Exports and Imports

Exports

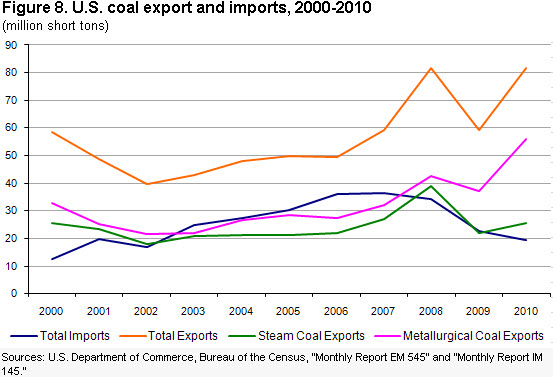

Total U.S. coal exports for 2010 increased by 38.3 percent to 81.7 million short tons (Figure 8).

Figure Data This increase was largely due to two factors. First, heavy rains and flooding in Australia, Indonesia, and Colombia reduced world coal supply and forced many coal importing nations to look elsewhere, primarily to the United States, to fulfill their coal needs. In addition, the shortage of their own domestic coal in relation to growing needs, namely for China and India, provided ample opportunities for U.S. coal producers to export to these markets.

U.S. coke exports increased in 2010 by 11.9 percent to a total of 1.5 million short tons. Mexico received 510 thousand short tons or 34.8 percent of total U.S. coke exports, while Canada received 400 thousand short tons in 2010. Last year, Brazil and India increased their share of total U.S. coke exports by 4.9 and 2.0 percentage points, respectively. The average price of coke exports in 2010 was $167.25 per short ton, an increase of 61.7 percent from 2009.

In 2010, the average price of U.S. coal exports increased by 18.7 percent to $120.41 per short ton. Metallurgical coal exports, which accounted for 68.7 percent of total coal exports, increased by 50.6 percent to 56.1 million short tons in 2010. The average price of U.S. metallurgical coal exports grew by 23.5 percent to a level of $145.44 per short ton, an increase of $27.71 per short ton from the 2009 level. Steam coal exports increased in 2010. With a percentage change of 17.2 percent, total steam coal exports hit 25.6 million short tons. However, unlike the average price of metallurgical exports, the average price of steam coal exports dropped by 11.0 percent to $65.54 per short ton.

Nearly half of all U.S. coal exports were destined for European markets. In 2010, metallurgical coal exports to Europe increased by 49.5 percent to 29.5 million short tons. Metallurgical exports to the Netherlands, 9.7 percent of total U.S. metallurgical exports in 2010, grew to 5.4 million short tons. (Note: Most ports in the Netherlands serve as transshipment points for coal. Hence, exports to the Netherlands may be bound for other countries in the region.) In 2010, the United Kingdom and Italy were other key European destinations for U.S. metallurgical coal exports. U.S. metallurgical coal exports to the United Kingdom totaled 3.0 million short tons, an increase of 52.2 percent since the previous year. In addition, the average price per ton increased from $106.19 to $131.66. Italy received a total of 2.6 million short tons in 2010, 25.2 percent greater than total metallurgical exported to Italy in 2009. Similar to the average price of metallurgical coal exports to the United Kingdom, average price of metallurgical coal exports to Italy grew; from $116.13 per short ton to $145.39 per short ton in 2010. Furthermore, U.S. metallurgical coal exports to Ukraine, Turkey, and Poland increased by over 144 percent in 2010.

Europe is the second largest market for U.S. steam coal exports. U.S. steam coal exports to Europe have thrived because many European nations have reduced production of coal. Moreover, South Africa, a coal exporting nation, has increased exports to India and China leaving less coal to be exported to the European markets. Proximity to major European ports has contributed to export increases to Europe. However, in 2010, total steam coal exports to Europe declined by 15.6 percent to 8.8 million short tons. Last year, European nations utilized existing stockpiles of coal. Moreover, exports of steam coal to the United Kingdom, which decreased by 47.9 percent to 1.3 million short tons, were affected by subsidies provided to utilities by the British government to diversify to biomass and other renewable energy sources. France and Germany are key destinations for U.S. steam coal exports, accounting for 4.6 percent and 4.0 percent, respectively, of total U.S. steam coal exports. While exports to France declined by 2.8 percent, exports to Germany remained strong, growing at 28.5 percent.

Asian markets received 17.9 million short tons or 21.9 percent of total coal exports in 2010. This increase of 176.0 percent from 2009 exports was due primarily to a surge in sales of metallurgical coal to China, Japan, and South Korea, and sales of steam coal to China and South Korea. Total metallurgical coal exports to Asia totaled an estimated 13 million short tons in 2010, an increase of 133.0 percent from 2009, China received 4.2 million short tons or 32.4 percent of all metallurgical coal exports to Asia. South Korea remained the second largest Asian destination of U.S. metallurgical coal exports in 2010, securing 3.0 million short tons, 73.7 percent greater exports than in 2009. The average price of metallurgical coal exports to South Korea increased by 32.1 percent to $141.62. Japan and India acquired roughly 3.0 million short tons and 2.5 million short tons, respectively. The increased use of steel in Japan, the result of fiscal stimuli and export growth in 2010, is a reason for the 332.0 percent rise in metallurgical coal exports to the nation.

In 2010, steam coal exports to Asia increased dramatically by 437.6 percent from 2009 to 4.9 million short tons. As global supplies of thermal coal tightened and steam coal prices increased steadily, Asian nations, namely South Korea and China increased imports of U.S. thermal coal. South Korea remained the primary Asian destination of U.S. steam coal exports with a total of 2.8 million short tons. Additionally, steam coal exports to South Korea as a percentage of total U.S. steam coal exports increased by 8.9 percentage points. The average price of U.S. steam coal exports to South Korea was $40.54 per short ton, a decrease of 12.4 percent from the 2009 price. Exports to China increased to 1.6 million short tons from 0.2 million short tons. The average price of U.S. steam coal exports to China was $62.91 per short ton, a decrease of 13.1 percent from the 2009 price.

In 2010, total U.S. coal exports to countries in North and South America increased to 13.4 million short tons and 9.5 million short tons, respectively. Average prices per short ton increased by 10.5 percent to $77.91 per short ton and 22.4 percent to $142.09 per short ton, respectively. U.S. metallurgical coal exports to countries in North and South America increased in 2010. The greatest increase in exports was to Canada and Brazil. Canada received 3.4 million short tons, an increase of 42.6 percent from 2009, while shipments to Brazil increased by 6.1 percent to total 7.9 million short tons. The average price of metallurgical coal exports to Canada and Brazil increased to $112.25 per short ton and $155.26 per short ton, respectively.

Canada remains the single largest market for all U.S. steam coal exports. In 2010, exports to Canada, which accounts for 31.2 percent of all U.S. steam coal exports, decreased by 2.6 percent to an estimated 8.0 million short tons. However, the average price of steam coal exports to Canada increased by 2.2 percent to $59.84 per short ton. (Note: Currently, there are no major coal-exporting facilities on the U.S. west coast. Coal producers in the west coast utilize coal-export terminals in British Columbia for shipments to Asian markets.)

Total steam coal exports to South America grew from 0.7 million short tons in 2009 to 1.3 million short tons in 2010. Similar to 2009, Chile received most of U.S. export of steam coal to South America in 2010. Further, Chile increased imports of U.S. steam coal by 70.5 percent to 1.2 million short tons. The average price of steam coal exports to South America and in particular to Chile decreased in 2010.

Total coal exports to Africa increased by 42.7 percent to 2.6 million short tons. While exports of metallurgical coal to South Africa decreased to 149 thousand short tons, exports to Egypt increased by 81.6 percent to an estimated 1.1 million short tons in 2010. Average price of metallurgical coal exports to Egypt increased by 42.2 percent from 2009 to $167.25 per short ton. U.S. steam coal exports to the African continent gained by 78.0 percent in 2010, to a total of 1.3 million short tons. The majority of the increase in steam coal exports to Africa is attributable to one country, Morocco. Total steam coal exports to Morocco in 2010 were 1.1 million short tons, an increase of over 60 percent. The average price of steam coal exports to Morocco decreased in 2010 to $73.65 per short ton.

U.S. steam coal exports to the African continent gained by 78.0 percent in 2010, to a total of 1.3 million short tons. The majority of the increase in steam coal exports to Africa is attributable to one country, Morocco. Total steam coal exports to Morocco in 2010 were 1.1 million short tons, an increase of over 60 percent. The average price of steam coal exports to Morocco decreased in 2010 to $73.65 per short ton.

Imports

In 2010, coal imports represented only 1.9 percent of total U.S. coal consumption. Last year, U.S. coal imports decreased by 3.3 million short tons to 19.4 million short tons. Colombia, which has dominated the U.S. coal import market for many years, accounted for over three-fourths of all coal imports. Imports from Colombia, however, decreased by 18 percent to 14.6 million short tons in 2010. Indonesia and Venezuela imports decreased to 1.9 million short tons and 0.6 million short tons, respectively, while imports from Canada increased by a modest 0.5 million short tons. The average price of imported coal increased by 12.3 percent to $71.77 per short ton in 2010.

Coke imports rose by 250.2 percent to 1.2 million short tons in 2010. Average price of coke imports increased to $331.70 per short ton after a fall in 2009 to $268.37 per short ton.