EIA projects rise in U.S. crude oil and other liquid fuels production beyond 2017

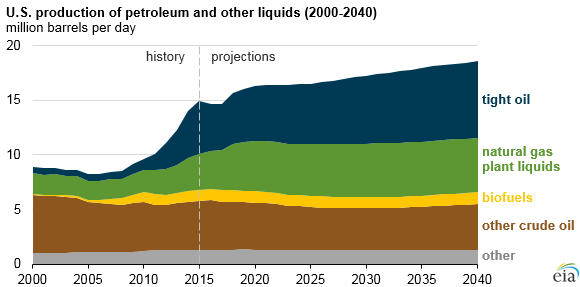

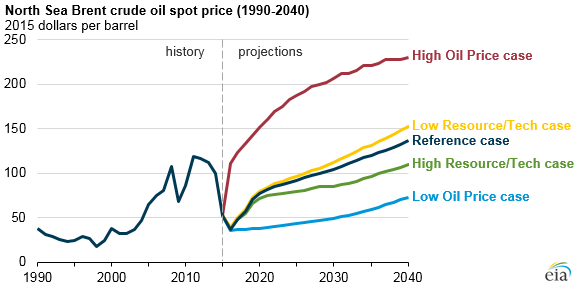

The U.S. Energy Information Administration projects that U.S. petroleum and other liquid fuels production, which in addition to crude oil and condensate production includes natural gas plant liquids derived from natural gas processing as well as biofuels and volume gain at refineries, is projected to grow from 14.8 million barrels/day (b/d) in 2015 to 18.6 million b/d in 2040 in its Annual Energy Outlook 2016 (AEO2016) Reference case. Given the uncertainty inherent in making projections, AEO2016 also includes several alternative cases, based on different assumptions for world oil prices, macroeconomic growth, resource availability, technology improvement, and other factors. Differences in crude oil from tight formations (tight oil) and natural gas plant liquids (NGPL) account for most of the differences in production across these cases.

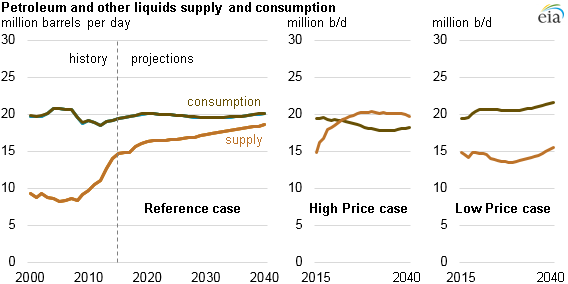

The oil price cases illustrate the effect of higher or lower global crude oil prices on U.S. production and use of petroleum. By 2030, the Brent crude oil spot price averages $49/b in the Low Oil Price case, $104/b in the Reference case, and $207/b in the High Oil Price case. In the High Oil Price case, increased energy efficiency, conservation, and fuel switching reduce projected consumption. The converse is true in the Low Oil Price case, where demand increases in response to low prices. In the High Oil Price case, the United States becomes a net exporter of petroleum and other liquid fuels by 2022.

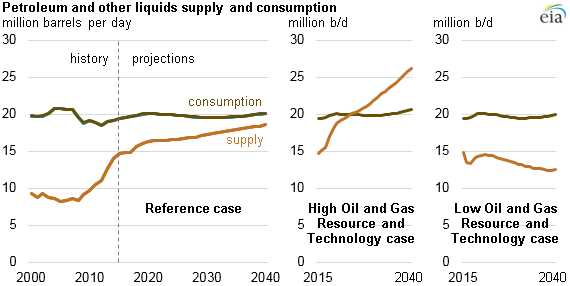

In the resource and technology cases, the estimated ultimate recovery for shale gas, tight gas, and tight oil wells in the United States, undiscovered resources in Alaska, and the offshore Lower 48 states are 50% higher or 50% lower than in the Reference case. Rates of technological improvement that reduce costs and increase productivity in the United States are also 50% higher or 50% lower than in the Reference case. In the High Oil and Gas Resource and Technology case, the United States becomes a net exporter of petroleum and other liquid fuels by 2024.

Tight oil. In the Reference case, relatively low prices through 2017 have the greatest effect on tight oil production, which drops to 4.2 million b/d in 2017 before increasing to 7.1 million b/d in 2040. The increase in tight oil production is largely attributed to higher oil prices and the ongoing exploration and development programs that expand operator knowledge about producing reservoirs. Of all the crude oil and liquids types, tight oil changes the most across cases: in the High and Low Resource/Technology cases, tight oil production in 2040 ranges from 3.12 million b/d in the Low Resource/Technology case to 12.9 million b/d in the High Resource/Technology case.

Natural gas plant liquids. Production of NGPL increases throughout the Reference case projection, from 3.3 million b/d in 2015 to 4.8 million b/d in 2025, and then more slowly through 2040, reaching 5.0 million b/d as growth in wet natural gas production slows. Future NGPL production depends on both domestic resources and the differential between crude oil prices and natural gas prices.

Offshore and Alaska crude oil. Production in Alaska continues to decline through 2040, dropping to less than 0.2 million b/d in 2040. Offshore production is less sensitive to short-term price movements than onshore production.

Biofuels. Supply from renewable sources grows slowly throughout the projection, and is less sensitive to price assumptions, remaining at about 1 million b/d throughout the projection across the oil price cases.

Other liquid fuels. Neither gas-to-liquids nor coal-to-liquids contribute to domestic production in most of the AEO2016 cases because of the risks associated with their high capital costs, long construction lead times, and the likelihood they will not remain price-competitive with crude oil over facility lifetimes. However, both become economic in the High Oil Price case after 2020, combining to add 1.1 million b/d to domestic liquid fuel supply by 2040.

Principal contributor: Laura Singer