtu and $1.61/MMBtu on Friday, before rebounding to $2.05/MMBtu and $2.01/MMBtu, respectively, yesterday.

Prices rise at the Nymex. The price of the near-month (November 2014) contract rose from $3.911/MMBtu last week to $4.023/MMBtu yesterday. The 12-month strip (the average of the 12 contracts between November 2014 and October 2015) remained unchanged at $3.962/MMBtu.

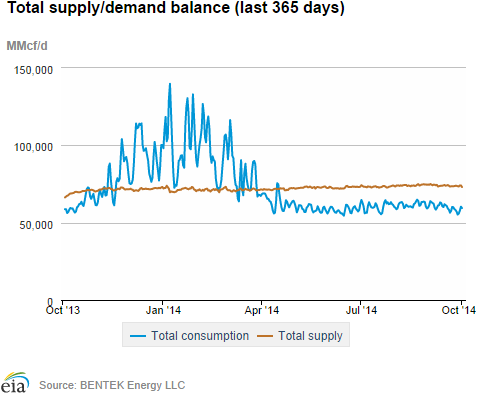

Demand declines slightly. Total natural gas consumption declined by 1.4%, according to Bentek data, led by decreased consumption in the residential/commercial (4.8%) and industrial (1%) sectors. Consumption of natural gas for power generation (power burn) increased modestly by 0.1%, driven by strong increases in the Midwest (69%), Northeast (17%), and Midcontinent (15%), which were offset by declines in power burn in the rest of the regions. Exports to Mexico also declined by 5.6%, but remained 13% above the year-ago level.

Supply remains flat. Despite dry gas production increasing by 0.2% week-over-week, overall supply remained flat, according to data from Bentek Energy. Dry gas production was 7.5% (4.8 Bcf/d) higher than it was the same time last year. Pipeline imports from Canada declined by 1.4%, led by declines in the Northeast and Midwest, and were 5.7% lower than year-ago levels. LNG imports remain at minimal levels.

Storage

Triple-digit net injections into storage much higher than average. The net injection reported for the week ending September 26 was 112 Bcf, 27 Bcf larger than the five-year average net injection of 85 Bcf and 13 Bcf larger than last year's net injection of 99 Bcf. Net injections were last in the triple digits 10 weeks ago and only exceeded this week's level three other weeks so far in this injection season. Working gas inventories totaled 3,100 Bcf, 373 Bcf (10.7%) less than last year at this time and 399 Bcf (11.4%) below the five-year (2009-13) average.

Storage build larger than expectations. Market expectations called for an average build of 107 Bcf. When the EIA storage report was released at 10:30 a.m., the price for the November natural gas futures contract fell 8 cents to $3.92/MMBtu in trading on the Nymex.

From the week ending on April 4 through the week ending on September 26, net storage injections totaled 2,278 Bcf versus 1,773 Bcf for the same 26 weeks in 2013, and 1,685 Bcf for these weeks between 2009 and 2013, on average. The average unit value of what storage holders put into storage from April 4 to September 26 was $4.28/MMBtu, 13% higher than the average value for the same 26 weeks last year of $3.78/MMBtu. The highest winter-month Nymex price (for the January 2015 contract) in trading for the week ending on September 26 averaged $4.10/MMBtu. This is 22 cents more than the current front month Nymex contract price for that week. A year ago, the difference was 34 cents/MMBtu.

There currently are five more weeks in the injection season, which traditionally occurs April 1 through October 31, although in each of the past 11 years, injections continued into November. In six of those years, there have been multiple weeks of net injections. There have also been multiple weeks within the injection season when the weekly change resulted in a net withdrawal. EIA forecasts that the end-of-October working natural gas inventory level will be 3,477 Bcf, which, as of September 9, would require an average injection of 75 Bcf per week through the end of October. EIA's forecast for the end-of-October inventory levels are below the five-year (2009-13) average peak storage value of 3,851 Bcf.

All regions post larger-than-average builds. The East, West, and Producing regions had net injections of 68 Bcf (18 Bcf larger than its five-year average), 8 Bcf (similar to its five-year average), and 36 Bcf (9 Bcf larger than its five-year average), respectively. Storage levels for all three regions remain below their year-ago and five-year average levels.

Temperatures during the storage report week were a degree warmer than the 30-year average. Temperatures in the Lower 48 states averaged 66.4 degrees for the week, 1.1 degrees warmer than the 30-year normal temperature and 1.3 degrees warmer than during the same period last year. There were 31 population-weighted cooling degree days during the storage report week, 2 higher than the 30-year normal and 4 higher than the same period last year.

See also:

| Spot Prices ($/MMBtu) | Thu, 25-Sep |

Fri, 26-Sep |

Mon, 29-Sep |

Tue, 30-Sep |

Wed, 1-Oct |

|---|---|---|---|---|---|

| Henry Hub |

3.88 |

3.90 |

4.02 |

4.14 |

4.14 |

| New York | 1.88 |

1.73 |

2.06 |

2.12 |

2.24 |

| Chicago | 3.89 |

3.92 |

4.08 |

4.09 |

4.10 |

| Cal. Comp. Avg,* |

4.09 |

4.09 |

4.21 |

4.26 |

4.25 |

| Futures ($/MMBtu) | |||||

| October Contract | 3.971 |

3.984 |

Expired |

Expired |

Expired |

| November Contract | 4.014 |

4.029 |

4.154 |

4.121 |

4.023 |

| December Contract | 4.097 |

4.114 |

4.227 |

4.190 |

4.089 |

| *Avg. of NGI's reported prices for: Malin, PG&E citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. Natural Gas Supply - Gas Week: (9/24/14 - 10/1/14) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| Gross Production | 7.60%

|

0.17%

|

| Dry Production | 7.52%

|

0.17%

|

| Canadian Imports | -5.74%

|

-1.43%

|

| West (Net) | -15.16%

|

1.84%

|

| MidWest (Net) | 15.79%

|

-6.20%

|

| Northeast (Net) | 225.92%

|

-15.97%

|

| LNG Imports | -94.26%

|

-83.39%

|

| Total Supply | 6.21%

|

-0.03%

|

| Source: BENTEK Energy LLC | ||

| U.S. Consumption - Gas Week: (9/24/14 - 10/1/14) | ||

|---|---|---|

Percent change for week compared with: |

||

last year |

last week |

|

| U.S. Consumption | 3.4%

|

-1.4%

|

| Power | 8.9%

|

0.1%

|

| Industrial | 2.1%

|

-1.0%

|

| Residential/Commercial | -3.7%

|

-4.8%

|

| Total Demand | 3.7%

|

-1.6%

|

| Source: BENTEK Energy LLC | ||

| Rigs | |||

|---|---|---|---|

Fri, September 26, 2014 |

Change from |

||

last week |

last year |

||

| Oil Rigs | 1,592 |

-0.56% |

16.89% |

| Natural Gas Rigs | 338 |

2.74% |

-10.11% |

| Miscellaneous | 1 |

0.00% |

-83.33% |

| Rig Numbers by Type | |||

|---|---|---|---|

Fri, September 26, 2014 |

Change from |

||

last week |

last year |

||

| Vertical | 373 |

-1.32% |

-10.55% |

| Horizontal | 1,347 |

0.45% |

24.15% |

| Directional | 211 |

-0.47% |

-12.81% |

| Source: Baker Hughes Inc. | |||

| Working Gas in Underground Storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (bcf) |

||||

| Region | 2014-09-26 |

2014-09-19 |

change |

|

| East | 1,714 |

1,646 |

68 |

|

| West | 453 |

445 |

8 |

|

| Producing | 933 |

897 |

36 |

|

| Total | 3,100 |

2,988 |

112 |

|

| Source: U.S. Energy Information Administration | ||||

| Working Gas in Underground Storage | |||||

|---|---|---|---|---|---|

Historical Comparisons |

|||||

Year ago (9/26/13) |

5-year average (2009-2013) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 1,792 |

-4.4 |

1,886 |

-9.1 |

|

| West | 528 |

-14.2 |

497 |

-8.9 |

|

| Producing | 1,153 |

-19.1 |

1,116 |

-16.4 |

|

| Total | 3,473 |

-10.7 |

3,499 |

-11.4 |

|

| Source: U.S. Energy Information Administration | |||||

| Temperature -- Heating & Cooling Degree Days (week ending Sep 25) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 58

|

14

|

8

|

0

|

-1

|

0

|

||

| Middle Atlantic | 35

|

1

|

-5

|

3

|

-4

|

3

|

||

| E N Central | 37

|

-1

|

-4

|

2

|

-6

|

-9

|

||

| W N Central | 25

|

-15

|

-5

|

16

|

4

|

2

|

||

| South Atlantic | 15

|

3

|

0

|

47

|

-5

|

-1

|

||

| E S Central | 11

|

-1

|

3

|

40

|

1

|

-5

|

||

| W S Central | 2

|

-2

|

0

|

74

|

5

|

2

|

||

| Mountain | 4

|

-40

|

-25

|

53

|

21

|

20

|

||

| Pacific | 2

|

-13

|

-5

|

40

|

15

|

23

|

||

| United States | 21

|

-6

|

-5

|

31

|

2

|

4

|

||

|

Note: HDD = heating degree-day; CDD = cooling degree-day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-Day Mean ending Sep 25, 2014

Source: NOAA/National Weather Service

Deviation between average and normal (°F)

7-Day Mean ending Sep 25, 2014

Source: NOAA/National Weather Service