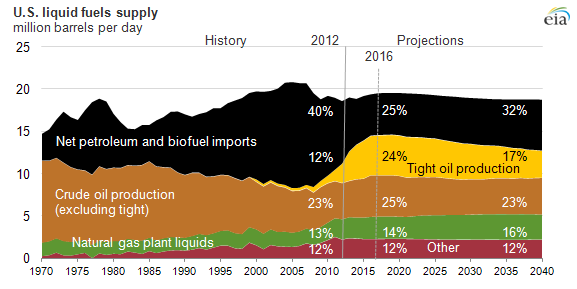

Increased tight oil production, vehicle efficiency reduce petroleum and liquid imports

Note: Other includes refinery gains, biofuels production, all stock withdrawals, and other domestic sources of liquid fuels.

The U.S. Energy Information Administration's Annual Energy Outlook 2014 Reference case shows that recent growth in domestic crude oil and natural gas production is expected to continue for many years. In 2016, crude oil production is expected to be close to the historical high of 9.6 million barrels per day, a record set in 1970. The AEO2014 Reference case was released at 9:30 a.m. EST today. It contains baseline projections for U.S. energy production, consumption, and imports through 2040.

While domestic crude oil production is projected to level off and then slowly decline after 2020, natural gas production grows steadily, with a 56% increase between 2012 and 2040, when production reaches 37.6 trillion cubic feet. The full AEO2014 report, to be released next spring, will also consider alternative resource and technology scenarios, some showing significantly higher long-term oil production than in the Reference case.

Some other key findings of the AEO2014 Reference case include:

Low natural gas prices boost natural gas-intensive industries. Industrial shipments are expected to grow at 3.0% per year over the first 10 years of the projection and then slow to 1.6% annual growth through 2040. Bulk chemicals and metals-based durables account for much of the increased growth in industrial shipments. Industrial shipments of bulk chemicals, which benefit from an increased supply of natural gas liquids, grow by 3.4% per year from 2012 to 2025. The competitive advantage in bulk chemicals diminishes in the long term. Industrial natural gas consumption is projected to grow by 22% between 2012 and 2025.

Natural gas overtakes coal as the largest fuel for U.S. electricity generation. Projected low prices for natural gas make it a very attractive fuel for new generating capacity. In some areas, natural gas-fired generation replaces power formerly supplied by coal and nuclear plants. In 2040, natural gas accounts for 35% of total electricity generation, while coal accounts for 32%. Generation from renewable fuels, unlike coal and nuclear power, is higher in the AEO2014 Reference case than in AEO2013. Electric power generation from renewables is bolstered by legislation enacted at the beginning of 2013 extending tax credits for generation from wind and other renewable technologies.

Higher natural gas production supports increased exports of pipeline and liquefied natural gas (LNG). In addition to increases in domestic consumption in the industrial and electric power sectors, U.S. exports of natural gas also increase in the AEO2014 Reference case. U.S. exports of LNG increase to 3.5 trillion cubic feet (Tcf) before 2030 and remain at that level through 2040. Pipeline exports of natural gas to Mexico grow by 6% per year, from 0.6 Tcf in 2012 to 3.1 Tcf in 2040. Pipeline exports to Canada grow by 1.2% per year, from 1.0 Tcf in 2012 to 1.4 Tcf in 2040. Over the same period, pipeline imports from Canada fall by 30%, from 3.0 Tcf in 2012 to 2.1 Tcf in 2040, as more demand is met by domestic production.

Car and light truck fuel use declines sharply. AEO2014 includes a new, detailed demographic profile of driving behavior by age and gender as well as new, lower population growth rates based on updated Census Bureau projections. As a result, annual increases in vehicle miles traveled (VMT) in light-duty vehicles (LDV) average 0.9% from 2012 to 2040, compared to 1.2% per year projected over the same period in AEO2013. The rising vehicle fuel economy of LDVs more than offsets the modest growth in VMT, resulting in a 25% decline in LDV energy consumption between 2012 and 2040 in the AEO2014 Reference case.

The full AEO2014 will be released this spring with side cases that examine the effect of alternative resource and demand assumptions as well as changes to some existing policies on the energy sector.

Principal contributors: EIA Staff