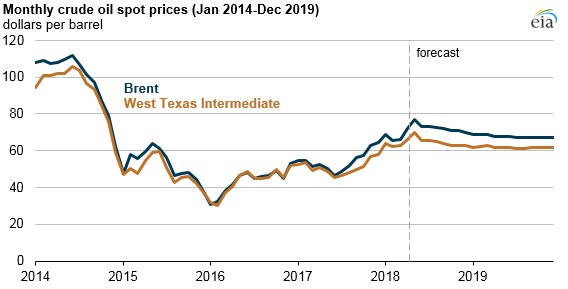

EIA expects Brent crude prices will average $71 per barrel in 2018, $68 per barrel in 2019

In the June 2018 update of its Short-Term Energy Outlook (STEO), EIA forecasts Brent crude oil prices will average $71 per barrel (b) in 2018 and $68/b in 2019. The updated 2019 forecast price is $2/b higher than in the May STEO. Brent crude oil spot prices averaged $77/b in May, an increase of $5/b from April and the highest monthly average price since November 2014. West Texas Intermediate (WTI) prices are forecast to average almost $7/b lower than Brent prices in 2018 and $6/b lower in 2019.

Crude oil prices have reached high levels as global oil inventories have generally declined from January 2017 through April 2018. Even though the 2019 oil price forecast is higher than it was in the May STEO, EIA expects oil prices to decline in the coming months because global oil inventories are expected to rise slightly during the second half of 2018 and in 2019.

Expected inventory growth results from forecast oil supply growth outpacing forecast oil demand growth in 2019. EIA currently forecasts global petroleum and other liquids inventories will increase by 210,000 barrels per day (b/d) next year, a factor that, all else being equal, typically puts downward pressure on oil prices.

Most of the growth in global oil production in the coming months is expected to come from the United States. EIA projects that U.S. crude oil production will average 10.8 million b/d for full-year 2018, up from 9.4 million b/d in 2017, and will average 11.8 million b/d in 2019. If the 2018 and 2019 forecast annual averages materialize, they would be the highest levels of production on record, surpassing the previous record set in 1970.

Tight oil production in the Permian region of West Texas and New Mexico is the main driver of rising U.S. production. Among other countries outside of the Organization of the Petroleum Exporting Countries (OPEC), Canada and Brazil are also expected to experience significant growth in oil production in 2019.

EIA expects that OPEC crude oil production will average 32.0 million b/d in 2018, a decrease of about 0.4 million b/d from the 2017 level. Total OPEC crude oil output is expected to increase slightly in 2019 to an average of 32.1 million b/d. The 2018 and 2019 levels are 0.2 million b/d and 0.3 million b/d lower, respectively, than forecast in the May STEO, reflecting revised expectations of crude oil production in Venezuela and Iran. The lower OPEC forecast is one of the main reasons EIA expects oil prices to be slightly higher in 2019 compared with last month’s forecast.

OPEC, Russia, and other non-OPEC countries will meet on June 22 to assess current oil market conditions associated with their existing crude oil production reductions. Current reductions are scheduled to continue through the end of 2018. Oil ministers from Saudi Arabia and Russia have announced that they will re-evaluate the production reduction agreement given accelerated output declines from Venezuela and uncertainty surrounding Iran’s production levels.

In the June STEO, EIA assumes declining Venezuelan and Iranian crude oil production in 2019 will be offset by increasing production from Persian Gulf producers, primarily Saudi Arabia. Depending on the outcome of the June 22 meeting, however, the magnitude of any supply response is uncertain. Overall, EIA expects global oil production to increase by almost 2.0 million b/d in 2019 compared with forecast oil demand growth of 1.7 million b/d.

Principal contributors: Tim Hess, Hannah Breul

Tags: Brent, liquid fuels, crude oil, oil/petroleum, OPEC