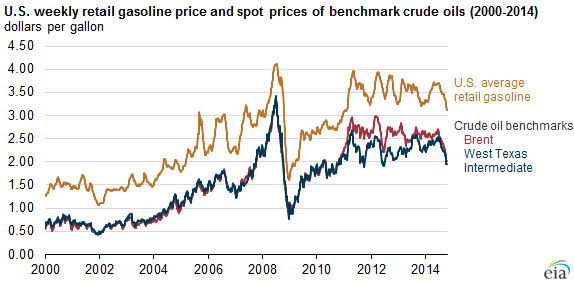

U.S. gasoline prices move with Brent rather than WTI crude oil

Recent increases in U.S. crude oil production have sparked discussion on how this increase in supply will be used by U.S. refiners given current limitations on exporting domestic crude. On October 30, EIA released a study that explored the relationships between crude oil and gasoline prices.

Key findings from the analysis include:

- Prices of Brent crude oil, an international benchmark, are more important than the price of West Texas Intermediate (WTI), a domestic benchmark, for determining gasoline prices in all four U.S. regions studied, including the Midwest.

- The effect that a relaxation of current limitations on U.S. crude oil exports would have on U.S. gasoline prices depends on its effect on international crude prices, such as Brent, rather than its effect on domestic crude prices.

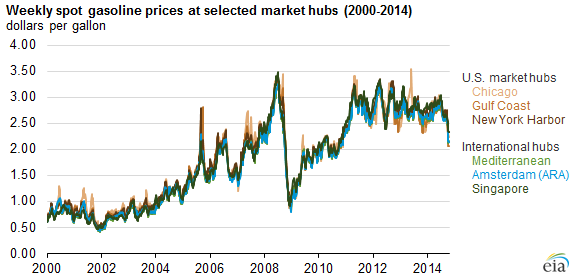

- Gasoline is a globally traded commodity, and prices are highly correlated across global spot markets.

- Gasoline supply, demand, and trade in various regions are changing; one effect is that U.S. Gulf Coast and Chicago spot gasoline prices, which are closely linked, are now often the lowest in the world during fall and winter months.

A change in current limitations on crude oil exports could have implications for both domestic and international crude oil prices. Such a relaxation could raise the prices of domestically produced oil. If higher prices for domestic crude were to spur additional U.S. production than might otherwise occur, the increase to global crude oil supply could reduce the global price of crude.

The extent to which domestic crude prices might rise, and global crude prices might fall, depends on a host of factors, including the degree to which current export limitations affect prices received by domestic producers, the sensitivity of future domestic production to prices changes, the ability of domestic refiners to absorb domestic production, and the reaction of key foreign producers to changes in the level of U.S. crude production.

Relationships between gasoline and crude oil prices

U.S. retail gasoline prices reflect four key components: the price of crude oil; refining costs and profit margins; retail and distribution costs and profit margins; and taxes. The first two factors tend to be more volatile, causing most of the variation in retail gasoline prices, while the latter two reflect the retail portion and tend to be relatively stable.

A general guideline for how crude oil prices affect gasoline is that a $1-per-barrel change in the price of crude oil translates into a change of about 2.4 cents per gallon of gasoline. (There are 42 gallons in one barrel, and 2.4 cents is about 1/42 of $1.)

While there are many crude oils traded around the globe, two of the major benchmark light sweet crudes are West Texas Intermediate (WTI) and North Sea Brent. Before 2010, there was little reason to specify which crude oil price was more important with respect to effects on domestic gasoline prices, as the two benchmarks traded at similar prices. In mid-2010, more Canadian exports to the U.S. Midwest and increased production in the United States led to transportation constraints, which caused the price of WTI to fall below the Brent price. The surge of domestic production also reduced U.S. crude imports.

However, the lower WTI prices did not result in lower U.S. gasoline prices because, as EIA's analysis shows, U.S. gasoline prices are more closely linked to the price of Brent. The analysis shows this is the case in all parts of the country, including the Midwest, where the trading hub for WTI is located (Cushing, Oklahoma).

Gasoline itself is also a globally traded commodity, and the United States both imports and exports gasoline and other finished products. The graph below shows prices at trading hubs around the world: New York Harbor, U.S. Gulf Coast, and Chicago, as well as Singapore, the Mediterranean, and Amsterdam-Rotterdam-Antwerp (ARA). These prices trade within a relatively narrow band, and the prices between different points reflect the transportation costs associated with shipping gasoline from exporting markets to importing markets.

Global gasoline supply and demand patterns have been evolving. Gasoline demand in Asia, Latin America, and the Middle East has been outpacing gasoline production in those regions. In the United States, demand is declining but refinery production of gasoline has been rising, resulting in increasing exports of U.S. gasoline into the global market. Because of these changes in the market and seasonal fluctuations in U.S. gasoline demand, the gasoline spot prices in the U.S. Gulf Coast or Chicago are now often the lowest in the world during fall and winter months.

While EIA's new report provides directional insights regarding the implications for U.S. gasoline prices of a possible relaxation of current limitations on crude oil exports, it does not address the extent of any actual change in domestic production or the domestic or international price of crude oil that might follow from a decision to relax or eliminate those limitations. EIA is undertaking further analyses that will examine those issues and expects to report additional results over the coming months.

Note: Amsterdam reflects the Amsterdam-Rotterdam-Antwerp trading hub.

Principal contributor: EIA staff