Is the seasonal gasoline price peak behind us?

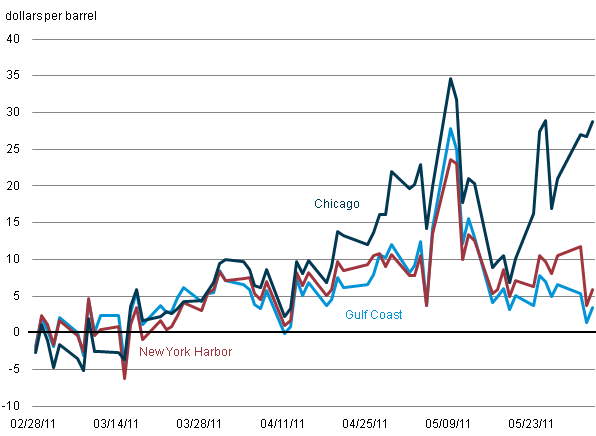

Regional gasoline crack spreads

Note: Crack spreads are calculated by subtracting LLS crude oil spot price from the conventional gasoline spot price.

Gasoline crack spreads, which measure the difference between the selling price of finished products and the purchase price of crude oil, rose sharply toward the end of April, but fell recently. Although risks still linger, there are reasons to think that, for most regions, the summer weekly gasoline peak price may be behind us. EIA's Short-Term Energy Outlook (STEO), published in May, projected June retail prices averaging $3.88 per gallon nationally, about the same as in May, with prices continuing to ease over the rest of the summer, averaging $3.76 per gallon during August. The May 11, 2011 edition of This Week in Petroleum discussed a rule of thumb for estimating retail prices from the reformulated gasoline blendstock for oxygenated blending (RBOB) futures contract. Following a sharp drop in RBOB prices since the STEO publication, that rule of thumb would imply retail prices as low as $3.65 per gallon in August.

Disruptions in crude oil supply resulting from unrest in the Middle East and North Africa have been widely recognized as important sources of oil - and in turn gasoline- price increases since the beginning of the year. More recently, however, unusually wide gyrations in wholesale gasoline prices have shown that downstream factors closer to consumer markets can also greatly affect prices at the pump. Factors behind these changes included:

- Unplanned refinery outages in the Gulf Coast and the East Coast: Unplanned outages seem to account for most of the gasoline crack pressure in April. The East Coast lost 17% of its operable crude distillation capacity on average during April, and 23% of its fluid catalytic cracking (FCC) unit capacity. (FCC units are large gasoline-producing units.) The Gulf Coast lost, on average, 7% of its crude oil input capacity during April, compared to a typical 4%, and 9% of its FCC capacity versus a typical 6%. There have been additional refinery outages in late May and early June in the Midwest, which have led to increasing crack spreads in the Chicago market over the last two weeks. As refineries return to normal operation, and barring additional unplanned outages, refineries east of the Rocky Mountains should be running at more normal levels in June.

- Supply did not keep up with demand: Low production, combined with only slightly elevated imports and likely strong exports caused inventories to decline sharply. East Coast gasoline inventories normally fall about 3 million barrels from the end of February through the end of April. This year they fell about 15 million barrels—or 5 times the typical amount. Midwest gasoline inventories were already at low levels in February and fell about 6.5 million barrels by the end of April, which is slightly higher than the typical 6 million barrels.

- Concerns over refinery and pipeline flooding: In early May, concerns about renewed supply disruption risks on the Gulf Coast from refinery and pipeline flooding, particularly in Louisiana, brought further price pressure. However, after the Morganza Spillway on the Mississippi River was opened on May 14, waters rose less than expected, implying less potential for serious petroleum supply disruptions. Gasoline spot prices dropped significantly on Monday, May 16, falling about 16-18 cents per gallon in many regions, and about 26 cents per gallon in Chicago.

This Week in Petroleum, released May 18, provides further insight into the unusual regional crack spreads this Spring.

Tags: crack spread, crude oil, gasoline, liquid fuels, oil/petroleum, prices