Analysis of Octane Costs: November 28, 2018

Introduction

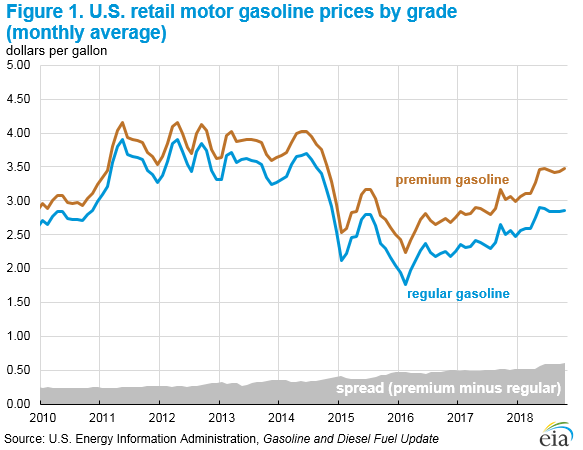

In 2017, the U.S. average retail premium gasoline price was $0.50 per gallon (gal) more than the price of regular gasoline. The difference between premium gasoline and regular gasoline prices began to increase in approximately 2010. The cause of this price spread may be the result of a change in U.S. refinery operations or retail gasoline pricing dynamics. The U.S Energy Information Administration (EIA) commissioned this study (Phase 1: Analysis of Gasoline Octane Costs and Phase 2: Future Gasoline Octane Scenarios) to examine the possible changes in U.S. refinery operations that would result in the increasing price differential between premium gasoline and regular retail gasoline prices since 2010. This study is not an examination of pricing dynamics of retail motor gasoline markets.

Phase 1 of this study examines the components of motor gasoline, motor gasoline properties and specifications, refining processes to produce motor gasoline, motor gasoline consumption, and motor gasoline production trends between 2010 and 2016. Phase 2 of this report models possible outcomes of a change in motor gasoline octane requirements and changes in demand for octane.

To assess octane costs, this study examines trends at the national, the Petroleum Administration for Defense District (PADD), and the regional wholesale market levels. The market for motor gasoline is global, and the U.S. gasoline market is interconnected with the global gasoline market through imports and exports. To that end, this study includes a supplementary analysis of international gasoline markets to identify gasoline pricing trends similar to those occurring in the United States.

This study is written for an audience already generally familiar with refining, motor gasoline markets, and petroleum chemistry terms.

EIA retained Baker & O’Brien, Inc. to analyze the factors and conditions resulting in the increasing price spread between premium and regular gasoline. Baker & O’Brien used its PRISM™ Refining Industry Analysis modeling system to conduct this study. The PRISM model is based on publicly available information and uses Baker & O’Brien's industry experience and knowledge. No proprietary or confidential refining company information is solicited or included in the PRISM modeling results. The results are estimates, and actual outcomes could vary.

The opinions and findings in this report are based on Baker & O’Brien’s experience, expertise, skill, research, analysis, and related work to date. Forecasts and projections in this report are the result of Baker & O’Brien’s best judgment and are inherently uncertain because of the potential impact of factors or future events that are unforeseeable or beyond Baker & O’Brien’s control. If additional information should become available (that is, information material to the conclusions presented in this report), Baker & O’Brien has reserved the right to supplement or amend this report. Nothing in this report should be used or construed as a recommendation for or against implementing any policies or regulations.

Executive summary

In the United States, since approximately 2010, the price difference between regular gasoline with an octane rating, or Anti–Knock Index (AKI), of 87, and premium gasoline with an AKI of 91 has been increasing. Between 2010 and 2017, the U.S. average retail price difference between premium gasoline and regular gasoline doubled, from approximately $0.25 per gallon (gal) to $0.50/gal. However, in the 15 years before that period, from 1995 and 2010, the U.S. average premium to regular price spread increased $0.05/gal.

Gasoline is a complex mixture of liquid hydrocarbons used as a fuel in internal combustion engines. Gasoline has many different attributes and specifications. Of those specifications, a gasoline’s octane rating, which measures the fuel’s ability to withstand compression without pre–igniting, is what separates different grades of gasoline at the retail level.

Motor gasoline is the predominant fuel for light duty vehicles in the United States. In 2017, U.S. product supplied for motor gasoline, a proxy for consumption, was 9.3 million barrels per day.

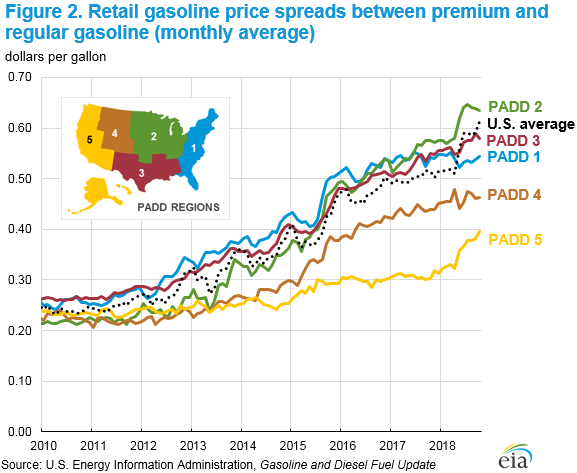

The increasing spread between premium gasoline and regular gasoline has occurred in all Petroleum Administration for Defense Districts (PADD) across the country–but to varying degrees. The gasoline price spread between premium and regular gasoline is largest in the Midwest (PADD 2) with an average difference of $0.56/gal in 2017, up $0.34/gal from 2010. The price difference between premium and regular gasoline on the West Coast (PADD 5) grew the least, up $0.08/gal, from $0.23/gal in 2010 to $0.31/gal in 2017.

Phase 1: Analysis of gasoline octane costs

This section examines the possible causes for the increasing premium–to–regular price spread related to the production of motor gasoline and its components at refineries in the United States. To that end, EIA retained Baker & O’Brien to analyze the factors and conditions at refineries that could result in the increasing spread.

Baker & O’Brien’s analysis concludes that the increasing premium–to–regular gasoline retail price spread is not the result of a change in the cost to produce higher octane gasoline at U.S. refineries.

Baker & O’Brien’s analysis centered on reformer units at U.S. refineries. Reformer units convert low–octane naphtha into the high–octane gasoline blendstock reformate. Reformer units are one of the primary determinants in the incremental costs of producing octane.

Because U.S. production of mostly light–sweet crude oil from shale formations has increased since 2010, domestic refineries have increased the share of light–sweet domestic crude oil they process. Many of the light–sweet shale crude oils yield larger portions of naphtha and other low–octane gasoline blendstocks when processed at refineries. As a result, U.S. refinery net production of naphthas and lighter oils has increased since 2012.

The increased supply of naphtha has, in turn, decreased the cost of feedstocks (naphtha) for reformer units at U.S. refineries. With lower feedstock costs, U.S. refiners have increased reformer throughputs and slightly increased reformer severity, converting the surplus naphtha supplies into high–octane gasoline components.

Baker & O’Brien’s analysis found that the increased supply of high octane components from increased reformer throughputs and severity caused the spread between regular gasoline and premium gasoline at the wholesale (spot) level to narrow. Excluding a few brief periods of higher octane spreads as a result of temporary conditions, such as refinery outages, a narrowing spot market spread between regular and premium gasoline prices started in 2013 and has continued through the study period. A narrowing price spread between regular gasoline and premium gasoline in the spot market, or the first point of sale after being produced in a refinery, indicates decreasing costs of producing octane at U.S. refineries, not increasing.

Further analysis of regular gasoline and premium gasoline prices at the rack, or distribution terminal level just before delivery to retail stations, also failed to find any significant change since 2010 to account for the increasing regular–to–premium retail gasoline price spread.

Baker & O’Brien also analyzed changes in demand, or consumption, patterns that may explain the increasing regular–to–premium retail gasoline price spread. After accounting for increased ethanol blending, Baker &O’Brien found that, although U.S. gasoline consumption has been increasing since 2012, consumption of petroleum–based quantities of gasoline was lower in 2016 than at the 2007 peak. As a result, Baker & O’Brien concludes that no major shifts in U.S. gasoline consumption have occurred, and consumption shifts were unlikely to have been significant contributing factors in the increasing premium–to–regular retail gasoline price differential.

In addition to overall gasoline consumption trends, Baker & O’Brien also examined changes in demand of the different grades of gasoline as a result of changing vehicle designs. As vehicle manufacturers have modified engine designs to increase efficiency, one trend has been to increase compression ratios using turbochargers. Engines with higher compression ratios typically require higher octane gasoline than those with lower compression ratios. However, Baker & O’Brien found the changing engine design trends have not yet had a significant effect on the share of vehicles requiring premium gasoline in the light-duty vehicle fleet. Therefore, changing engine design trends to more car models requiring premium gasoline or higher octane gasoline does not appear to have been a significant contributing factor in the premium–to–regular retail gasoline price differential.

To determine if the widening retail price spread between regular and premium gasoline was unique to the United States, Baker & O’Brien examined international gasoline markets and found no similar pricing dynamic in other markets.

Baker & O’Brien identified two factors not included in the scope of this study but could be contributing to a widening regular–to–premium gasoline retail price spread.

One factor could be different asymmetrical price movement tendencies between regular gasoline and premium gasoline prices. The theory is a variation on the rockets and feathers hypothesis (Bacon, 1991) of asymmetric petroleum product pricing, where regular prices and premium gasoline prices both increase at similar speeds, but premium prices fall slower than regular gasoline prices.

A second possible contributing factor is the search and adjustment cost theory, which contends that the consumer could have less price transparency for premium gasoline prices compared with regular gasoline prices. Less price transparency leads to higher search costs to discover the most competitive premium gasoline prices compared to regular gasoline. The higher search costs possibly explain why premium gasoline prices fall more slowly than regular gasoline prices. Baker & O’Brien cites evidence supporting this theory from the Los Angeles gasoline market where retailers are legally required to post prices of all grades of gasoline for sale and where essentially no change occurred in the regular to premium price differential during the study period.

Phase 2: Future gasoline octane scenarios

In Phase 2, Baker & O’Brien analyzed whether or not the U.S. domestic refining industry would be capable of meeting higher octane demand if the octane requirements for retail gasoline increased. The scenario assumes that, beginning with model year 2023, all light–duty vehicles in the United States will require a minimum 95 research octane number (RON) gasoline. Because vehicle model years are ahead of the calendar year, the study also assumes that U.S. refineries would be required to make 95 RON gasoline by January 1, 2022. Baker & O’Brien modeled U.S. gasoline markets and octane requirements in 2027 as a result of this change.

Baker & O’Brien concluded that, in 2022, no significant changes in refinery configuration or throughput would be required to meet the minimum 95 RON gasoline requirement. Consumption of 95 RON gasoline would increase as the U.S. light–duty vehicle fleet changes to include more vehicles that require the 95 RON gasoline. Baker & O’Brien concluded that 29% of total gasoline consumption would be 95 RON by 2027. Baker & O’Brien found that existing U.S. refineries would be able to supply the increased octane requirements in 2027 with minor operational adjustments through a combination of a projected decline in U.S. gasoline consumption based on EIA’s 2018 Annual Energy Outlook and increased reformer severity.