Energy reform could increase Mexico’s long-term oil production by 75%

On August 11, Mexico's president signed into law legislation that will open its oil and natural gas markets to foreign direct investment, effectively ending the 75-year-old monopoly of state-owned Petróleos Mexicanos (Pemex). These laws, which follow previously adopted changes in Mexico's constitution to eliminate provisions that prohibited direct foreign investment in that nation's oil and natural gas sector, are likely to have major implications for the future of Mexico's oil production profile. As a result of the developments in Mexico over the past year, EIA has revised its expectations for long-term growth in Mexico's oil production.

Although there are many complexities to the new reform and many details that still must be settled before the reforms can take effect, reform is expected to improve the long-term outlook for growth in Mexico's petroleum and other liquids production. Analysis in EIA's upcoming International Energy Outlook 2014 (IEO2014) will include the potential effects on upstream oil exploration and production and the potential for foreign participation.

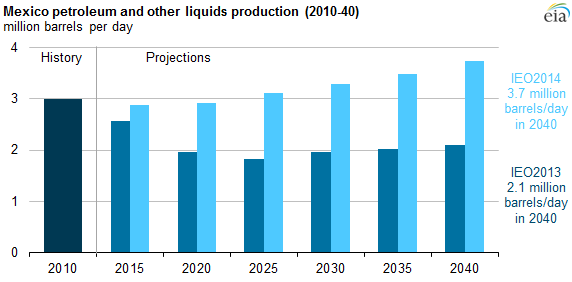

The changes in EIA's assessment of Mexico's liquids production profile are profound. Last year's International Energy Outlook projected that Mexico's production would continue to decline from 3.0 million barrels per day (MMbbl/d) in 2010 to 1.8 MMbbl/d in 2025 and then struggle to remain in the range of 2.0 to 2.1 MMbbl/d through 2040. The forthcoming Outlook, which assumes some success in implementing the new reforms, projects that Mexico's production could stabilize at 2.9 MMbbl/d through 2020 and then rise to 3.7 MMbbl/d by 2040—about 75% higher than in last year's outlook. Actual performance could still differ significantly from these projections because of the future success of reforms, resource and technology developments, and world oil market prices.

Since 2008, the contract structure for any private company partnering with Pemex was a performance-based service contract, which offered financial incentives to private contractors working in Mexico's upstream sector. Incentives were provided in some cases, such as when a project is completed ahead of schedule, when Pemex benefits from the use of new technology provided by the contractor, or when the contractor is more successful than originally expected. These contracts also include penalties for environmental negligence or failure to meet contractual obligations.

Mexico's legislation introduced three new contract types that will provide more opportunity for foreign investment in its energy sector:

- Profit-sharing contracts allow companies to receive a percentage of the profits resulting from oil and natural gas development. While companies entering into these contracts would not own the resources being developed, they would be allowed to include the revenue from their part of the estimated future profits.

- Production-sharing contracts allow companies to own title to a percentage of resource volumes as they are produced.

- Licenses allow participating companies to be paid in the form of oil and natural gas extracted from each project.

The production-sharing contracts and licenses will effectively allow foreign companies to account for reserves, which is a particularly attractive incentive for investment in Mexico's energy sector. Different contract types will likely be applied according to the degree of risk associated with specific projects. For instance, licenses will likely be used for projects that are very capital intensive and high-risk, requiring advanced technology, like oil shale or ultra-deepwater projects. Less risky onshore and shallow offshore projects would more likely use profit-sharing arrangements.

More details on EIA's projections for Mexico's oil production will be available with the release of the International Energy Outlook 2014.

Principal contributors: Linda Doman, Laura Singer