Global LNG supplies and natural gas stocks will likely meet demand this winter 2023–24, but risks remain

Release date: November 6, 2023

Relatively full natural gas inventories in the United States and Europe as well as expanded global export and import capacity for liquefied natural gas (LNG) have improved the likelihood that supply will be sufficient to meet demand in global natural gas markets as we enter the upcoming 2023–24 winter season (November–March). However, risks to this balance are associated with possible extreme weather and supply issues.

LNG supplies from new LNG export projects that came online this year or that will start service this winter, in addition to greater output at existing facilities especially in the United States, should help balance global natural gas markets. The addition of new LNG import facilities—both fixed terminal facilities and floating storage regasification units that convert LNG into pipeline-ready gaseous supplies—have increased regional LNG import capacity, especially in Europe. Europe’s natural gas storage inventories are full at the start of the 2023–24 winter season. If normal weather conditions prevail, we expect less natural gas demand for heating in Europe and limited growth in demand from Asia compared with prior years. Under these conditions, the market should remain balanced during the upcoming winter season.

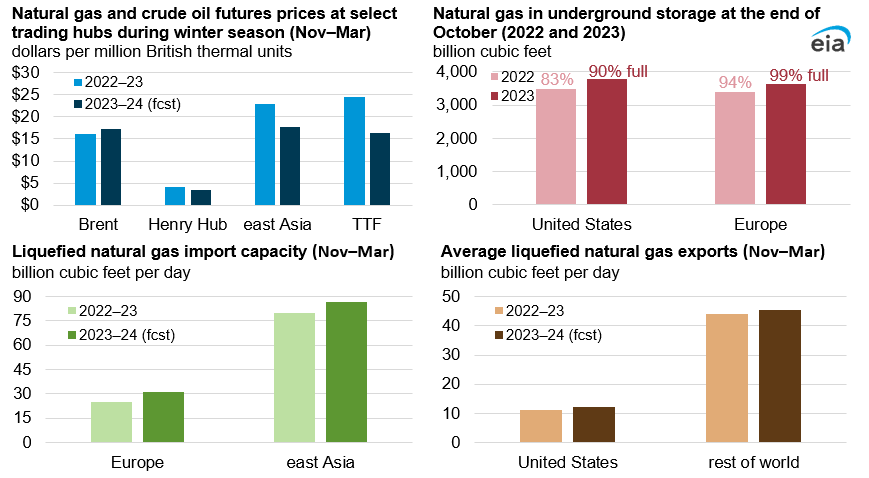

Data source: U.S. Energy Information Administration, U.S. Department of Energy, Bloomberg Finance, L.P., Gas Infrastructure Europe, Aggregated Gas Storage Inventory (AGSI+), International Group of Liquefied Natural Gas Importers (GIIGNL), and CEDIGAZ Note: Fcst = forecast. The 2022–23 historical prices are average daily near-month futures prices. The 2023–24 prices are average monthly futures prices as of October 27, 2023. Brent crude oil price was converted using energy equivalence of 5.691 MMBtu/Bbl. Storage stocks in the United States and Europe (EU-27) are as of October 27, 2022, and October 27, 2023. Europe’s storage stocks include EU-27 countries and do not include storage stocks in the United Kingdom, Serbia, and Ukraine.

Even with increasing LNG supplies and larger natural gas inventories, key market uncertainties remain. Sustained colder-than-normal temperatures in one or more regions in the Northern Hemisphere could increase demand for LNG. Unplanned outages at LNG export facilities or key natural gas supply basins due to freeze-offs could decrease supply and potentially disrupt global natural gas balances by creating supply shortages that lead to price spikes. Some major natural gas utilities, especially in Europe, have limited access to long-term, contract-based LNG supply. The lack of long-term contracts increases supply risk during cold weather and price spikes and may also intensify competition for spot LNG between regions. Lack of underground storage capacity in Asia highlights the region’s dependence on real-time LNG flows. If economic activity in China and other markets improves, that could boost regional natural gas demand. Electricity generation from sources other than natural gas (including nuclear, coal, hydropower, wind, and solar) based on fuel pricing could also affect natural gas balances in regional markets.

Last year, exceptionally mild winter weather in the Northern Hemisphere reduced heating demand in both Europe and Asia. In addition to mild weather, an economic slowdown in China reduced LNG imports. High LNG prices reduced the use of LNG imports in other parts of Asia. Europe implemented coordinated demand-reduction measures to offset decreased natural gas pipeline imports from Russia, decreasing the region’s natural gas consumption by more than 15%. Reduced demand in Asia offset increased LNG demand in Europe, leading to a relatively balanced global natural gas market during the past winter.

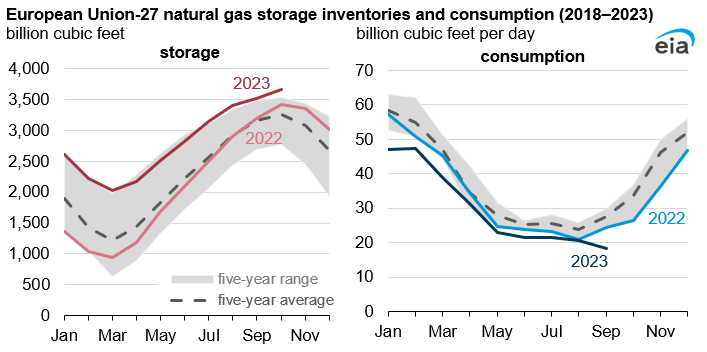

Overall, more natural gas is in storage than last winter. Europe’s natural gas storage inventories are almost full near the start of 2023–24 withdrawal season. Europe has enacted policies requiring storage operators to maximize storage injections during the refill season to ensure availability of natural gas during the winter. Natural gas storage inventories in Europe (EU-27) as of October 31, 2023, were approximately 3,657 billion cubic feet (Bcf). We estimate this storage volume represents 65 days of natural gas consumption at peak five-year (2019–2023) winter rates and 84 days of natural gas consumption at rates like we saw last winter. The on-site storage capacity at regasification facilities in Japan and South Korea has been consistently full this year. In the United States—an important global LNG supplier—storage inventories exceeded last year’s inventories by 8% as of October 27.

This year, LNG front-month futures prices have been consistently lower than last year, mainly in response to more natural gas held in storage inventories in Europe compared with previous years. Global natural gas prices in east Asia and at Title Transfer Facility (TTF) in Europe are down more than 50% compared with this time last year, averaging close to $15.00/million British thermal units (MMBtu), according to data from Bloomberg, L.P. Natural gas prices reached daily record highs of nearly $70.00/MMBtu in east Asia and nearly $100.00/MMBtu at TTF in Europe in the summer 2022. Natural gas prices in both regions averaged over $30.00/MMBtu last winter. Above-average natural gas storage inventories and modest demand in both Europe and Asia have reduced global natural gas prices so far this year. Entering winter, front-month natural gas futures prices remain high enough to encourage robust LNG exports to both Europe and east Asia. Prices could spike in the short term in the event of severely cold regional weather or major supply disruptions.

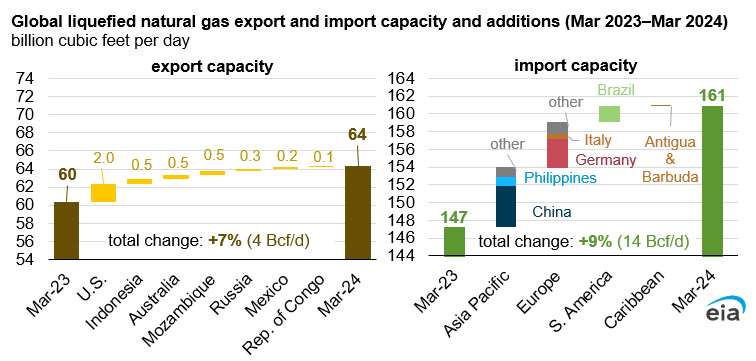

Expanded LNG export and import capacity will make more natural gas available this winter. Similar to last year, global LNG export (liquefaction) capacity continued to expand this year, although more slowly than in recent years. The return to service of Freeport LNG in the United States has boosted global LNG production capacity and LNG exports by 2.0 billion cubic feet per day (Bcf/d) so far this year. We expect approximately 2.0 Bcf/d of additional new and returning-to-service LNG export capacity will be available during winter 2023–24, including projects in Indonesia, Mozambique, Mexico, offshore the Republic of Congo (Brazzaville), Russia, and Australia. We estimate that global LNG import (regasification) capacity has expanded by 13% (18 Bcf/d) so far this year in both Europe and Asia and that more import projects will be entering operation this winter in Germany and China.

Data source: U.S. Energy Information Administration

Exports from the United States will continue to help balance global natural gas markets this winter. The United States, which exported more LNG than any other country in the first half of 2023, will be the key swing supplier of spot LNG this winter. With the return to service of Freeport LNG and the startup of the Calcasieu Pass LNG facility last year, the United States remains an important provider of flexible LNG supplies in global spot markets. In 2022, the United States exported 34% of global spot and short-term volumes, the largest share of any country, followed by Australia at 15%, according to data from the International Group of Liquefied Natural Gas Importers (GIIGNL). This winter, we forecast U.S. LNG exports averaging 12.2 Bcf/d, a 10% increase from last winter. If global LNG demand has a sustained peak, U.S. LNG export facilities, which we estimate have an overall peak capacity of 13.9 Bcf/d, could be utilized at higher rates.

Similar to last winter, countries in Europe will continue implementing natural gas conservation measures and importing flexible LNG supplies to replace natural gas pipeline imports from Russia. In 2022, following a reduction in pipeline imports from Russia, European governments enacted coordinated demand-reduction measures, which reduced natural gas consumption from August 2022 through March 2023 by 18% compared with the previous five-year average during the same months.

In the first six months of this year, Europe and the UK’s LNG imports exceeded natural gas pipeline imports for the first time on record, according to data from Refinitiv Eikon. Europe and the UK’s LNG imports averaged 15.9 Bcf/d, 0.1 Bcf/d more than the region's natural gas pipeline imports from all sources. In comparison, last year, the region imported 14.9 Bcf/d of natural gas as LNG, 28% less than it did through pipelines. LNG exports more than doubled from the United States to Europe in 2022 compared with 2021 and increased by even more in the first half of 2023.

Data source: Aggregated Gas Storage Inventory (AGSI+), Eurostat

LNG consumption in east Asia this winter is a key uncertainty with potentially large implications for global markets. Japan and South Korea have relied in the past on steady LNG imports supplied under long-term contracts, while China has been a major LNG consumer in the global spot market during peak winter months to supplement its contracted LNG supply. Since last year, China increased pipeline imports from Russia and reduced its spot LNG purchases. China is also likely to have access to more stable natural gas pipeline imports from Central Asia (Uzbekistan and Kazakhstan) this winter. Imports from those countries in the past varied based on domestic demand, but Uzbekistan started receiving imports of natural gas from Russia in October 2023 under new supply contracts, making more natural gas available for export to China. However, the pace of China’s natural gas demand recovery and the effects of winter weather on natural gas consumption this winter remain a key uncertainty for the global natural gas market.

Severe cold weather or unplanned supply outages could lead to significant price spikes and affect global natural gas balances. In the event of severe cold weather over several weeks or months in Europe or Asia, global LNG spot prices could increase rapidly. Buyers in Europe and Asia would have to compete for spot LNG cargoes, which in turn would raise prices at both European and Asian price hubs, especially if they can’t switch to alternative fuels. Production freeze-offs in the United States, Norway, or other major natural gas suppliers could also greatly affect global balances, creating supply shortages and price spikes. Other supply disruptions could occur, such as a further reduction in pipeline exports from Russia transiting Ukraine, worker strikes at Australian LNG facilities, spread of the military conflict in the Middle East, or other potential unplanned outages affecting global supplies.