Wind energy tax credit set to expire at the end of 2012

Note: Click to enlarge.

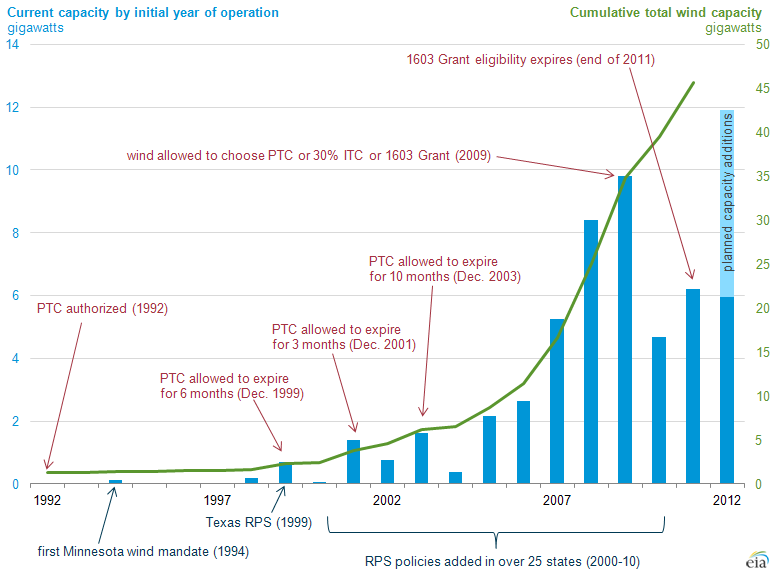

Note: Data for 2012 planned additions are based on industry data submissions and monthly updates on planned wind facilities. Left-hand axis plots current capacity of existing generators by their initial date of operation. Capacity may change over time as generators are altered. For recent years, these data are synonymous with capacity additions. Early in the time period, this data series may be missing generators that have since retired.

The wind energy production tax credit (PTC), along with state-level policies, has boosted the growth of the U.S. wind industry over the past decade, but the PTC is set to expire at year-end unless legislation extending its provisions is approved. This tax credit was first implemented in 1992, when the United States had less than 1.5 gigawatts (GW) of installed wind capacity. By the end of 2011, wind capacity stood at more than 45 GW, about 4% of U.S. power generating capacity, and provided 3% of total U.S. electricity generation in 2011. Wind's generation share is below its capacity share because wind's capacity utilization is limited to windy periods. Data reported to EIA for 2012 point to another year of significant wind capacity additions, following a trend of increasing capacity additions in anticipation of a PTC expiration.

Since its implementation in 1992, the PTC has significantly contributed to wind development in the United States by increasing the financial return on a wind energy investment and allowing wind plants to price their generation more competitively. The cycle of expirations and reauthorizations of the wind PTC (see red labels in chart) during the past decade has had a noticeable effect on wind development through its impact on the planning and financing of wind energy projects.

The PTC was first enacted as part of the 1992 Energy Policy Act as a replacement for prior incentives for wind generation under the Public Utility Regulatory Policies Act of 1978 and an investment tax credit (ITC) first made available under the Energy Tax Act of 1978. The PTC is a credit based on annual production of electricity from eligible resources. The initial tax credit of 1.5 cents per kilowatthour (1992 dollars) for the first 10 years of output from plants entering service by December 31, 1999, included an annual adjustment for inflation and is currently valued at 2.2 cents per kilowatthour (2011 dollars). Although amendments to the original law have expanded it to a wide variety of renewable resources and technologies, the original PTC applied to generation from tax-paying owners of new wind plants, as well as eligible biomass power plants.

In its early years, the PTC had little discernible effect on the industries it was designed to support. By 1999, when the provision was originally set to expire, U.S. wind capacity had begun growing again, and the PTC supported the development of more than 500 megawatts of new wind capacity in California, Iowa, Minnesota, and other states that had implemented policies to support or require renewable generation capacity.

State-level programs encouraged wind power development. For example, the mandate in Minnesota for 425 megawatts of wind power by 2003 was part of a settlement with Northern States Power (now Xcel Energy) to extend on-site storage of nuclear waste at its nuclear facility. In 1999, Texas became the first state to implement a renewable portfolio standard (RPS) for a competitive electricity supply market.

Cycles of expiration and reauthorization. From 1999 to 2004, Congress allowed the PTC to expire three times, each time retroactively extending it several months after the expiration deadline had passed. The two-year cycle of expiration and re-extension is apparent (see chart, starting in 1999). In the 12-month period immediately prior to the expiration dates (which, after 1999, were always pegged to the last day of the calendar year), new installations reached high levels as developers rushed to beat the legislative deadline, followed by a substantial retrenchment in the following year as the status of the tax credit was sorted out.

Congress has not allowed the PTC to expire since passage of the Working Families Tax Relief Act of 2004. In the period from 2005 to 2010, the wind industry experienced a period of consistent year-over-year growth. This growth occurred as the number of states with renewable power requirements increased.

Recession and recovery. The break in this growth streak occurred in 2010, as an echo effect of the financial crisis and recession from late 2008 and 2009. While wind projects were still eligible for tax credits, a lack of investors with sufficient tax appetite, or tax-situation ability to take advantage of the credits, a general decline in the need for new sources of generation, and a decline in natural gas prices that hurt the competitiveness of wind on a cost basis all contributed to slower growth for wind capacity in 2010.

In 2009, as part of the American Recovery and Reinvestment Act (ARRA), Congress modified the PTC to address the tax appetite issue. In particular, the ITC was reintroduced for wind and other PTC-eligible technologies at a 30% level. In addition, projects starting construction before the end of 2011 may elect to receive an equivalent-value cash grant in lieu of the ITC (known as a 1603 Grant after its ARRA section number), thus mitigating the need for investors with sufficient tax burdens to be offset by the ITC.

Recent events. In 2011, wind power construction began to rebound from the 2010 retrenchment, largely with projects taking advantage of the 1603 Grant before its expiration. The trend has continued through 2012, with approximately 6 GW of new installations through October and another 6 GW expected to enter service in the last months of the year, as reported to EIA by project developers. If all reported capacity installations are completed as reported to EIA, 2012 would again set a record for new wind installations in the United States. In 2011, installed wind capacity stood at more than 45 GW, and generated almost 120 million megawatthours of electricity, accounting for about 4% of U.S. installed capacity and 3% of total U.S. generation in 2011.

Currently, the PTC is scheduled to expire for new wind generators entering service after the end of 2012. Other PTC-eligible technologies may continue to receive this tax credit for facilities that begin operation during 2013. Eligibility of these projects for the ITC will expire at the same time as eligibility for the PTC (end of 2012 for wind, end of 2013 for other PTC-eligible technologies). Projects that were under construction before the end of 2011 will still be eligible for a 1603 Grant, as long as they enter service prior to expiration of the PTC or ITC for their technology class.