United Kingdom increases oil production in 2015, but new field development declines

After many years of decline, production of petroleum and other liquids in the United Kingdom (U.K.) increased by about 100,000 barrels per day (b/d) in 2015. The largest contribution to this increase came from fields that were brought online in the second half of 2014. Significant increases also came from fields that came online in 2015, and from improved performance of the U.K.'s largest producing field, the offshore Buzzard field. A similar year-over-year increase in production volumes hasn't occurred since 1998, when petroleum and other liquids production grew by slightly more than 100,000 b/d.

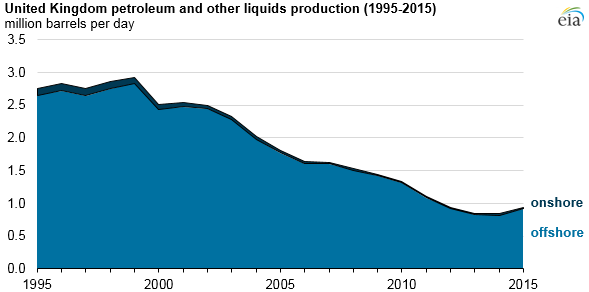

The U.K. is the second-largest liquids producer in Europe (after Norway), producing one million b/d in 2015. This amount is large among European countries but small in the global market, and the U.K. remains a net importer of petroleum and other liquids. More than 97% of its liquids production in 2015 came from offshore fields, where petroleum development projects have long lead times. The majority of the offshore crude and condensate fields that began production in 2015 were approved in 2012 or earlier when oil prices were much higher.

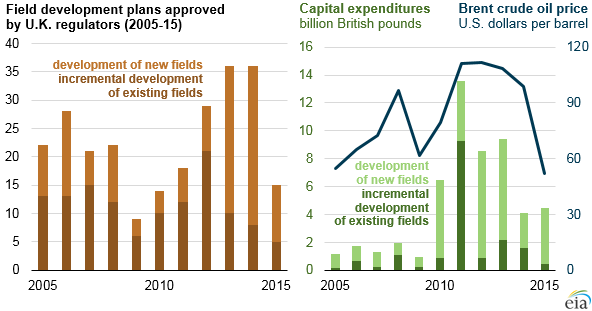

In response to current low oil prices, U.K. producers have begun to slow plans for new development. Given the long lead times associated with offshore production, this will likely have ramifications in the two-to-five year timeframe (2018-21). In the U.K., project developers must receive governmental approval of their field development plans (FDP) prior to developing a field. The number of FDPs approved in 2015 was less than half the number approved in 2013 or 2014. Additionally, although the number of FDPs approved in 2014 was similar to the number approved in 2013, the investment associated with the fields approved in 2014 was much lower.

The current lull in both new field approvals and incremental development approvals could lead to significant production declines in the United Kingdom in 2018 and beyond. However, in 2016 and 2017, several already-approved fields where investment is already committed are expected to begin production, at least partially offsetting production declines from existing fields.

For more analysis of the U.K.'s energy sector, see EIA's recently released Country Analysis Brief on the United Kingdom.

Principal contributor: Justine Barden