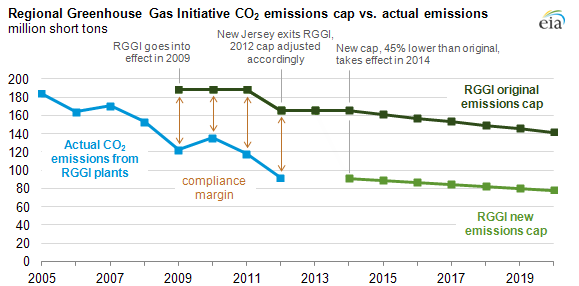

Lower emissions cap for Regional Greenhouse Gas Initiative takes effect in 2014

Note: States participating in the current program include Maine, New Hampshire, Vermont, Massachusetts, Rhode Island, Connecticut, New York, Delaware, and Maryland. New Jersey withdrew from the RGGI program in 2012. As a result, the program cap and associated emissions declined starting in 2012.

Republished February 4, 2014, text was modified to clarify content.

Republished February 5, 2014, text was modified to clarify content.

Last year, the nine states participating in the Regional Greenhouse Gas Initiative (RGGI) cap-and-trade program for carbon dioxide (CO2) decided to lower the program's emissions cap by 45% starting in 2014. RGGI is intended to limit CO2 emissions from electric power plants in the Northeast.

When it took effect in 2009, RGGI became the first mandatory CO2 cap-and-trade program in the United States. The cap was tightened primarily because actual CO2 emissions in the region since 2009 have been roughly 35% below the cumulative cap. This lower level of emissions is primarily attributed to low natural gas prices, which have shifted a large share of electricity generation in the region toward natural gas, and to lower overall electricity demand.

RGGI covers fossil-fueled electric power plants greater than 25 megawatts (MW) located in any of the nine participating states. CO2 emissions in the RGGI region accounted for 4% of the total emissions from the electric power sector in the United States in 2012. RGGI is one of the two legally mandated CO2 reduction programs in the United States, the other being a California cap-and-trade statute.

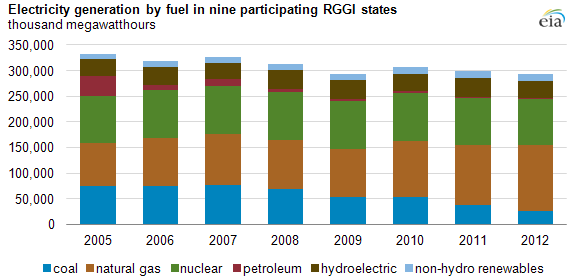

In 2005, which is when CO2 emissions in the RGGI states reached a peak, coal accounted for 23% of the regional generation mix and petroleum accounted for 12%. By 2012, coal's share had declined to 9%, while the natural gas share had risen from 25% share in 2005 to 44%. Petroleum's generation share in the region fell below 1% by 2012.

Note: States participating in the current program include Maine, New Hampshire, Vermont, Massachusetts, Rhode Island, Connecticut, New York, Delaware, and Maryland. This figure does not include New Jersey, which withdrew from the program in 2012.

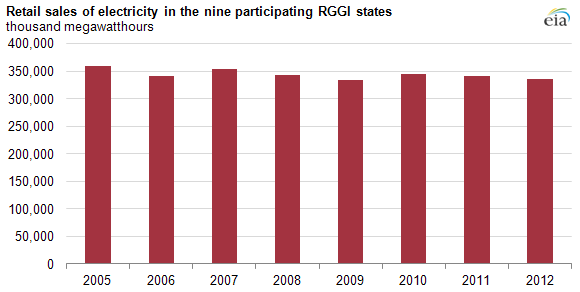

At the same time the shift in fuels for electricity generation began lowering the carbon intensity of electricity in the region, demand for electricity in the Northeast became stagnant or started declining. Average annual retail electricity sales in the nine participating states from 2009 through 2012 were 6% below the annual sales in 2005.

Note: States participating in the current program include Maine, New Hampshire, Vermont, Massachusetts, Rhode Island, Connecticut, New York, Delaware, and Maryland. This figure does not include New Jersey, which withdrew from the program in 2012.

Despite the reduction in the cap beginning in 2014, it remains to be seen whether the updated program caps will result in significant emissions reductions compared to the outcomes that might occur absent the new caps. CO2 emissions in 2012 in the participating states were still only 92 million short tons, close to the 2014 target cap of 91 million short tons. However, the cap is designed to tighten annually through 2020. CO2 emissions from coal-fired generation were up both in the RGGI region and nationally in the first half of 2013, compared with 2012 levels, which indicates that the new RGGI cap could become more binding in the future.

Because of a surplus of allowances obtained via auction during the initial years of RGGI, the value of these allowances remained close to the program's price floor of $1.93/ton of CO2 allowed in each quarterly auction. The value of allowances increased slightly to $3.00/ton of CO2 in the latest auction, with market participants possibly anticipating a rise in the future value of allowances. RGGI states use allowance revenues for a variety of programs that support cleaner generation and/or energy efficiency programs that reduce demand. Unless the supported programs using RGGI auction revenues would be funded at the same level using other funding sources in the absence of RGGI, these programs provide a tangible incremental reduction in emissions.

The RGGI program allows unused allowances from the early years of the program to be saved and applied after 2014, a strategy often referred to as banking allowances. Additional flexibility exists in the program through the recently created Cost Containment Reserve. When the price hits a given level, program participants can purchase additional allowances beyond the annual cap. This is intended to moderate the increase in prices when demand is higher than expected. The price trigger starts at $4/ton of CO2 in 2014 and rises to $10/ton of CO2 in 2017.

The program also allows for the limited use of CO2 offsets, which are reductions in emissions from activities not subject to the RGGI cap, as a compliance option. RGGI program participants may cover 3.3% of their emissions using offsets. Although the RGGI caps have been lowered, it remains uncertain how much the new caps will affect generation choices and related emissions.

Principal contributor: Mike Leff