United States remains the world’s top producer of petroleum and natural gas hydrocarbons

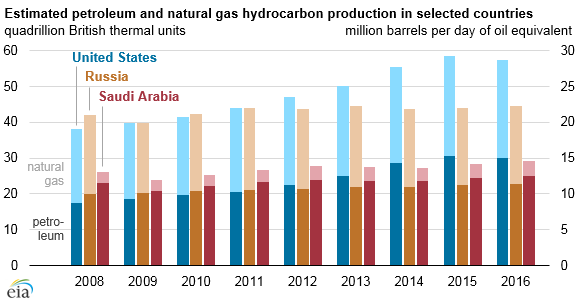

The United States remained the world's top producer of petroleum and natural gas hydrocarbons in 2016 for the fifth straight year despite production declines for both petroleum and natural gas relative to their 2015 levels. The United States has been the world's top producer of natural gas since 2009, when U.S. natural gas production surpassed that of Russia, and it has been the world's top producer of petroleum hydrocarbons since 2013, when its production exceeded Saudi Arabia’s.

For the United States and Russia, total petroleum and natural gas hydrocarbon production in energy content terms is almost evenly split between petroleum and natural gas, while Saudi Arabia's production heavily favors petroleum. Total petroleum production is made up of several different types of liquid fuels, including crude oil and lease condensate, tight oil, extra-heavy oil, and bitumen. In addition, various processes produce natural gas plant liquids (NGPL), biofuels, and refinery processing gain, among other liquid fuels.

In the United States, crude oil and lease condensate accounted for roughly 60% of total petroleum hydrocarbon production in 2016. In Saudi Arabia and Russia, this share is much greater, as those countries produce lesser amounts of natural gas plant liquids, and they also have much smaller volumes of refinery gain and biofuels production. U.S. petroleum production fell by 300,000 barrels per day in 2016, as a result of relatively low oil prices.

With rapid growth in natural gas production through 2015 and a very mild 2015–2016 winter that reduced demand for natural gas as a heating fuel, average U.S. natural gas prices in 2016 were at their lowest level since 1999. Despite a modest recovery in prices later in the year, natural gas production decreased by 2.3 billion cubic feet per day in 2016.

Russian hydrocarbon production has been rising as capital expenditure spending on exploration and production increased. Russia also has favorable tax regimes and exchange rates (Russian company expenditures are in Russian Rubles, but oil sales are in U.S. Dollars) that resulted in record levels of Russian petroleum production in the second half of 2016. Russian natural gas production also rose in 2016, in part to meet growth in European natural gas demand. In 2016, natural gas demand increased by an estimated 6% in European countries that are members of the Organization for Economic Cooperation and Development (OECD).

In contrast to past actions to raise or lower oil production levels to balance global oil markets, Saudi Arabia did not reduce its petroleum production between late 2014 and 2016 in an effort to defend its market share, even as prices remained low and world oil inventories continued to grow. In 2016, Saudi Arabia's total petroleum and natural gas hydrocarbon production rose by 3%.

In EIA’s June Short-Term Energy Outlook (STEO), U.S. petroleum and other liquid fuels production is expected to increase, reaching 15.6 million barrels per day (b/d) in 2017 and 16.7 million b/d in 2018, up from 14.8 million b/d in 2016.

The June STEO forecasts Russian liquid fuels production to average 11.18 million b/d over 2017 and 2018, close to the 2016 production of 11.24 million b/d. The STEO provides a production forecast for members of OPEC as a whole rather than for individual OPEC countries. OPEC liquid fuels production, which was 39.0 million b/d in 2017, is forecast to be 39.2 million b/d in 2017 and 39.9 million b/d in 2018. This outlook takes into account recent agreements among OPEC member countries, as well as pledges by key non-OPEC producers, including Russia, to restrain production. In November 2016, OPEC had agreed to production cuts that would last through the first half of 2017. At their May 25 meeting, OPEC agreed to extend these cuts through March 2018.

Principal contributor: Linda Doman