U.S. ENERGY INFORMATION ADMINISTRATION

WASHINGTON DC 20585

FOR IMMEDIATE RELEASE

MAY 11, 2010

EIA Assesses Impact of Economic Growth, Oil Prices, and

Future Policies on Projected Energy Trends

WASHINGTON, DC - The U.S. Energy Information Administration (EIA) today released the complete version of the Annual Energy Outlook 2010 (AEO2010), which includes 38 sensitivity cases that show how different assumptions regarding market and policy drivers affect the Reference case projections that EIA previously released in December, 2009. In addition to considering alternative scenarios for oil prices, economic growth, and the uptake of more energy-efficient technologies, the AEO2010 includes cases that examine the impact of changes in selected policies, such as the extension of existing policies that are currently scheduled to sunset as well as the sensitivity of natural gas shale production to variations in drilling activity and the size of the resource base.

The AEO2010 sensitivity cases show that "variations in assumptions regarding key market or policy drivers can have a significant impact on projected energy market trends," said EIA Administrator Richard Newell. He noted that “understanding these potential alternate energy futures can inform individuals, businesses, and policy makers as they make decisions today.”

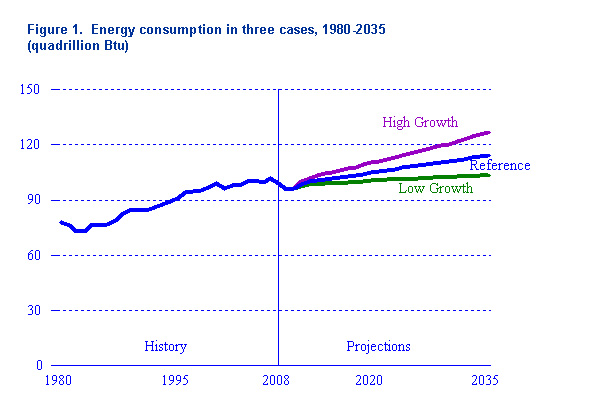

The projected level of total U.S. energy use depends significantly on the rate of economic growth, which is assumed to be 2.4 percent annually from 2008 to 2035 in the AEO2010 Reference case. Annual average economic growth rates of 1.8 percent in the Low Economic Growth case and 3.0 percent in the High Economic Growth case, correspond to projections of energy use in 2035 ranging from about 104 to 127 quadrillion Btu, increases of between 0.1 percent to 0.9 percent annually (Figure 1). Changes in the size of the economy lead to less than proportional changes in projected U.S. energy use because improvements in energy intensity vary with rates of economic growth.

The AEO2010 Reference case does not include potential future policies that have not yet become law and assumes that existing laws expire as currently specified. Some laws, however, have a history of being extended or periodically updated. The AEO2010 No Sunset case and Extended Policies case examine the impacts of extending and updating various policies. Projected energy use in both these cases is below the Reference case level. By 2035, projected energy-related carbon dioxide emissions are 2.3 percent lower in the No Sunset case and 3.2 percent lower in the Extended Polices case than in the Reference case (Figure 2).

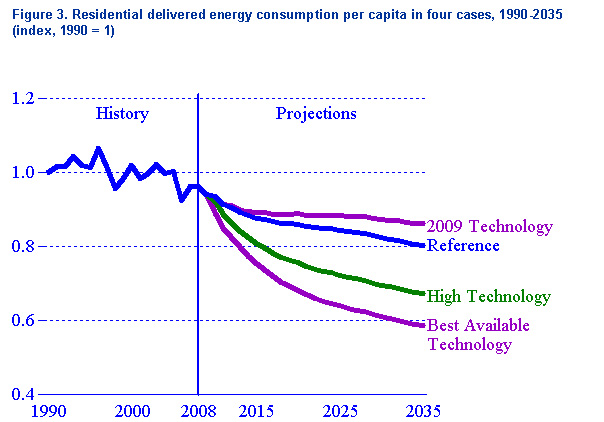

The rate of energy efficiency improvement will also have a major impact on the future level of energy consumption. Total delivered residential energy consumption grows 0.2 percent from 2008 levels to 12.1 quadrillion Btu by 2035 in the AEO2010 Reference case, assuming historical rates of technological progress in residential equipment and appliances. However, in the Buildings Best Technology case, if residential consumers are assumed to uniformly adopt the best available technology (ignoring cost), total residential consumption could be over 27 percent lower in 2035 (Figure 3). Equipment cost, consumer preference for a shorter payback period, and other barriers to the selection of the best available technology can, however, inhibit adoption of the best available technology.

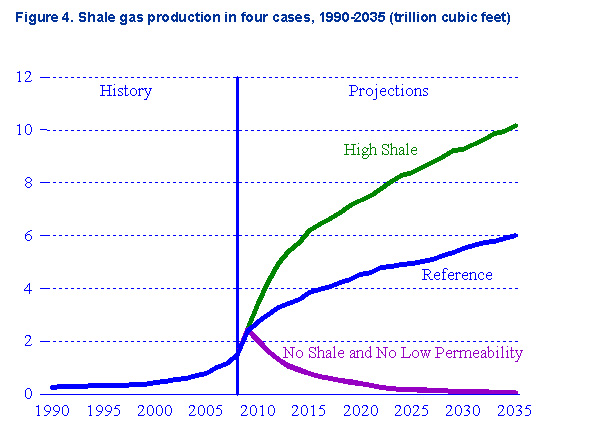

EIA expects that the level of shale gas production will significantly influence U.S. natural gas prices, production, imports, and consumption in the future. However, there is considerably uncertainty regarding the size of low permeability natural gas resources and concerns have also been raised regarding the environmental impacts of accessing those resources. The AEO2010 includes three sensitivity cases to examine the implications of those uncertainties. In the No Shale Drilling case there is no new onshore, lower 48 shale drilling after 2009, while in the No Low Permeability Drilling case there is no new onshore, lower 48 shale or tight sands drilling after 2009. In contrast, the High Shale Gas Resource case increases unproven shale gas resources in the AEO2010 from 347 trillion cubic feet to 652 trillion cubic feet. Natural gas prices and production vary significantly across these cases. Henry Hub spot natural gas prices range from $7.62 to $10.88 per million Btu (all in 2008 dollars) in 2035 from the High Shale Gas Resource case to the No Low Permeability Gas Drilling case and total U.S. production in 2035 ranges from 17.4 to 25.9 trillion cubic feet, with most of the variation reflecting changes in shale gas production (Figure 4).

The projections from the complete AEO2010, including the Reference case, all of the alternative cases, supplemental tables showing the regional projections, as well as a report on the major assumptions underlying the projections, can be accessed on EIA’s Internet site at www.eia.gov/oiaf/aeo/index.html.

EIA Program Contact: John Conti, 202-586-2222, John.Conti@eia.gov

EIA Press Contact: Jonathan Cogan, 202-586-8719, Jonathan.Cogan@eia.gov

EIA-2010-05