Natural gas

Natural gas prices

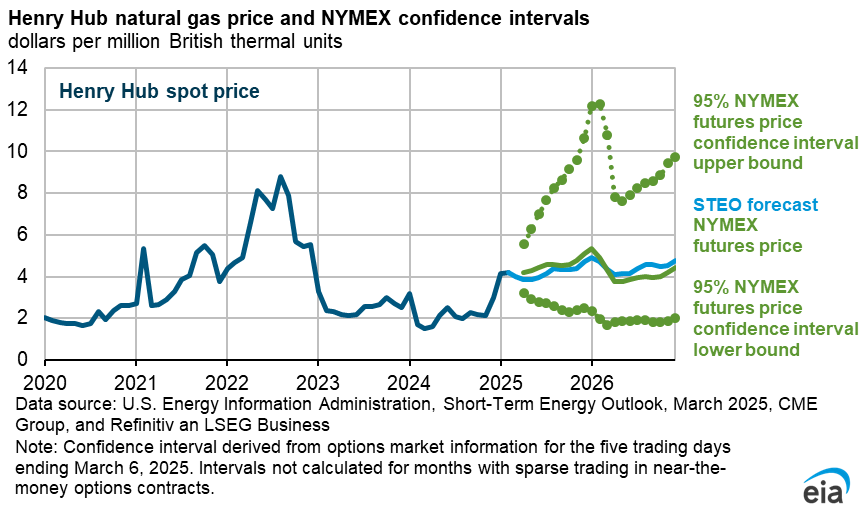

We forecast that natural gas prices will remain relatively flat in the upcoming shoulder season of September and October before generally rising in 2025. The U.S. benchmark Henry Hub natural gas price averaged $1.98 per million British thermal units (MMBtu) in August, down 4% from July.

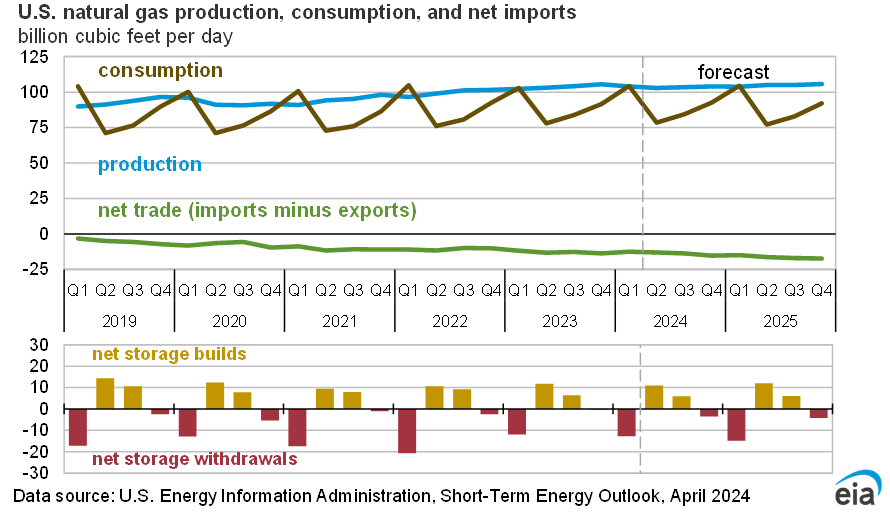

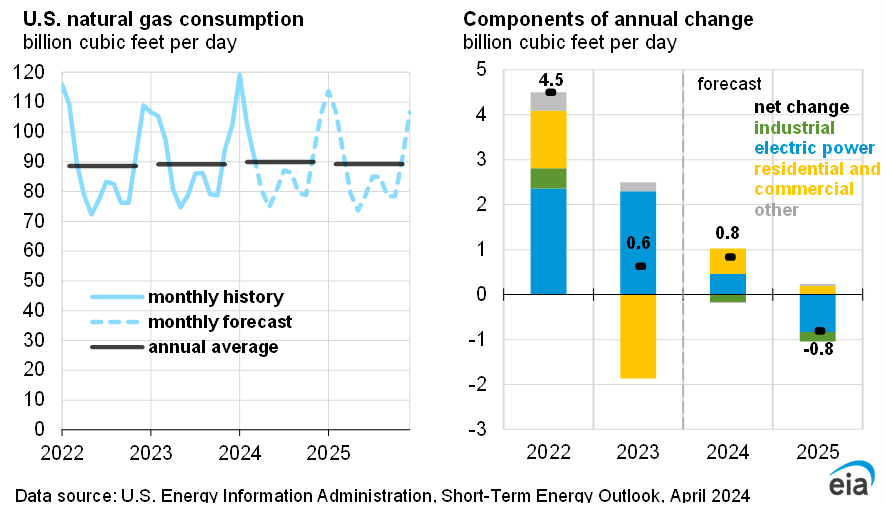

September Henry Hub prices in our forecast remain close to prices in August, as we enter the shoulder season when less natural gas is consumed overall and before demand for space heating increases in the United States. We expect U.S. natural gas consumption to decline by 8% to 79 billion cubic feet per day (Bcf/d) between August and September.

With relatively flat production and reduced natural gas consumption because of a seasonal decrease in demand from the electric power sector, we expect the Henry Hub natural gas spot price to stay close to $2.00/MMBtu the next couple of months and remain below $3.00/MMBtu through the end of 2024.

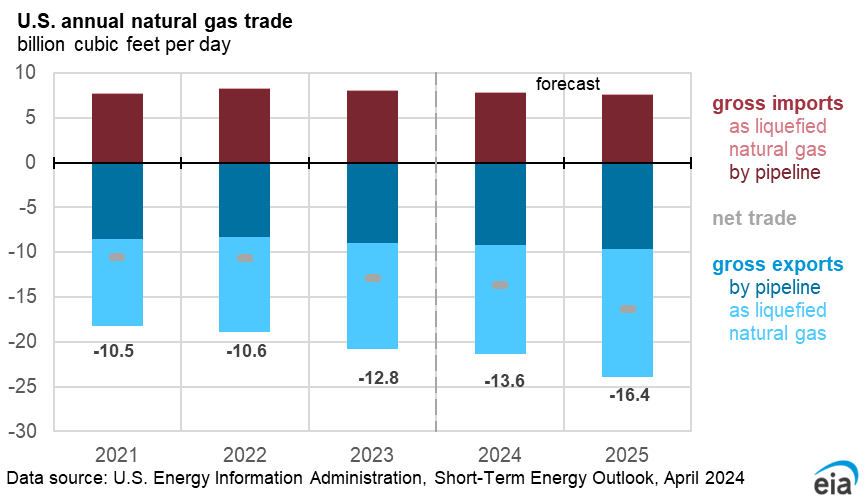

In 2025, we expect prices to rise as liquefied natural gas (LNG) exports increase while domestic consumption and production remain relatively flat for much of the year. We forecast U.S. consumption of natural gas to average about 90 Bcf/d in 2025, which is about the same as our forecast for total consumption in 2024. However, we expect that LNG exports will rise by more than 2 Bcf/d (17%) next year as export capacity expands.

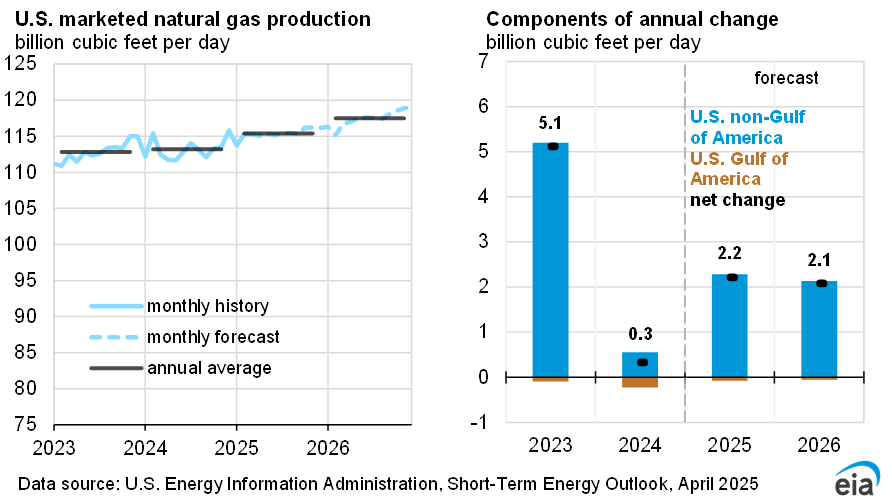

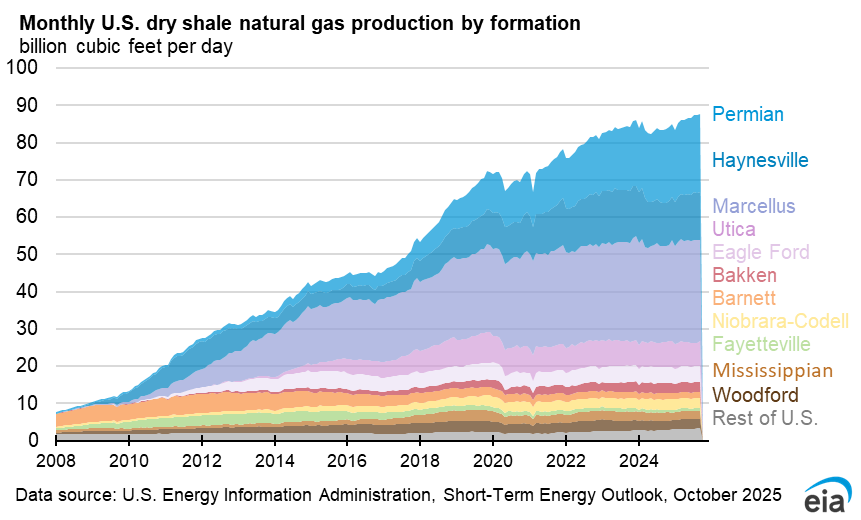

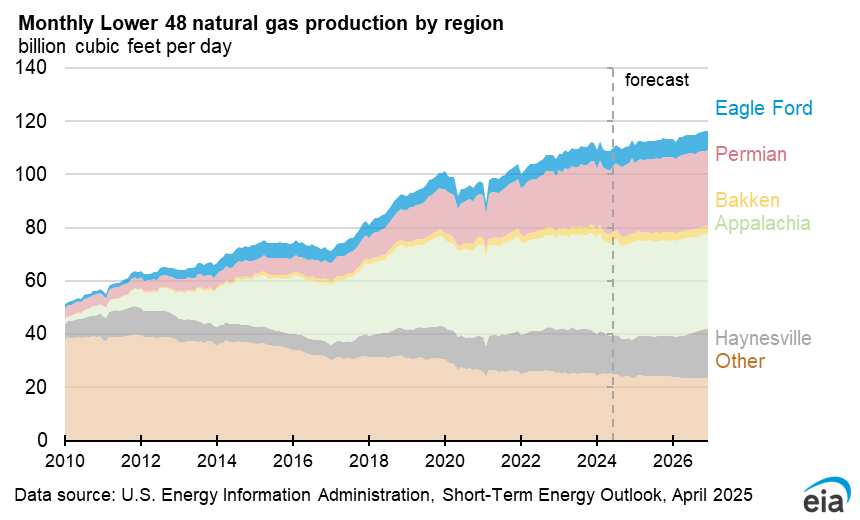

We expect U.S. dry natural gas production will remain relatively unchanged over the next several months as some producers, particularly in the Marcellus and Haynesville regions, continue to curtail production until prices rise. U.S. dry natural gas production averages 104 Bcf/d in 4Q24 in our forecast and 105 Bcf/d during 2025. Most of the growth in natural gas production comes in late 2025 when we expect new LNG export facilities to ramp up production. We forecast the Henry Hub price to average around $2.20/MMBtu in 2024 and $3.10/MMBtu in 2025.

Natural gas storage

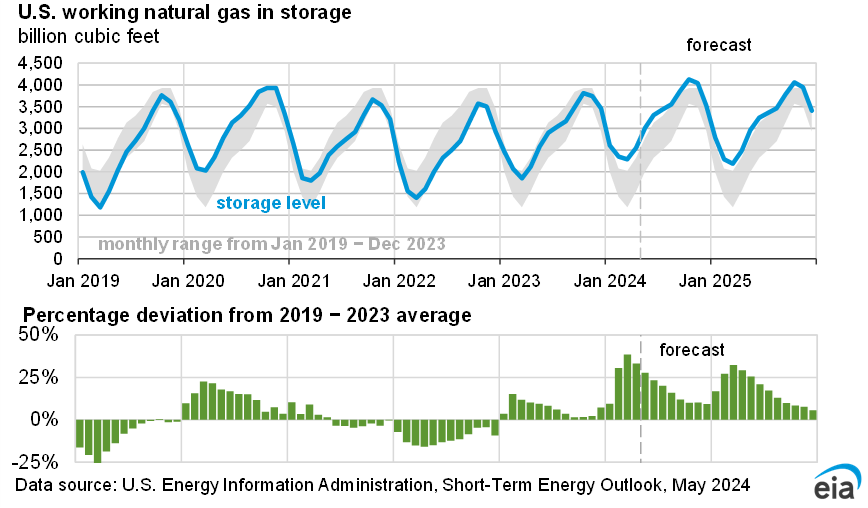

We expect less natural gas storage injections than the five-year average (2019–2023) through the remainder of this year’s injection season (April–October). Nevertheless, we expect inventories will end the injection season on October 31 with 5% more natural gas than the five-year average, down from a surplus of 11% at the end of August. Our anticipation of a narrowing surplus to the five-year average supports our expectation of rising prices in the coming months. If U.S. natural gas production is less than our forecast and consumption increases, leading to inventories ending the injection season closer to the five-year average, natural gas prices could be higher than forecast. At the same time, with peak hurricane season approaching, if LNG exports were disrupted because of a hurricane on the Gulf Coast, resulting in more U.S. inventories than expected, natural gas prices could be lower than in our forecast.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}