Global oil markets

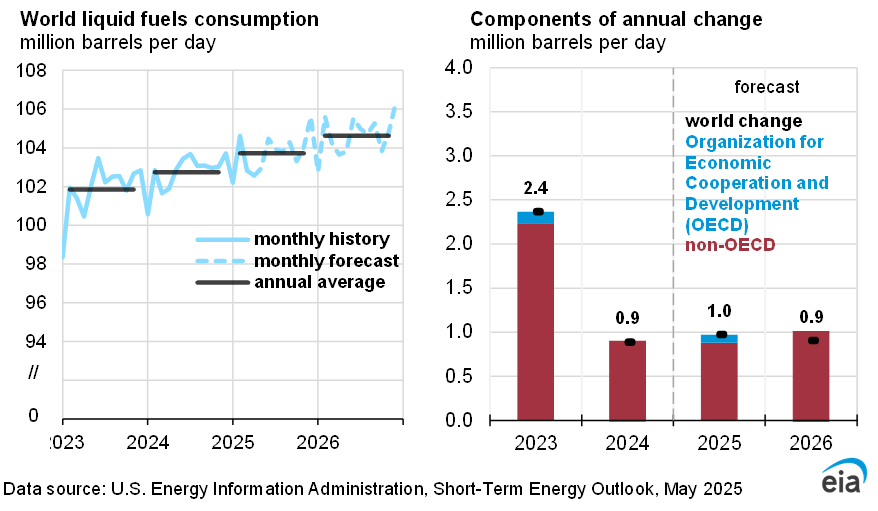

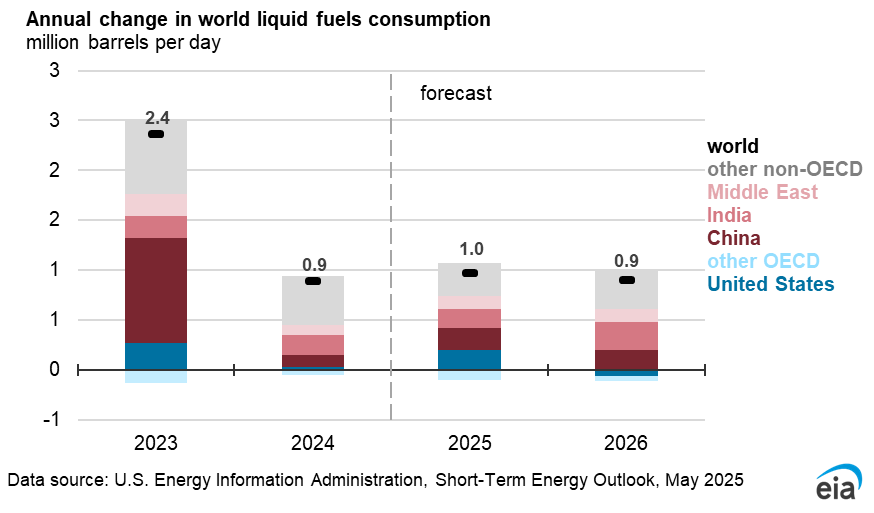

Global oil consumption

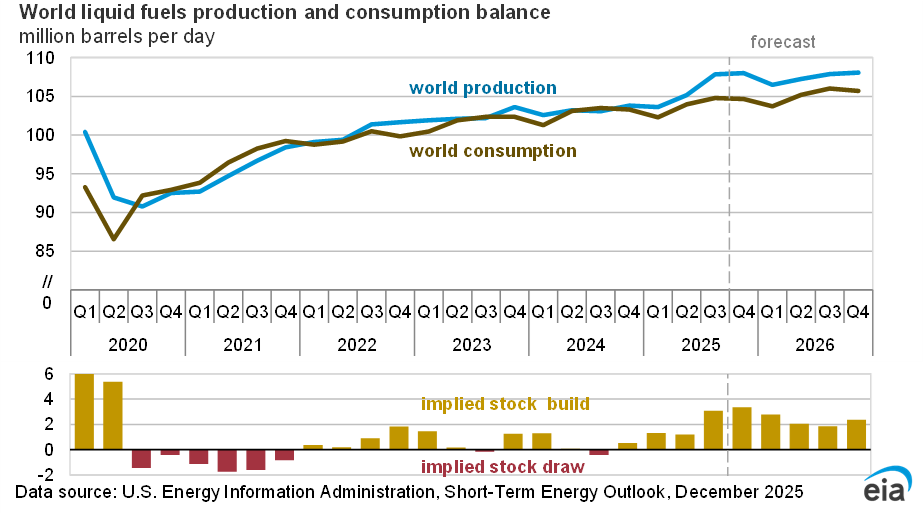

This month’s STEO incorporates the recent update to our International Energy Statistics for 2022. This update increased our assessment of global liquid fuels consumption for 2022 by nearly 0.8 million barrels per day (b/d) compared with last month’s STEO. Most of this change reflects non-OECD consumption that is higher than we previously estimated. The higher baseline historical data for 2022 in turn increased our estimate of consumption in 2023 and our forecasts for 2024 and 2025. We now estimate that global liquid fuels consumption averaged 102.0 million b/d in 2023, a 2.0 million b/d increase from 2022 and about 1.0 million b/d higher than in last month’s STEO. Global liquid fuels consumption in our forecast now averages 102.9 million b/d in 2024 and 104.3 million b/d in 2025, which is between 0.4 million b/d and 0.5 million b/d more in both years than in last month’s STEO. Year-over-year forecast consumption growth in 2025 is largely unchanged compared with the March STEO.

Although the revisions to historical consumption resulted in more forecast petroleum consumption, they also decreased demand growth in 2024 compared with our previous STEO. However, the sources of growth remain the same; non-OECD Asian countries—particularly China and India—drive global liquid fuels demand growth in our forecast, although we also expect significant growth in the Middle East and United States.

Global oil prices and inventories

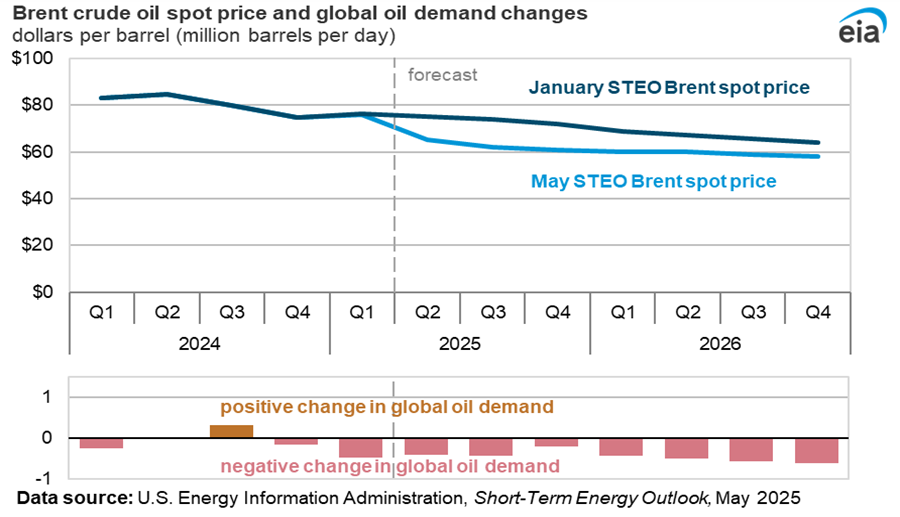

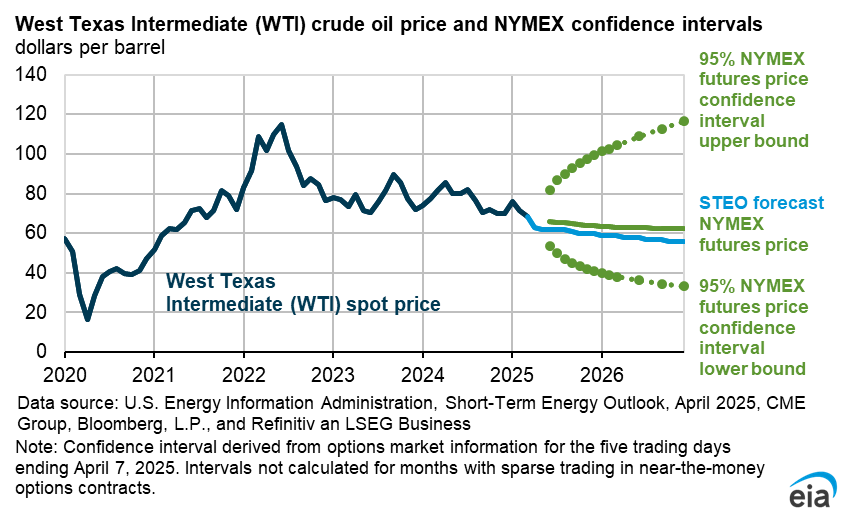

The Brent crude oil spot price averaged $85 per barrel (b) in March, a $2/b increase compared with February and the third consecutive month when the average Brent price increased. Oil prices continued to increase in March as a result of heightened geopolitical risk related to the attacks targeting commercial ships transiting the Red Sea shipping channel and general elevated tensions around the region. In addition, the recent extension of OPEC+ voluntary production cuts add to upward price pressure right at a time of the year when oil demand typically increases because of the spring and summer driving seasons in the Northern Hemisphere.

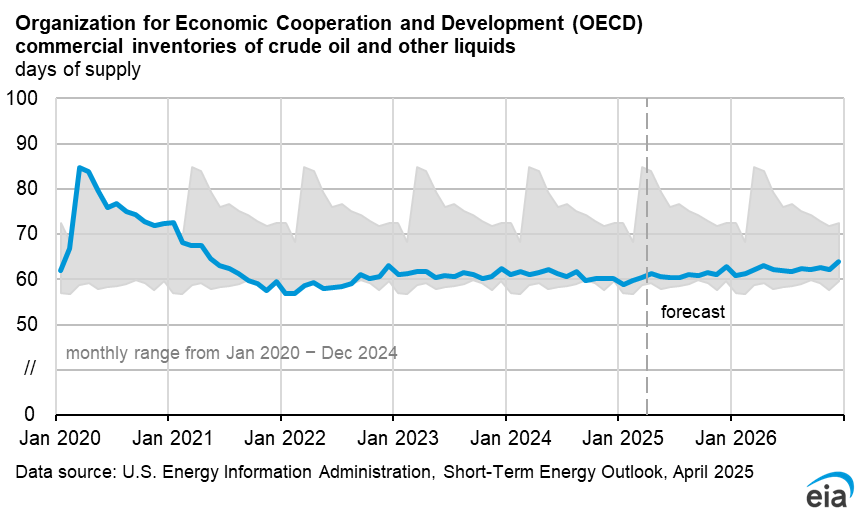

The combination of flat production and rising consumption causes our forecast of global oil inventories to fall by more than 0.9 million b/d in 2Q24, which we expect will add upward pressure to oil prices. We expect the tighter market balance to keep oil prices relatively elevated, averaging $90 in 2Q24—$2/b higher than in last month’s STEO.

We forecast oil inventories will begin increasing in 2025 because we assume OPEC+ production will increase when OPEC+ supply cuts expire. We forecast global oil inventories to increase by an average 0.4 million b/d in 2025, which we expect will put downward pressure on prices. We forecast the Brent crude oil price will decrease year-over-year from an average $90/b in 4Q24 to an average $86/b in 4Q25, with annual averages of $89/b in 2024 and $87/b in 2025.

Global oil production

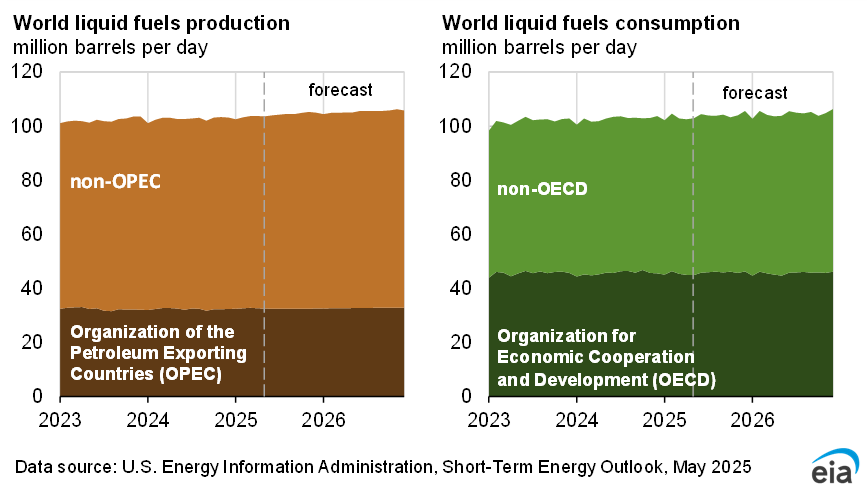

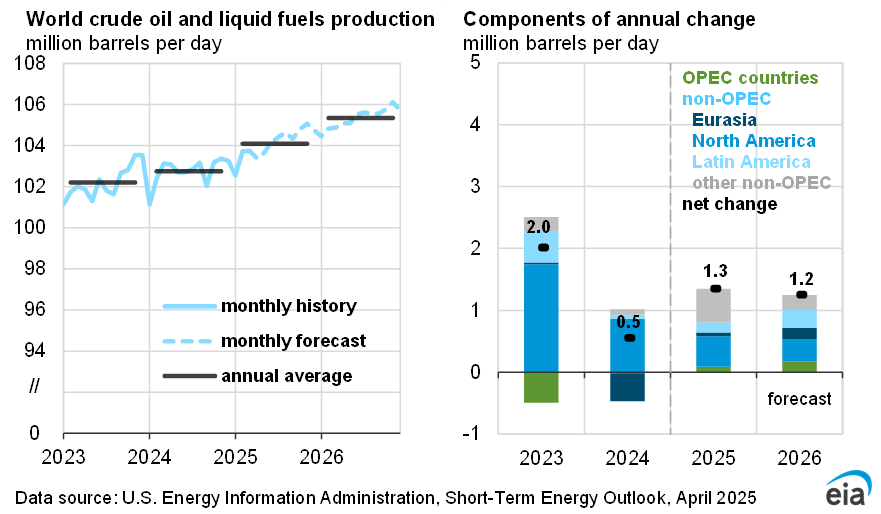

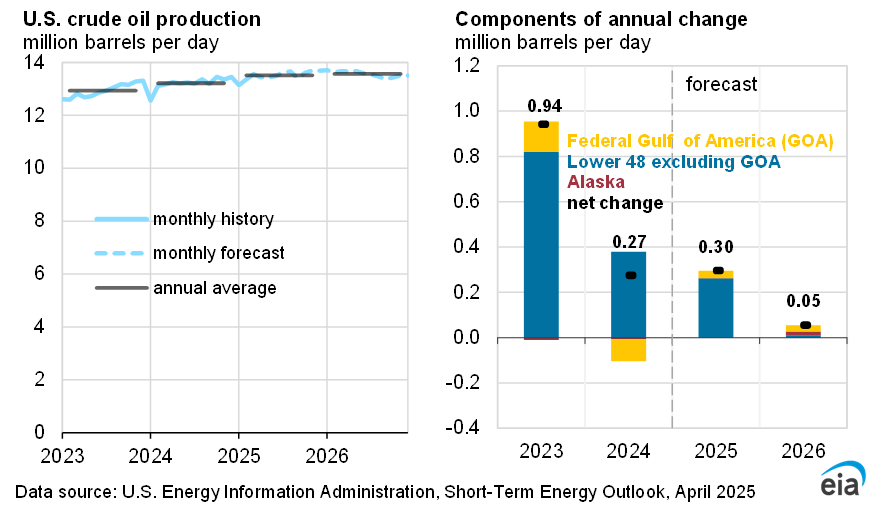

We expect global production of liquid fuels to increase by more than 0.8 million b/d in 2024, slowing from the 1.8 million b/d increase in 2023, as OPEC+ voluntary production cuts are offset by supply growth outside of OPEC+. Although forecast OPEC+ crude oil production in 2024 decreases by 0.9 million b/d compared with last year, forecast production outside of OPEC+ increases by 1.8 million b/d, led by the United States, Guyana, Brazil, and Canada. Global liquid fuels production in our forecast increases by 2.0 million b/d in 2025 as the OPEC+ production cuts expire and supply growth outside of OPEC+ continues to grow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}