Issues in Focus: Drivers for Standalone Battery Storage Deployment in AEO2022

The Drivers for Standalone Battery Storage Deployment is based on the Annual Energy Outlook 2022 which reflects current laws and regulations as of November 2021. As such, it does not incorporate the recently enacted Inflation Reduction Act, which will be reflected in future editions of the AEO.

Executive Summary

Large-scale battery storage capacity on the U.S. electricity grid has steadily increased in recent years, and we expect the trend to continue.1,2 Battery systems have the technical flexibility to perform various applications for the electricity grid. They have fast response times in response to changing power grid conditions and can also store excess generation from the grid, allowing energy from solar or wind resources to be used during the time of highest value, not just when produced. However, the degree to which different applications will drive future battery storage deployment is uncertain.

This study evaluates the economics and future deployments of standalone battery storage across the United States, with a focus on the relative importance of storage providing energy arbitrage and capacity reserve services under three different scenarios drawn from the Annual Energy Outlook 2022 (AEO2022). The analysis focuses on the AEO2022 Reference case and side cases with relatively high deployment of battery storage through 2050. We assume that a battery storage facility can receive two sources of revenue payment: an energy payment (from selling electricity generation to the grid) and a capacity payment (from its contribution to grid reliability through capacity reserves). The availability and design of these capacity and energy markets currently vary across the United States, with some utilities relying on power exchanges, some on market mechanisms, and other utilities providing such services under regulatory constructs. Assessing the economic drivers of standalone battery storage deployment can allow regulators, policymakers, and market operators to evaluate the various roles of battery storage, particularly as more intermittent renewable generators are added to the power grid and competing storage technologies come into play. The fundamental drivers of energy storage value as evaluated in our analysis will be similar, regardless of whether the utility participates in a regional electricity market or is operating as a vertically integrated generator and distributor of electricity within a regulated service territory.

Our analysis of the economics of future standalone battery storage deployments suggests that combining revenue streams from different applications is important when evaluating future investment decisions. In addition, in some scenarios one application may be a larger economic driver than the other:

- In the AEO2022 Reference case, battery storage is primarily deployed when receiving both energy and capacity payments.

- In the Low Renewables Cost case, we assume lower capital costs for battery storage and renewable power plants compared to the Reference case. The lower capital costs result in battery storage being more competitive with natural gas units in the capacity market, even when receiving lower capacity credits. Greater penetration from intermittent resources also reduces marginal electricity prices, indicating that energy markets may be less important.

- When electricity prices are higher, as in the Low Oil and Gas Supply case, the energy payment for battery storage applications can be a stronger driver for future battery storage deployment than the capacity payment.

Background

Battery storage can provide flexible capacity and energy to the power grid, and can be used in a wide range of applications3 that we categorized into three primary types:

- Energy arbitrage: Batteries purchase the electricity needed for charging when electricity prices are low, and sell electricity through discharging when electricity prices are high.

- Capacity reserve:4 Batteries contribute to the capacity reserve margin the power grid requires to ensure reliability.

- Ancillary services: Batteries help maintain grid stability through frequency response (maintaining grid frequency of 60 hertz) and spinning reserves (quick responding reserves for sudden system disruptions).

In AEO2022, we model battery storage used in two applications, energy arbitrage and capacity reserve, which represent the primary long term economic opportunities for large-scale deployment of batteries under the conditions generally represented in the AEO Reference case and its side cases. We do not model ancillary services for battery storage, which represent high-value but low-volume markets that are not likely to significantly affect the gross characteristics of the generation and capacity mix for electricity markets as represented in EIA's AEO projections.

In all cases, we assume all batteries have a maximum discharge duration of four hours, for a total system rating of 4 megawatthours (MWh) of stored energy for every megawatt (MW) of rated battery capacity. Multiple batteries can be operated simultaneously to increase instantaneous output for the 4 hour discharge period, can be operated serially to extend the total discharge period, or in some combination to optimize power and energy capacity utilization. Although we model battery storage as either a standalone system charged directly from the grid or as a solar-plus-battery hybrid system charged directly from the onsite (co-located) solar photovoltaic (PV) generator, this study only evaluates economic drivers for standalone battery storage systems because each component (storage and solar generation) can be independently evaluated.5 When operated as a hybrid unit, where the battery is constrained to be charged from its associated solar panels, it becomes difficult to evaluate these characteristics separately.

The potential economics of battery storage as modeled for this study include revenue received from energy arbitrage and capacity reserve applications. It is important to note that we expect the U.S. electric power system in 2050 to be very different than today, as represented in the AEO Reference and side cases. System conditions become more favorable for storage over time, particularly with respect to the high incidence of solar generation and how solar interacts with demand.

Energy arbitrage

We assume battery storage participates in the energy market and receives energy payments for generating at the marginal cost of electricity when the facility is dispatched. In our model, the marginal cost of electricity, or marginal generation price, is the cost of meeting demand in a specified period and is typically determined by the variable cost (fuel cost plus variable operation and maintenance, or O&M, cost) of the most expensive generating unit dispatched to satisfy demand.

Standalone energy storage facilities in our model must also purchase electricity from the grid, ideally during low-demand hours, to recharge. In some cases, grid operators may pay the battery project operator for storage to off-load excess generation from the grid (reflected as negative prices). Net revenue for the energy arbitrage application then becomes the difference between the price paid to recharge (positive, free, or negative) and the price received to discharge.

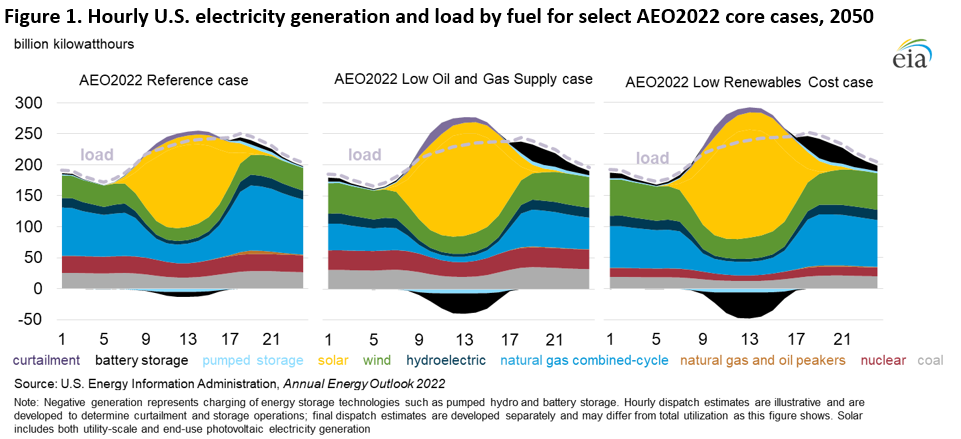

High grid penetration of solar generation can result in zero or negative prices during hours when generation from zero-marginal-cost and inflexible generators exceeds demand and solar generation would otherwise be curtailed. Battery storage uses these hours of excess solar generation and lower electricity prices for charging, generally between the hours of 9:00 a.m. and 5:00 p.m. (Figure 1). As demand increases in the evening and overnight hours, battery storage discharges to capture the benefit of higher electricity prices, usually between 5:00 p.m. and midnight, and in some cases, between midnight and 8:00 a.m.7

Capacity reserve

When a battery storage unit contributes to the required reserve margin through a capacity market, it receives revenue for its available capacity, which is calculated as a capacity price times a capacity credit.

We model the capacity price as the marginal cost of retaining or installing enough capacity to meet a reserve margin. The capacity credit represents the ability of an electricity generator to provide system reliability reserves during times of peak load. For dispatchable units, such as natural gas-fired combustion turbines or nuclear power plants, we assume that the capacity credit is 1, or 100%, indicating that the entire rated capacity is available to participate in the reliability capacity market. For intermittent renewables and batteries, the capacity credit is, or can be, less than 100% because the entire rated capacity of the unit may not be available during peak load hours. This limitation is due to a lack of resources (such as little sunlight during an evening peak) or insufficient stored energy (such as when a battery is partially discharged entering the peak load hours). When deciding between options to meet reserve requirements and receive future capacity payments, the ability to maximize the reserve margin contribution from each MW installed during peak hours, represented by the capacity credit, is weighed against the capital cost of installing each option.

We model capacity credits for battery storage to be dependent on the amount of energy stored in batteries during net peak load8 hours. Because battery storage optimizes buying electricity for charging during the hours with lower electricity prices and selling electricity during the hours with higher electricity prices, it essentially shifts a portion of electricity demand from peak load hours to non-peak hours, flattening the spikes in electricity demand that typically occur during peak hours. The new flattened peak load is lower in magnitude but longer in duration as more battery capacity is added to the grid, all else equal. Because we assume that batteries have a limited duration of four hours in our model, the ability of battery storage to meet the entire duration of the peak decreases as more battery capacity is deployed. The capacity credit for battery storage decreases and either a single unit (assumed as 50 MW by 4 hours of storage) can operate at a lower output (less than 50 MW) to meet the increased width of the peak, or additional units can be added to provide the full output (50 MW) for a longer duration.

Capacity credits for storage are also affected by other characteristics of the grid, including changes to electricity demand patterns and increasing generation from solar or other resources with a strong diurnal or seasonal output pattern. In addition, using battery storage to provide both energy arbitrage and capacity reserve requires operators to develop operational strategies that consider both services. Grid operators across the country are in different stages of addressing how to value the ability of storage to provide firm capacity, with different approaches in different regions. EIA necessarily takes a simplified approach to this valuation, as described in Appendix A of this report.

Methodology

This study uses the AEO2022 Reference case, Low Oil and Gas Supply case, and Low Renewables Cost case to explore the addition of battery capacity.

- The Reference case assumes implementation of current laws and policies, as well as baseline assumption for technology progress. The future costs of utility-scale battery, PV, wind, and other technologies are not pre-determined, but allowed to decline with increased market penetration (learning by doing) and other factors.

- The Low Renewables Cost case assumes higher learning rates for renewable technologies (including battery storage), resulting in a cost reduction of about 40% from the Reference case by 2050. The cost reduction in the Low Renewables Cost case are fixed in advance, based on the cost trajectory resulting from the Reference case.

- The Low Oil and Gas Supply case reflects higher costs and lower resource availability for oil and natural gas in the United States. As with the Reference case, utility-sector costs are subject to learning-by-doing and other cost dynamics.

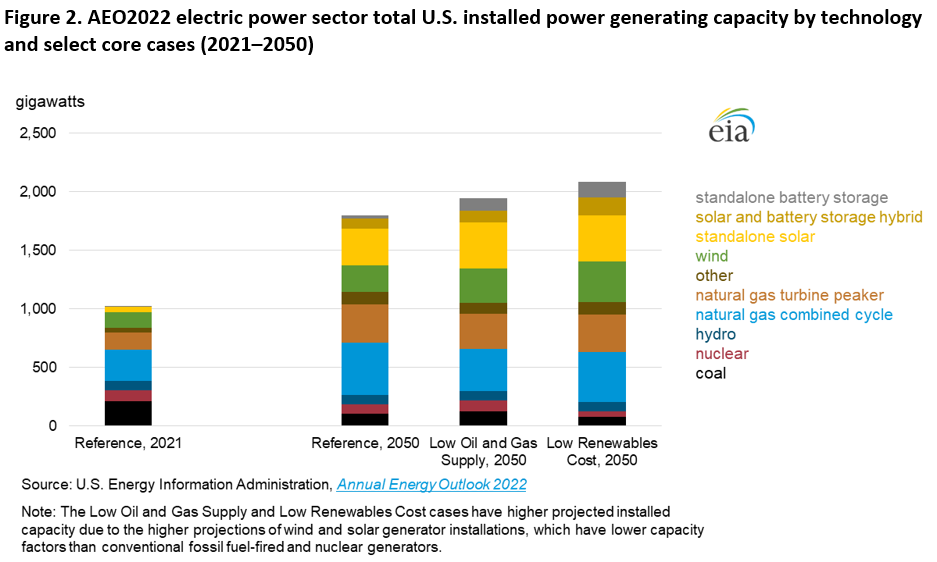

We expect greater penetration of intermittent generation and battery storage deployment in both the Low Oil and Gas Supply case and the Low Renewables Cost case compared with the Reference case or other AEO2022 side cases (Figure 2). However, the economics that drive intermittent generating capacity and battery storage are different between these two cases, making them useful comparisons for evaluating economic drivers for battery storage deployment.

Our study assumes that standalone battery storage provides energy arbitrage or capacity reserve, receiving energy payments for energy arbitrage use and capacity payments for capacity reserve use. Limiting battery storage’s ability to participate in only one of the two markets (energy or capacity) allows us to see how much battery storage is deployed for each application compared with the original AEO2022 core cases, which allow battery storage to participate in both markets. For this analysis, capacity and energy payments are represented as average annual values over the assumed cost-recovery period of 30 years for new battery storage in a particular online year, and are expressed as real 2021 dollars per kilowatt ($/kW).

For each of the three AEO2022 core cases evaluated here (Reference case, Low Oil and Gas Supply case, Low Renewables Cost case), two alternative cases were run. In the three AEO2022 core cases, we assume standalone battery storage systems participate in and receive revenue for both energy arbitrage and capacity reserve. In each of the two alternative cases, we limit the standalone battery storage system to participate and receive revenue for one use only, as described in the following sections. Thus we examine a total of 9 cases in this analysis.

Although the projections include solar-plus-battery hybrid systems charged directly from the onsite (co-located) solar photovoltaic (PV) generator, this study only evaluates and discusses economic drivers for standalone battery storage systems.9

Capacity Only cases

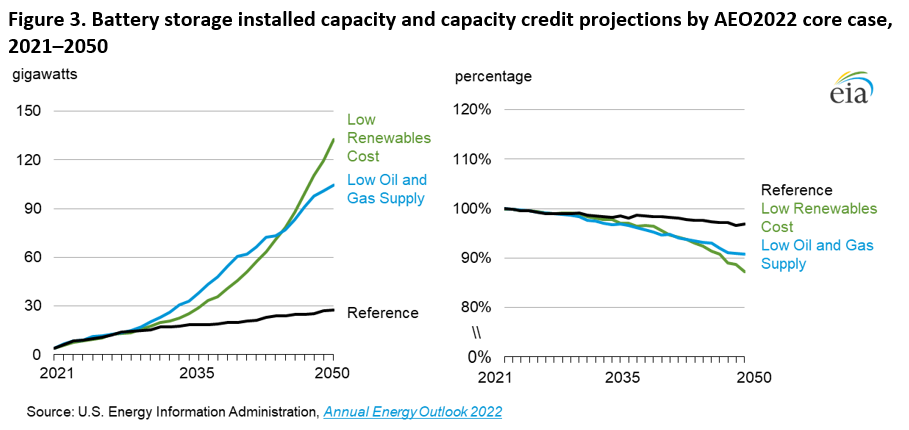

In these cases, we assume battery storage receives revenue only from its contribution to the capacity reserve margin and not from energy arbitrage when making capacity planning decisions for future years. When compared to the Reference case, the model has deployed enough battery storage in both the Low Oil and Gas Supply case, Low Renewables Cost cases to flatten the net load curve and reduce the capacity credit for storage below Reference case levels (Figure 3).

Energy Only cases

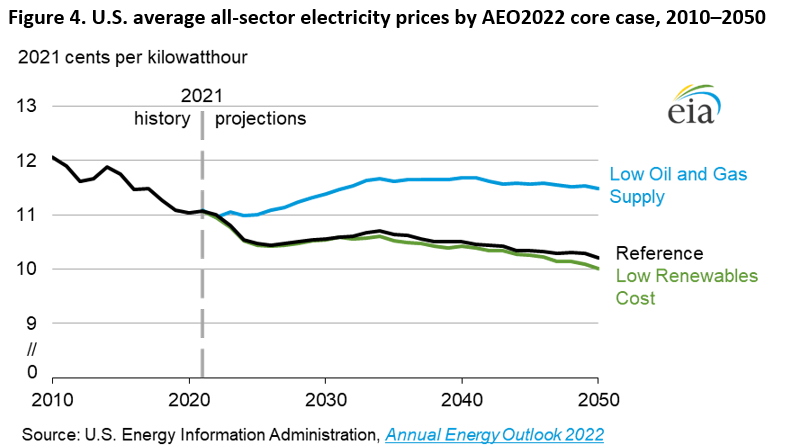

In these cases, we assume standalone battery storage receives revenue only from energy arbitrage and is not used for capacity reserve purposes. Electricity prices are a component in determining the energy payment, and in our analysis they are generally determined by the cost to dispatch the marginal generating unit that must operate to meet demand during a specific period. In the AEO2022 Low Oil and Gas Supply core case, the higher projected price of natural gas leads to higher operating costs for the natural-gas generating units that operate on the margin and are used to meet incremental electricity demand. In that same case, electricity prices are 9% higher, on average, than those in the Reference core case between 2021 and 2050 (Figure 4). In contrast, more generation from low- or zero-cost renewables in the AEO2022 Low Renewables Cost core case leads to 1% lower electricity prices averaged over the projection period when compared with the AEO2022 Reference core case.

Results

The ability for battery storage to participate in both energy and the capacity markets is important in supporting future battery storage growth in all cases (Table 1).

Table 1. Summary of results by case, 2050

| Case | Total battery storage power capacity (gigawatts) 10 |

Capacity market payment (2021 dollars per kilowatt) |

Energy market payment (2021 dollars per kilowatt) |

|---|---|---|---|

| Reference—Core | 28 | 54.37 | 11.55 |

| Reference—Capacity Only | 14 | 58.81 | 0 |

| Reference—Energy Only | 13 | 0 | 12.64 |

| Low Renewables Cost—Core | 133 | 41.42 | 12.11 |

| Low Renewables Cost—Capacity Only | 59 | 52.97 | 0 |

| Low Renewables Cost—Energy Only | 13 | 0 | 22.14 |

| Low Oil and Gas Supply—Core | 104 | 48.51 | 28.41 |

| Low Oil and Gas Supply—Capacity Only | 14 | 59.77 | 0 |

| Low Oil and Gas Supply—Energy Only | 20 | 0 | 37.55 |

More battery capacity is installed by 2050 in the Low Renewables Cost—Capacity Only case than in the corresponding Low Renewables Cost—Energy Only case, indicating more value for batteries meeting capacity reserve requirements under conditions with greater solar or wind generation.

In the Low Oil and Gas Supply—Energy Only case, the energy payment for battery storage causes more battery storage growth than the capacity payment in the Low Oil and Gas Supply—Capacity Only case because the operators receive more revenue when electricity prices are higher.

Removing battery storage’s participation in either the energy or capacity market, compared with the AEO2022 core cases (with participation in both markets) decreases the total revenue available to the battery storage facilities compared to when it is able to receive revenue from both markets.

Reference case, alternative cases

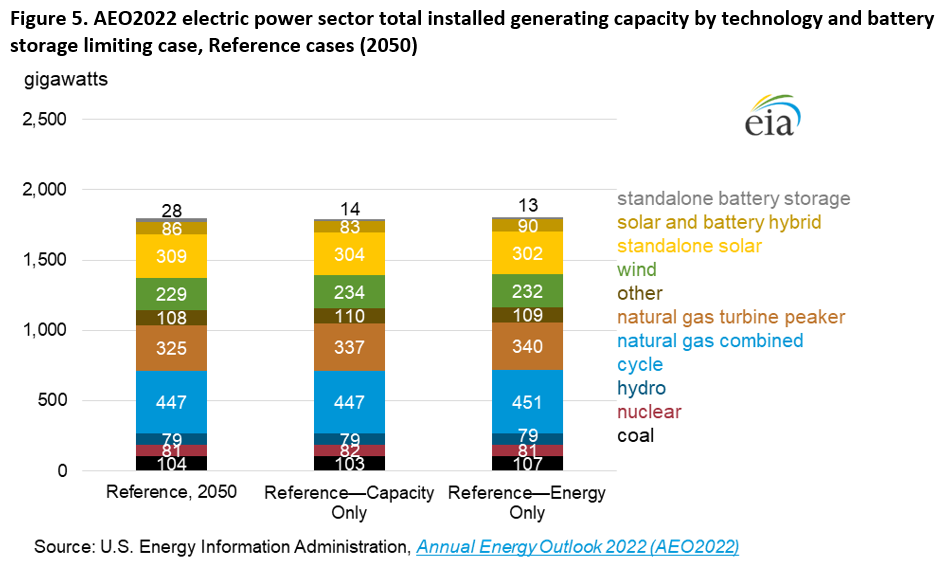

We altered Reference case assumptions, limiting standalone battery storage’s ability to participate to only the energy or the capacity market, not both. Exploration of these alternatives suggest that battery storage becomes less cost competitive than natural gas-fired combustion turbine peaking units (CT) and natural gas-fired combined-cycle plants when storage cannot participate in both markets at the same time. This limitation results in nearly all 15 GW of unplanned battery storage capacity additions becoming uneconomical to build by 2050 (Figure 5); remaining capacity primarily represents projects that are either already on the grid or already in advanced planning/construction phases. In both alternative cases, CT plants primarily replace the battery storage capacity, also reducing investment in total solar capacity.

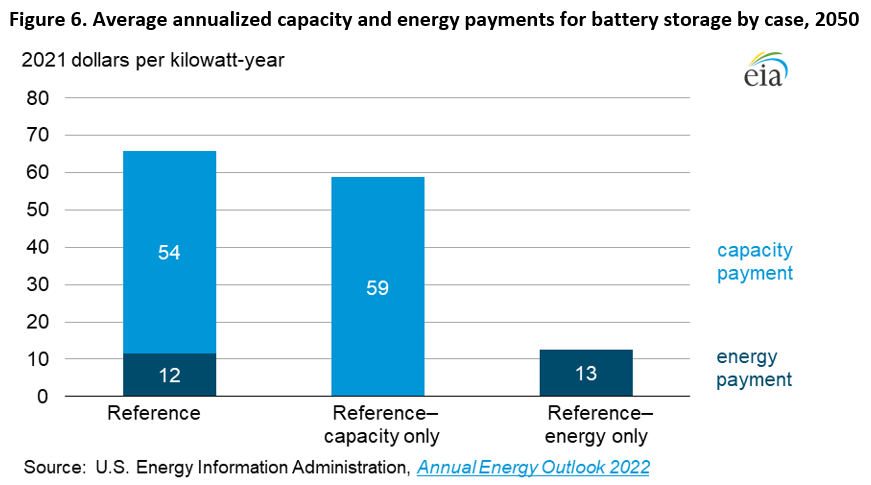

When battery storage facilities cannot participate in the capacity market (Reference—Energy Only case), the revenue from the energy payment alone cannot cover the investment cost of building new battery storage facilities. In the Reference—Capacity Only case, the revenue available to standalone storage facilities comes only from their participation in the capacity market. The resulting modeled capacity payment of $59/kW for the year 2050 in the Reference—Capacity Only case is slightly higher than the $54/kW modeled in the AEO2022 Reference core case (Figure 6). The modeled capacity payment is higher partly due to the availability of a larger capacity credit for battery storage because of fewer expected battery storage capacity additions. The capacity payment alone is still sufficient to make a small amount of battery storage capacity economically competitive in some regions. Operators cannot cover investment costs in this case through energy only payments, despite the slightly higher marginal cost of electricity in the Reference case alternatives compared to the core Reference case, resulting from less total solar PV generated power and more generation from natural gas-fired units.

Low Renewables Cost case, alternative cases

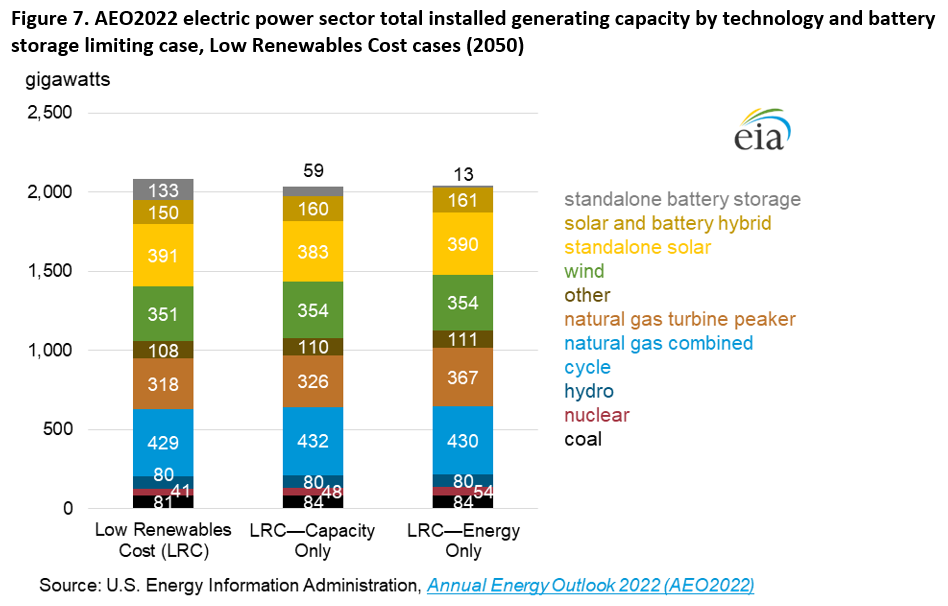

In the Low Renewables Cost—Energy Only case, our model indicates that it is uneconomical to build any new battery storage throughout the projection period, with only 13 GW of historical or previously planned capacity installed compared with 133 GW installed in the AEO2022 Low Renewables Cost core case (Figure 7). However, in the Low Renewables Cost—Capacity Only case, 59 GW of battery storage capacity is operating in 2050. This result suggests that battery storage remains economically competitive with the capacity payment alone, particularly with higher intermittent generation. Similar to the Reference case alternative cases, when limiting the application for standalone battery storage participation to only one application, much less battery storage capacity is built in the Low Renewables Cost case alternative cases compared to the core case, and more natural gas-fired CT capacity is built to replace it.

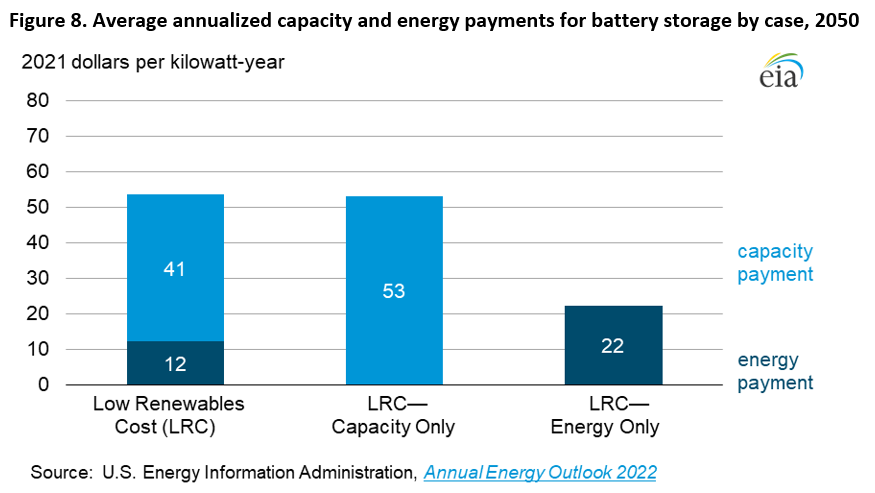

The capacity payment is projected to be higher in the Low Renewables Cost—Capacity Only case in 2050: $53/kW compared with $41/kW in the AEO2022 Low Renewables Cost core case because of the higher capacity credit available due to fewer battery storage additions (Figure 8). Additionally, because we assume a lower installed battery cost in the Low Renewables Cost cases relative to the Reference cases, the capacity payment in the Low Renewables Cost—Capacity Only case is still sufficient to support 47 GW of additional storage capacity over the projection period, even without an energy payment. Although the projected revenue from energy arbitrage available to energy storage in 2050 is higher in the Low Renewables Cost—Energy Only case compared to the AEO2022 Low Renewables Cost case, it is still insufficient to support capacity additions even under the low capital cost assumption, without the addition of a capacity payment.

Low Oil and Gas Supply case, alternative cases

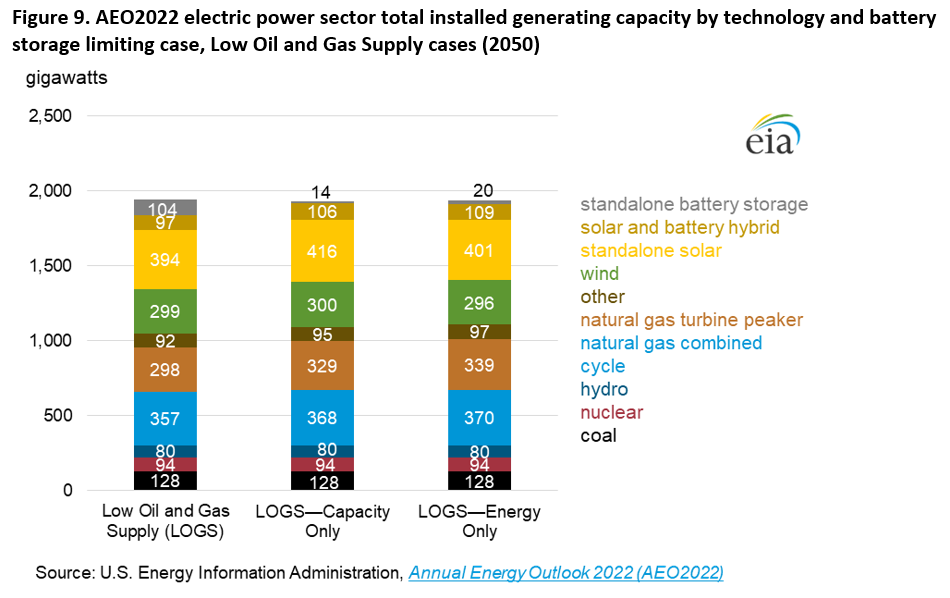

The Low Oil and Gas Supply—Energy Only case is the only case in which we project battery storage to be economically competitive with revenue coming solely from energy payments. Under the case assumptions, the model projects 20 GW of storage capacity installed by 2050 to solely provide energy arbitrage, compared with 104 GW in the Low Oil and Gas Supply core case (Figure 9). Only 14 GW of battery storage is built in the Low Oil and Gas Supply—Capacity Only case, of which only 1 GW is not historical or previously planned capacity. This result suggests that under the conditions explored in the Low Oil and Gas Supply cases, battery storage revenue from energy markets is a bigger economic driver than revenue from capacity markets. However, isolating participation to either market (the Energy Only and Capacity Only alternative cases) reduces projected future deployment of standalone battery storage by over 90% compared with the AEO2022 Low Oil and Gas Supply core case, which allows for battery storage participation in both markets.

Similar to the previous Energy Only and Capacity Only alternative cases, when we limited the market participation for standalone battery storage to energy markets, we project that natural gas-fired CT capacity replaces most of the battery storage. However, in this case, solar PV capacity (both standalone solar and hybrid solar co-located with battery storage) would increase as well. PV capacity would increase due to the higher prices of natural gas in these Low Oil and Gas Supply case alternatives, which allow solar PV to still be a competitive option to serve peak load hours, even when the solar resource is curtailed and not fully utilized in other hours. The higher natural gas prices also lead to higher marginal prices for electricity in peak load hours, resulting in a higher energy payment for battery storage than in the other Energy Only and Capacity Only cases.

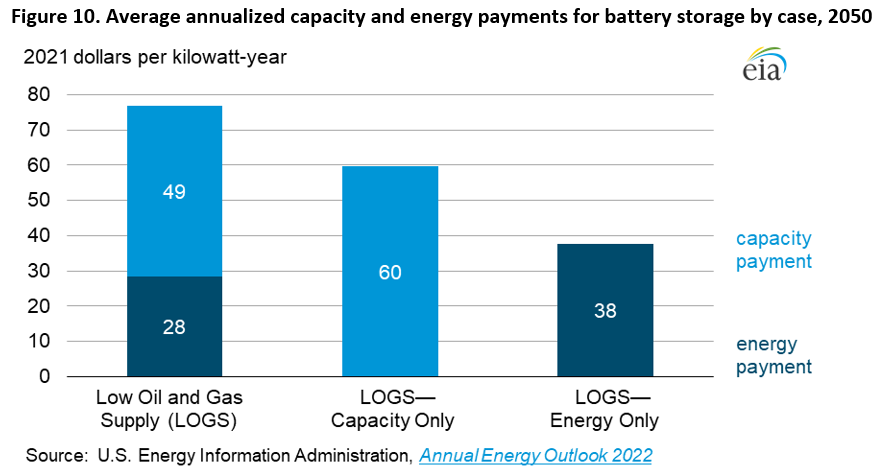

We estimate the average capacity payment in 2050 in the Low Oil and Gas Supply—Capacity Only case to be $60/kW for battery storage (Figure 10). However, even with the highest capacity payment of all the Capacity Only cases, without the energy payment from energy market participation, battery storage additions are limited to 1 GW in this case. Fewer retirements of coal-fired and nuclear generators in the Capacity Only cases also reduce the need for extra capacity to meet the reserve margin in the Low Oil and Gas Supply—Energy Only and Capacity Only cases.

In the Low Oil and Gas Supply—Energy Only case, we estimate the energy payment to be more than the Low Oil and Gas Supply core case. The marginal cost of electricity increases due to the natural gas units replacing the battery storage plants that would have otherwise been built. In addition, even with lower revenue from energy-only payments than the AEO2022 Low Oil and Gas Supply core case, battery storage would be economical to support capacity additions without capacity payments in some regions by 2050.

Electricity Prices

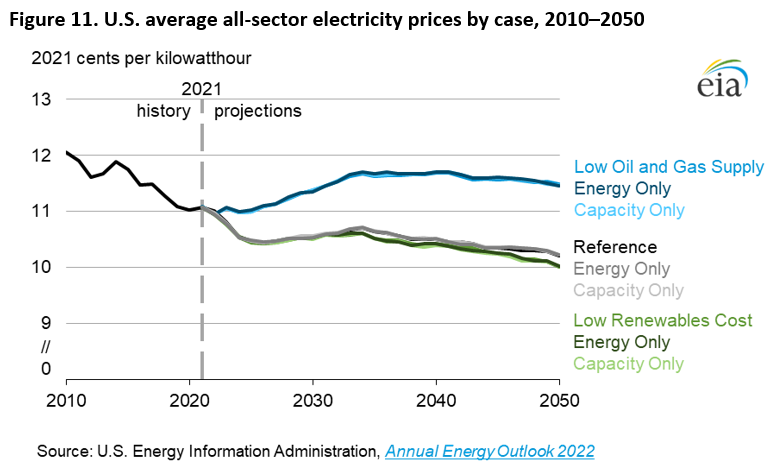

Limiting battery storage applications in the Low Renewables Cost—Energy Only and Capacity Only cases and in the Low Oil and Gas Supply—Energy Only and Capacity Only cases changes our estimates of average electricity prices minimally from their respective core cases (Figure 11). The average power prices in the Low Oil and Gas Supply—Capacity Only case and Low Oil and Gas Supply—Energy Only case are in a tight range with the Low Oil and Gas Supply case but remain much higher on average when compared with the other Energy Only and Capacity Only cases. We observed similar results for the Reference case and Low Renewables Cost cases, where we estimate that prices would change minimally among the energy and capacity-only cases, but all three Low Renewables Cost cases remain about 1% below the average Reference case prices.

Conclusions

Battery storage can be used for a number of applications when serving the power grid. Depending on factors such as diurnal variation in hourly electricity prices, competition from natural gas-fired generators, and increased deployment of intermittent renewable power generators on the grid, different market participation options for battery storage may drive future investments in the technology.

We found that in all AEO2022 scenarios, allowing battery storage to participate in both energy and capacity markets, rather than exclusively in one market or the other, resulted in significantly more deployment of battery storage systems through the year 2050. This result suggests that combining multiple revenue streams could be important when evaluating future investments in battery storage. In cases with a high penetration of renewables—particularly solar—standalone battery storage can remain economically competitive when allowing only energy or only capacity payments, although to a much lesser degree than when allowing both. However, the cost competitiveness of each battery storage application differs by case.

- In the Low Renewables Cost cases, the lower capital cost assumption makes battery storage economically competitive with conventional technology such as combustion turbines—even when participating only in the capacity market—even though the contribution to reliability from these resources decreases with increased grid penetration. However, higher wind and solar penetrations also reduce marginal electricity prices, indicating that energy markets may be less important as an economic driver for battery storage capacity additions under the conditions of this case.

- In the Low Oil and Gas Supply cases, participation in energy markets provides a slightly higher overall revenue than participation in capacity markets alone because of the higher marginal cost of electricity under the assumption of higher natural gas prices, making the energy market participation a stronger economic driver for battery storage capacity additions.

- Model results can be sensitive to assumed learning rates, particularly for technologies like batteries that have experienced rapid declining costs. In the Reference and Low Oil and Gas Supply cases, the selection of particular learning rates may affect the economics of participation in energy or capacity markets. The Low Renewables Cost case assumes a fixed cost decline, although these are based on Reference case results (that is, 40% below Reference case levels by 2050).

The cases examined in this report show the relative importance of energy and capacity markets to battery storage under several different scenarios. In particular, we examined the sensitivity to electricity prices from both reduced renewables and battery storage costs as well as increased natural gas prices. Examination of a wider range of cases from the AEO2022 supports the notion that battery storage growth strongly correlates with renewables growth, especially solar generation. As shown in this report, the relative importance of energy or capacity markets to storage is sensitive to the cost factors driving the increased solar generation, and it is reasonable to conclude that other drivers such as carbon emissions policies, macro-economic conditions, or other policy- or market-related factors could lead to different results.

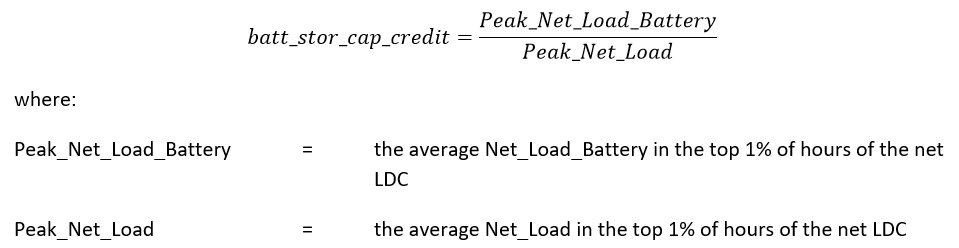

Appendix A: Methodology for calculating capacity credit

EIA calculates capacity credit for battery storage based on the load duration curve (LDC) method, as implemented by Lawrence Berkeley National Laboratory . The LDC is an hourly load curve sorted from highest load to lowest hourly load values. A “Net LDC”, Net_Loadh, can be created by first reducing the hourly load curve by the generation from non-dispatchable technologies such as solar or wind, and then sorting the hours by this “net load”. A “Storage Net LDC”, Net_Load_Batteryh, can be produced by further reducing the hourly load curve by the potential generation from battery storage units, represented by the amount of energy stored in the batteries in any given hour, and then sorting the hours by load. Battery state-of-charge for each representative hour is determined by the optimal system dispatch across the day, which will tend to charge batteries during periods of low energy cost and discharge during periods of highest value, accounting for energy remaining from the previous day and needed for the following day.

The model is unable to represent all 8760 hours in a year, and thus load duration curves for both peak net load and peak net load with the battery are determined based on a representative year using a 12 month by 24 hour by 2 day type time resolution (576 hours). Thus, for each month of the year, the model captures each hour of a typical weekday (typically higher loads) and a typical weekend (lower loads).

The complete methodology for the energy storage capacity credit calculation will be described in the AEO2022 documentation, when available.

Footnotes

- U.S. Energy Information Administration, “U.S. large-scale battery storage capacity up 35% in 2020, rapid growth set to continue”

- U.S. Energy Information Administration, Battery Storage in the United States: An Update on Market Trends, August 16, 2021.

- U.S. Energy Information Administration, “Battery storage applications have shifted as more batteries are added to the U.S. grid”

- U.S. Energy Information Administration, “Reserve electric generating capacity helps keep the lights on”

- U.S. Energy Information Administration, Renewable Fuels Module Assumptions to AEO2022

- Zero-marginal-cost generators include renewables such as wind, solar, and hydro that lack significant fuel or other variable operating costs. Inflexible generators are generators that are dispatched at minimum operating thresholds and face significant shutdown or restart costs if forced to go offline. Such generators, which can include plants with steam boilers or plants with technical or regulatory restrictions on their operation, may find it more economical to pay other generators to curtail operations rather than shut down. This situation can result in negative prices in wholesale electricity markets.

- The hourly generation profile shown in Figure 1 is an aggregation of hourly generation projections for all regions covering the entire continental United States in 2050. Hourly dispatch varies considerably across the country, and that variability influences the extent of the contribution from solar when joined by standalone battery storage.

- Net load is the total electricity load minus intermittent generation, such as wind and solar. It represents the hourly load that must be supplied by dispatchable generators on the grid, which must increase their power generation during times when solar and wind are not available.

- Solar PV-battery storage hybrid technology is not the focus of this analysis. Battery storage is modeled as an indistinguishable component of the hybrid system, and the revenue realized from this technology cannot be easily calculated separately from the PV component. So, we evaluated only the revenue of standalone battery storage applications.

- All cases have a minimum 13 GW of battery storage, which comes from historical or previously-planned generator additions.

- Lawrence Berkeley National Laboratory, “Simple and Fast Algorithm for Estimating the Capacity Credit of Solar and Storage”, 2020