Release Date: November 7, 2023

STEO Between the Lines: What effect have sanctions had on Russia’s production of petroleum and other liquids?

Data values: Non-OPEC Petroleum and Other Liquids Production

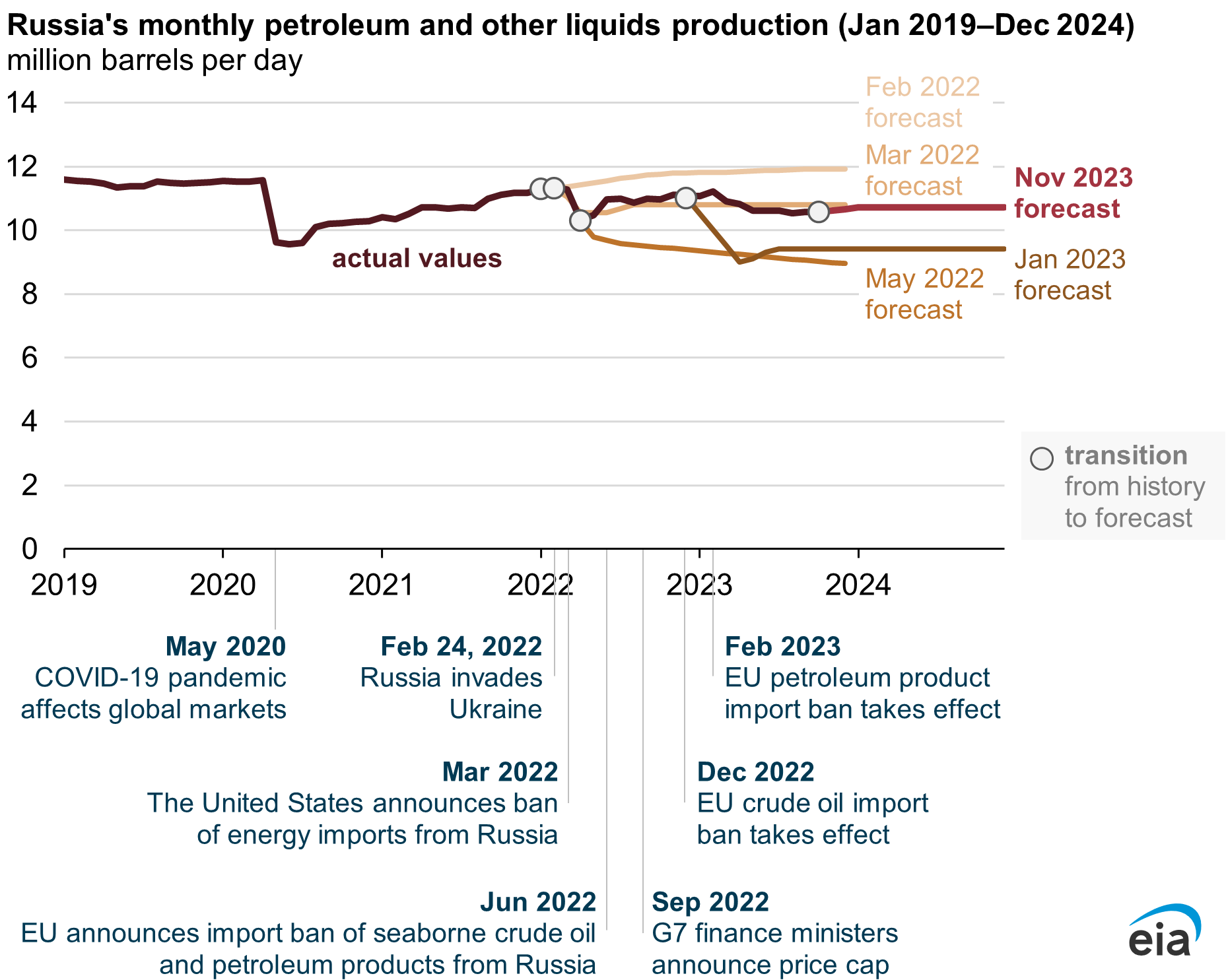

The prospects for trade in global fuels we forecast in our Short-Term Energy Outlook (STEO) has evolved in the months since Russia’s full-scale invasion of Ukraine in February 2022. The international response of voluntary corporate actions and sanctions following the invasion affected Russia’s liquid fuels production and in turn required adjustments in global oil trade flows. Although our forecasts of Russia’s production and trade flows have been relatively stable in recent months averaging about 10.6 million barrels per day (b/d) in the second half of 2023, many factors affecting our forecasts remain uncertain.

Sanctions and other actions have reduced Russia’s production

In the February 2022 STEO, we expected Russia’s production of petroleum and other liquids to continue to recover from its pandemic-related decline in early 2020. The next month, in our first forecast following the invasion, we expected a muted effect on Russia’s production because official sanctions were relatively limited. Shortly after we finalized the March STEO, the United States announced an import ban and many western energy companies announced that they were voluntarily stopping operations in Russia and stopping purchases or shipments of oil from Russia.

By May 2022, Russia’s production had declined considerably—down 9% in April alone—and we expected this decline to continue. Heightened uncertainty unfolded around the possibility of sanctions by the European Union (EU), which would ban imports of oil from Russia and include potentially wide-ranging provisions on shipping, tanker insurance, and other services to exporters of Russia’s oil.

Since May 2022, additional sanctions were announced and implemented, including EU sanctions and the Group of Seven countries (G7) price cap. We had time to observe actual market reactions to the implementation of these restrictions, and we included these observations in our forecast. By the January 2023 STEO—the first to include forecasts for 2024—we expected Russia’s production to decline based on several uncertain factors outlined in a previous Between the Lines article.

We assumed the limited number of oil tankers that weren’t subject to G7 led sanctions would limit Russia’s ability to export refined products. Without export markets or significant excess storage capacity, Russia would have to reduce refinery runs and crude oil production. However, the number of tankers available and the willingness to transport Russian oil has exceeded our initial expectations.

Russia, along with other countries not participating in sanctions, have established shipping services designed to avoid G7 sanctions and price caps, leading to more export outlets being available to Russia than we assumed. In the latest STEO forecast, we expect Russia’s production to average 10.7 million b/d in 2023 and remain mostly unchanged in 2024.

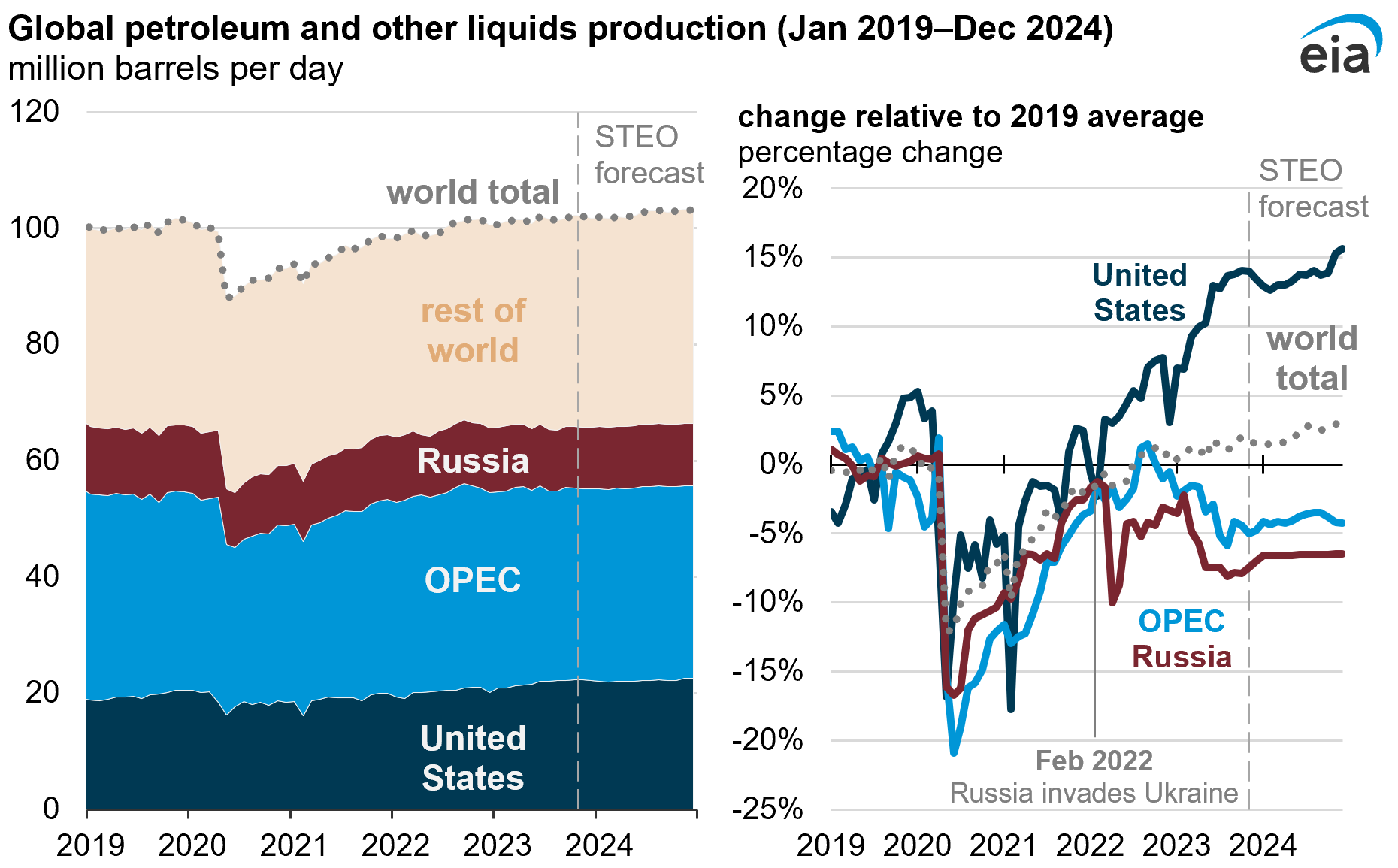

Russia's post-pandemic increases have lagged OPEC and the United States

Prior to the invasion, growth in Russia’s oil production following the pandemic was similar to the United States and OPEC in 2020 and 2021. However, since 2022, growth in Russia’s petroleum liquids production has lagged that of the United States and OPEC. Russia was among the OPEC+ countries that announced production cuts in November 2022, and Russia separately announced additional voluntary cuts of 500,000 b/d in February 2023. Although several factors affect their production, we believe sanctions and voluntary actions by companies in response to the invasion have been the primary cause of cuts in Russia’s production.

Data values: Non-OPEC Petroleum and Other Liquids Production and OPEC Crude Oil (excluding condensates) Production

Global petroleum trade flows have shifted in response

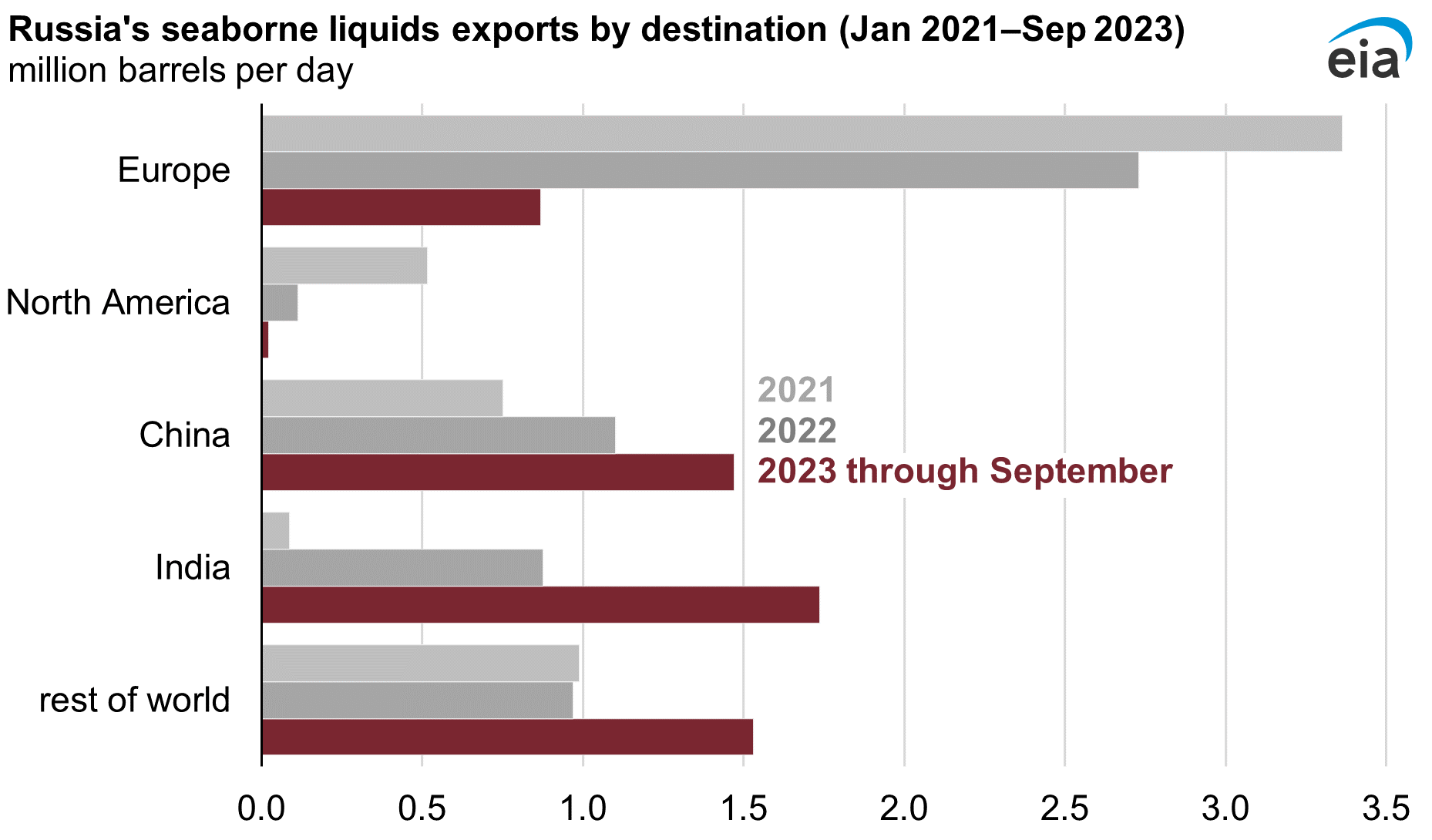

Russia’s liquid fuels production has been more robust than we expected soon after the invasion, averaging 10.8 million b/d since March 2022. One of the primary reasons is that the global oil market has adapted and shifted trade flows, with Russia increasingly exporting its liquid fuels to different markets, primarily by sea. Although we do not forecast country-level imports and exports, we monitor global trade flows to understand and anticipate changes in global petroleum market balances.

In 2021, before the invasion, 59% of Russia’s seaborne liquid fuel exports traveled relatively short distances to countries in Europe. Russia’s exports to Europe declined from 3.4 million b/d in 2021 to less than 0.9 million b/d in the first three quarters of 2023. More than 70% of those exports to Europe in 2023 were to Türkiye, which is not a member of the EU and has not sanctioned oil imports from Russia. Most of the remaining imports to Europe in 2023 were allowed under sanctions and imported to the EU, including product imports before February 5, 2023; imports of natural gas condensates; and imports into Bulgaria and Croatia, which have temporary exemptions from EU Sanctions.

Since 2021, Russia’s liquid fuel trade flows have increasingly shifted away from Europe and North America. Instead, Russia’s petroleum exports have been shipped longer distances to China, India, and numerous countries in the Middle East, Africa, and South America.

Russia’s exports have become harder to track, either through deliberate obfuscation or simply through longer supply chains that often include ship-to-ship transfers or off-loading cargo to storage facilities that are not the final destination. Thus, export figures based on tanker tracking may overcount exports to some destinations while undercounting exports to others, such as volumes offloaded in Malaysia which may ultimately end up in China.

Although the global oil market has adjusted relatively quickly to sanctions since the invasion and the resulting effect on global oil supplies and consumer fuel prices has been limited, several factors affecting global oil market uncertainties remain. Future actions taken by OPEC+ members remain uncertain, as do the future implementation and enforcement of sanctions against Russia’s exports, which have the potential to alter Russia’s future production of liquid fuels.

In our most recent STEO forecasts, we’ve expected that Russia’s production of liquid fuels will remain relatively flat in 2024 at 10.7 million b/d, with the assumption that upside and downside risks are largely balanced and existing sanctions will limit growth in Russia’s production from current levels, but the backdrop of heightened uncertainty could meaningfully affect our forecast in future editions.