Liquefied natural gas meets a quarter of New England's average natural gas needs

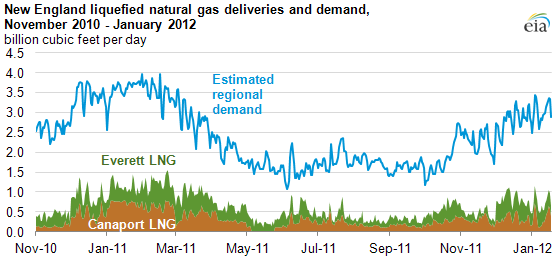

Note: LNG send-out (deliveries) from the 1.2 Bcfd Canaport LNG regasification terminal in New Brunswick, Canada serves both the U.S. New England market and regional demand within Canada. The majority of the send-out goes to New England through the Millennium Pipeline. Daily natural gas demand for New England estimated by Bentek Energy, LLC based on information reported by natural gas pipelines.

Liquefied natural gas (LNG) has met over 25% of New England's average daily natural gas demand since November 2010. Four LNG regasification facilities can provide LNG to New England—Canaport, Everett, Neptune, and Northeast Gateway. Most of New England's LNG deliveries come from the Canaport terminal in New Brunswick, Canada and the Everett terminal in Boston. Canaport's deliveries destined for the United States show up as pipeline imports from Canada. LNG facilities are important sources of natural gas supply for New England as pipeline deliveries into the region from gas-producing regions in North America are often constrained during periods of high demand.

The role of these LNG facilities highlights a few important dynamics of the natural gas market:

- The Northeast U.S. natural gas market. Natural gas in the Northeast trades at premium prices compared to the rest of the United States due to pipeline constraints during periods of high demand in the winter. These constraints can put upward pressure on local natural gas prices, which can then be relieved to some degree by additional natural gas supply from LNG terminals. For much of the 2010-2011 winter, the Canaport and Everett LNG facilities delivered 1-1.5 Bcfd of natural gas into New England, an important source of supply to this constrained market.

- Relative world natural gas prices. Companies in the United States compete for LNG supplies in a global marketplace. Since 2009, growing domestic gas production has contributed to average wellhead and wholesale natural gas prices typically ranging between $3 and $5 per million Btu (MMBtu). Natural gas prices in Europe and Asia have ranged much higher, reaching $10-$16/MMBtu. As a result, other LNG markets are typically served first, and the United States has become more of a residuals market for LNG supplies not served under long-term contracts. Most U.S. LNG terminals have seen very low utilization levels in recent years.

- LNG contract terms. Because of the lower-priced domestic natural gas market, most, if not all, recent LNG deliveries to the United States arrived under long-term supply contracts. The Canaport and Everett LNG facilities both have long-term contracts while the Neptune and Northeast Gateway facilities, like most others in the United States, do not have long-term supply contracts and have not received regular LNG deliveries.