Global Transportation Energy Consumption: Examination of Scenarios to 2040 using ITEDD

Release Date: September 12, 2017

Executive Summary

Energy consumption in the transportation sector is evolving. Over the next 25 years, the U.S. Energy Information Administration’s (EIA) International Energy Outlook (IEO) 2016 Reference case projects that Organization for Economic Cooperation and Development (OECD) countries’ transportation energy consumption will remain relatively flat. In contrast, non-OECD countries will grow to levels higher than in OECD countries by the early 2020s. This rapid non-OECD growth results in continued transportation energy consumption growth through at least 2040.

Some significant uncertainties exist in future transportation energy consumption. This study examines the potential energy impacts associated with some of those uncertainties using EIA’s new international transportation model – the International Transportation Energy Demand Determinants (ITEDD) model. The model outputs presented here are produced in a standalone run, rather than in an overall integrated global dynamic framework, and as such, are intended to be more illustrative than conclusive. However, the fundamental issues, and the use of more detailed modeling for capital stock and transportation demand, both set the stage for fully integrated analysis in future EIA work and provide new insights and reference points for related work.

One area of uncertainty in modeling the transportation sector is consumer preference and rates of vehicle ownership. Will consumers desire more fuel-efficient vehicles and will they prefer public transportation to individual vehicle ownership? Or will the reverse happen where consumers place a high value on vehicle attributes other than fuel economy improvement and desire the personal mobility and flexibility of owning and using a vehicle?

Another area of uncertainty in modeling the transportation sector is government policy. For example, several countries (Canada, China, European Union, Japan, Mexico, and the United States) have enacted light-duty vehicle fuel economy standards. A few countries (Canada, China, Japan, and the United States) also have enacted fuel economy standards for heavy-duty vehicles. Although vehicles are designed for a global market, some uncertainty remains regarding the growth in vehicle demand in non-regulated markets, whether those countries will adopt fuel economy standards, and how efficient vehicles will need to be to meet consumer preference or newly enacted fuel economy standards. Some policies encourage the adoption of alternative-fueled vehicles by consumers or require the production of alternative-fueled vehicles by automobile manufacturers. These policies exist for on-road vehicles but in the future could affect trains and marine vessels. Depending on what fuels are being replaced and what other policies exist or might be put in place, the effect on total transportation energy consumption could range from large to none.

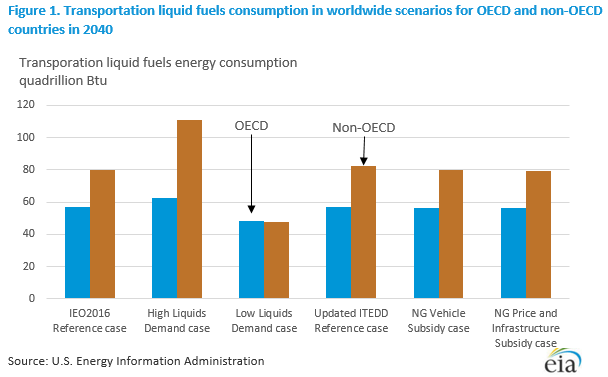

This study considered six worldwide scenarios and two region-specific scenarios to examine future transportation energy consumption. The six global scenarios presented are the following:

- International Energy Outlook (IEO) 2016 Reference case

- High Liquids Demand case

- Low Liquids Demand case

- Updated ITEDD Reference case

- Natural Gas Vehicle Subsidy case

- Natural Gas Price and Infrastructure Subsidy case

The first scenario is the EIA’s International Energy Outlook 2016 (IEO2016) Reference case projections. The second and third scenarios (High and Low Liquids Demand) were developed by adjusting consumer preferences and policies. The third scenario (Updated ITEDD Reference case) reflects the IEO2016 Reference case with ITEDD updates to the on-road module to allow for more refined policy implementation. The last two worldwide scenarios focus on different light- and/or heavy-duty vehicle alternative fuel policies.

Across the worldwide scenarios the projections show that non-OECD countries experience greater differences in transportation liquids consumption than OECD countries (Figure 1). Non-OECD countries experience more growth in their transportation sectors than OECD countries in the reference cases, through 2040. Because many people in non-OECD countries are purchasing vehicles for the first time during the projection period, changes in vehicle fuel economy or fuel choice can have an effect more quickly than in countries with existing large vehicle stocks. Through consumer preference and policy it is easier for developing countries to have more moderate growth in personal vehicle ownership and personal vehicle-miles traveled than in developed countries that already have high vehicle-per capita ratios. However, developing countries could reach OECD-level vehicle per capita ratios more quickly than currently projected.

Two region-specific scenarios were also considered. The first scenario adjusts consumer preference and policies in OECD Europe to reduce light-duty vehicle diesel sales. This scenario made no assumption about which powertrain would take the place of diesel vehicles. Based on make and model availability and price, motor gasoline vehicles sales more than offset the reduction in diesel sales. The second region-specific scenario considered the effects on the transportation sector of slower GDP growth in China than the current forecast. The slowdown in China’s GDP growth results in reduced passenger travel and freight travel.

see full report