U.S. natural gas spot prices increased during first-half 2013

Republished: July 22, 2013, 11:00 a.m.: To update a link in the text.

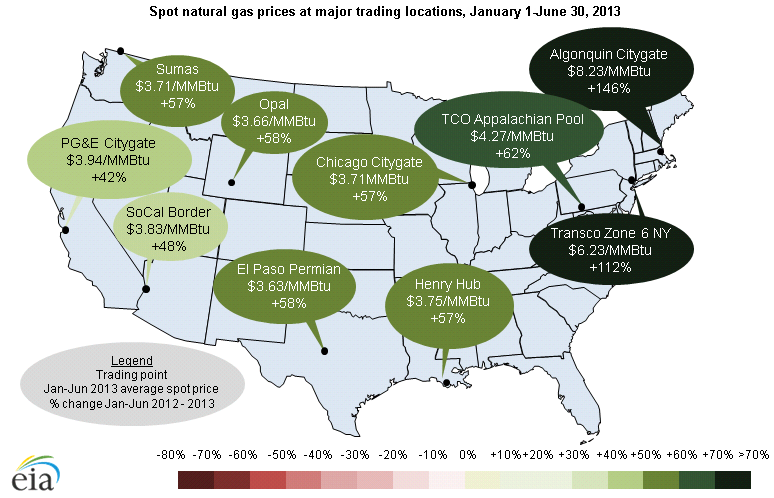

Note: Spot prices on the map reflect averages of daily prices from the first half of 2013, January 1 through June 30. The percentage change reflects the difference in the average price of natural gas by trading point for the first six months of 2013 compared to the first six months of 2012 divided by the average natural gas price by trading point for the first six months of 2012.

Note: Click to enlarge.

Average spot natural gas prices at most major trading points increased 40% to 60% during the first half of 2013 compared to the same period in 2012, as demand for natural gas rose faster than increases in supply. Price increases were relatively uniform throughout the country, with the exception of New England and New York, where supply constraints caused spot prices to spike when demand peaked this winter. Price differences between Henry Hub and most western trading hubs averaged less than 10 cents per million British thermal units (MMBtu).

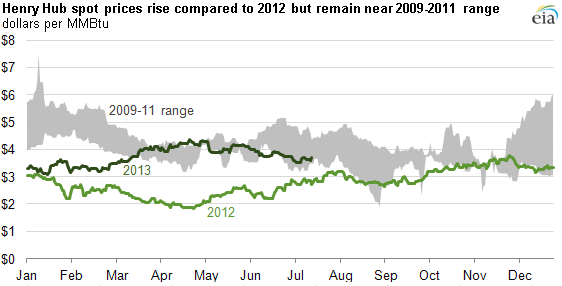

Natural gas spot prices at Henry Hub—a key benchmark and major trading location—averaged $3.75/MMBtu during the first half of 2013, up 57% from the $2.39/MMBtu average spot price for the first half of 2012. However, this year-over-year price increase principally reflected the extremely low prices in 2012. Spot prices so far in 2013 are very similar to levels seen in 2009 to 2011 (see chart below).

Specific factors contributed to the return of natural gas prices closer to the $4.00 per MMBtu range. These include:

- Colder winter temperatures compared to a year ago, with declining power burn. Overall, natural gas consumption was up by more than 3% through the first half of this year. A 5.6 billion cubic feet per day (Bcf/d) combined increase in residential, commercial, and industrial consumption more than compensated for a 3.3 Bcf/d decline in power sector consumption. As a result, total demand rose faster than total supply, which contributed to upward pressure on prices.

A return to more seasonal winter temperatures following an abnormally warm winter in 2011-12 drove residential and commercial consumption 20% above year-ago levels during the first half of 2013, and contributed to price spikes for natural gas and power in New England early in the year. Although power sector natural gas consumption was 14% below last year's record levels, power burn remained higher than in many past winters and 20% above the 2007-11 January-June average. Coal recovered some of its market share as natural gas prices increased through the first half of 2013. - Natural gas production gains slowed. U.S. dry natural gas production continued to grow during the first half of 2013, albeit at a slower pace compared to prior years. According to Bentek Energy, U.S. dry natural gas production was up 1.8% during the first 6 months of 2013 compared to increases of 5.6% and 7.3% during the first halves of 2012 and 2011, respectively. Significant production gains that began in 2010 as a result of rapid growth in supply from shale basins began to slow at the beginning of 2012, largely in response to lower prices. Slowing production growth continued through the first half of 2013, limiting the overhang of supply and resulting in rising prices. Production growth continued in the Appalachian Basin's Marcellus Shale play—increasing around 50% during the first six months of 2013, compared to the first six months of 2012—and boosted production levels in Pennsylvania.

- Storage inventories decreased below five-year average levels. Large withdrawals of Lower 48 natural gas storage inventories at the end of March pushed stocks below their five-year average levels for the first time since August 2011. This year's cold March temperatures led to high inventory drawdowns that month. The cold weather and high withdrawals persisted well into April, when net storage injections would normally begin to take place. Bigger withdrawals from storage counter-balanced higher total natural gas demand, which was only partially offset by slightly rising dry natural gas production, and as a result inventories fell.

Despite relatively high injections during May and June, storage levels have remained below their five-year average, supporting gas prices in the $4.00/MMBtu range. The Short-Term Energy Outlook projects that Lower 48 working inventories will reach 3,809 Bcf by the end of the injection season on October 31, 2013, with injection levels similar to those in 2008-11 but much higher than in 2012.