U.S. ENERGY INFORMATION ADMINISTRATION

WASHINGTON DC 20585

FOR IMMEDIATE RELEASE

September 9, 2014

World liquid fuels use projected to rise 38% by 2040, spurred by growth in Asia and Middle East

World petroleum and other liquid fuels consumption will increase 38% by 2040, spurred by increased demand in the developing Asia and Middle East, according to projections in International Energy Outlook 2014 (IEO2014), released today by the U.S. Energy Information Administration (EIA).

"The growth outlook for liquid fuels use will be largely driven by demand in the developing world, especially in Asia and the Middle East," said EIA Administrator Adam Sieminski. "Those two regions combined account for 85% of the total increase in liquid fuels used worldwide over that period."

World markets for petroleum and other liquid fuels have entered a period of dynamic change—in both supply and demand. The changes in the overall market environment have led EIA to reassess its outlook for long-term global liquid fuels markets in IEO2014. IEO2104 is an abbreviated edition of the report that focuses on world liquid fuels markets. A full edition of the report that includes projections of supply and demand for all energy sources will be released in 2015.

Some key IEO2014 findings:

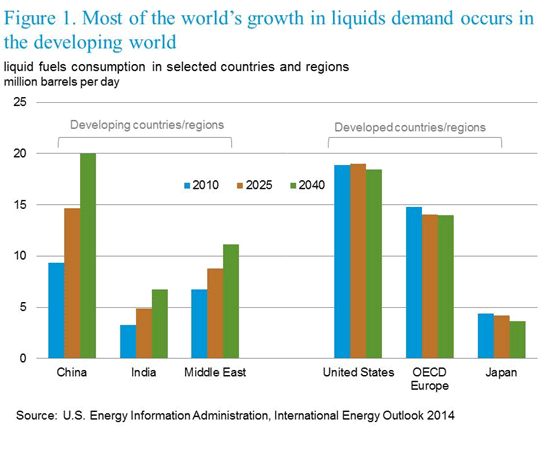

World liquid fuels use is projected to grow from 87 million barrels per day (MMbbl/d) in 2010 to 119 MMbbl/d in 2040. The potential for growth in demand for liquid fuels is focused on the emerging economies of China, India, and the Middle East, while liquid fuels demand in the United States, Europe, and other regions with well-established oil markets seems to have peaked (Figure 1). After a long period of sustained high oil prices, efficiency and fuel switching have reduced or slowed the growth of liquid fuels use among mature oil-consuming countries. Developing Asian countries (including China and India) account for 72% of the world increase in liquid fuels consumption, with Middle East consumers accounting for another 13%.

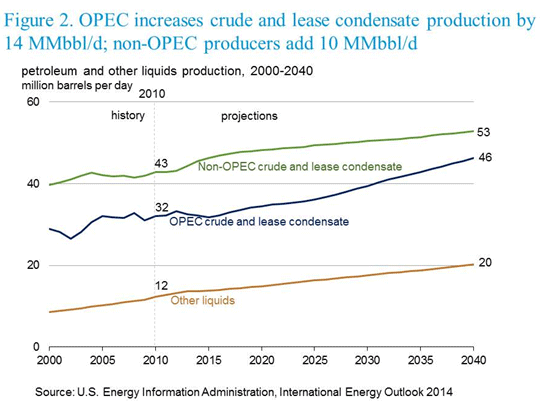

OPEC oil producers are the largest source of additional liquid fuel supply between 2010 and 2040. OPEC crude and lease condensate accounts for 14 MMbbl/d of the 33 MMbbl/d increase in total liquid fuel supply (Figure 2). The IEO2014 Reference case assumes OPEC producers invest in incremental production capacity that enables them to maintain a share of between 39% and 44% of total world liquid fuels production throughout the projection. The Middle East OPEC member countries alone account for 90% of the total growth in projected OPEC crude and lease condensate production.

Non-OPEC crude and lease condensate production increases by 10 MMbbl/d. Rising world oil prices attract investment in areas previously considered uneconomic. Potential new supplies of oil from tight and shale resources have raised optimism for large, new sources of global liquid supplies to meet growing demand. Compared to previous reports, IEO2014 incorporates larger new supplies of tight oil from the United States and Canada. However, other countries, including Mexico, Russia, Argentina, and China, begin producing substantial volumes of tight oil between now and 2040.

Other IEO2014 highlights:

- Since July 2012, North Sea Brent crude oil spot prices have generally remained in the range of $100 to $115 (nominal dollars) per barrel. Supply disruptions in several oil-producing regions, notably in North Africa and the Middle East, have been largely offset by increasing liquids supplies from the United States and Canada. In the IEO2014 Reference case, oil prices are expected to increase over the long term, with the world oil price in real 2012 dollars reaching $141 per barrel in 2040.

- Liquids other than crude and lease condensate—including natural gas plant liquids (NGPL), biofuels, coal-to-liquids (CTL), gas-to-liquids (GTL), kerogen (oil shale), and refinery gain—currently supply a relatively small portion of total world petroleum and other liquid fuels, accounting for about 14% of the total in 2010. However, they are expected to grow in importance, rising to 17% of total liquid fuels in 2040.

- Rising prices for liquid fuels improve the cost competitiveness of other fuels, leading many users of liquid fuels outside the transportation and industrial sectors to switch to other sources of energy when possible. The transportation and industrial sectors account for 92% of global liquid fuels demand in 2040. Consumption of liquid fuels in the other sectors (residential, commercial, and electric power) decreases over the projection period.

- In addition to the Reference case, the IEO2014 includes a low-oil-price scenario and a high-oil-price scenario with prices that reach $75 and $204 (real 2012 dollars) per barrel, respectively, in 2040. The price cases examine a range of potential interactions of supply, demand, and prices in world liquids markets.

IEO2014 is available at http://www.eia.gov/outlooks/ieo/.

EIA Program Contact: John Conti, 202-586-2222, john.conti@eia.gov

EIA Press Contact: Jonathan Cogan, 202-586-8719, jonathan.cogan@eia.gov

EIA-2014-08