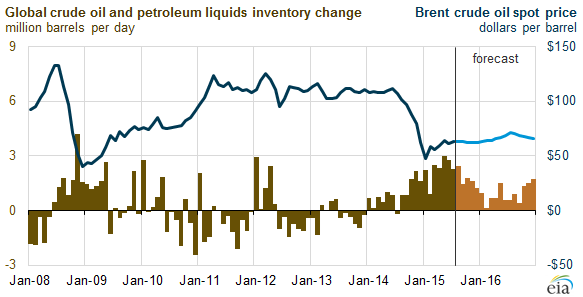

Growing global liquids inventories reflect lower crude oil prices

Continued growth in global production of petroleum and other liquids has outpaced consumption growth since August 2014, resulting in rising global liquids stocks. Total global liquids inventories are estimated to have grown by 2.3 million barrels per day (b/d) through the first seven months of 2015, the highest level of inventory builds through July of any year since 1998. These strong inventory builds have put significant downward pressure on near-term crude oil prices: North Sea Brent crude oil spot prices have averaged $58/barrel through July of this year compared to $109/b over the same period in 2014, responding to growth in global inventories.

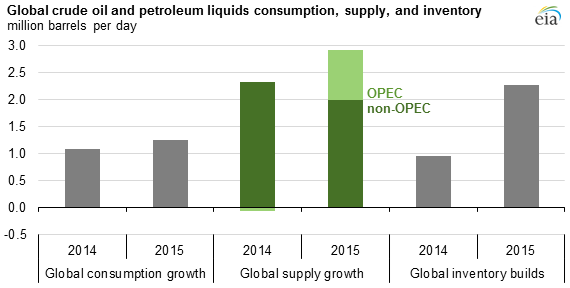

EIA estimates global consumption of petroleum and other liquids grew by 1.1 million b/d in 2014, averaging 92.4 million b/d for the year. Through July 2015, global liquids consumption has grown by an additional 1.2 million b/d. Global production of petroleum and other liquids has been higher, growing by 2.3 million b/d in 2014, averaging 93.3 million b/d for the year, and increasing by an estimated additional 2.9 million b/d through July 2015.

Although the annual increases in global crude oil and liquids production have been similar, the sources of supply have been different. In 2014, most global liquids production growth was from countries outside of the Organization of the Petroleum Exporting Countries (OPEC), particularly the United States, while production from OPEC actually fell. In contrast, growth thus far in 2015 has come from both OPEC and non-OPEC countries. Through the first seven months, EIA estimates that non-OPEC petroleum and other liquids production has grown by an average of 2.0 million b/d, while OPEC liquids production is estimated to have grown by 0.9 million b/d over the same period.

Growing oil inventories typically put downward pressure on near-term prices and increase contango in the futures market, meaning contracts for delivery in the future show higher prices than contracts in the near term. Since global liquids inventories began to consistently grow in the third quarter of last year, the difference between futures prices and near-term contracts has increased from nearly zero to $5/b-$10/b over the past year, reflecting the increased supply of crude oil and the associated costs of growing storage needs in the near term as well as the expectation of reduced oil supply growth in future months. Over the same period, Brent crude oil spot prices have fallen from an average of $102/b in August 2014 to a range between $55/b and $65/b for six consecutive months between February and July in 2015.

In the August Short-Term Energy Outlook (STEO), EIA forecasts that falling crude oil production in the United States in response to lower oil prices will help moderate oil inventory builds in the coming months, leading to slightly higher expected prices. The pace of inventory accumulation is expected to slow from more than 2.0 million b/d currently to 1.5 million b/d in the fourth quarter of 2015, and to drop below a 1.0 million b/d build in 2016. Expectations for a continuation in this trend should be reflected in increasing Brent crude oil spot prices, which are forecast in STEO to increase from an average of $51/b in the fourth quarter of this year to an average of $59/b in 2016.

Principal contributor: Sean Hill