Review of Emerging Resources: U.S. Shale Gas and Shale Oil Plays

Release date: July 8, 2011

Background

The use of horizontal drilling in conjunction with hydraulic fracturing has greatly expanded the ability of producers to profitably recover natural gas and oil from low-permeability geologic plays—particularly, shale plays. Application of fracturing techniques to stimulate oil and gas production began to grow rapidly in the 1950s, although experimentation dates back to the 19th century. Starting in the mid-1970s, a partnership of private operators, the U.S. Department of Energy (DOE) and predecessor agencies, and the Gas Research Institute (GRI) endeavored to develop technologies for the commercial production of natural gas from the relatively shallow Devonian (Huron) shale in the eastern United States. This partnership helped foster technologies that eventually became crucial to the production of natural gas from shale rock, including horizontal wells, multi-stage fracturing, and slick-water fracturing.1 Practical application of horizontal drilling to oil production began in the early 1980s, by which time the advent of improved downhole drilling motors and the invention of other necessary supporting equipment, materials, and technologies (particularly, downhole telemetry equipment) had brought some applications within the realm of commercial viability.2

The advent of large-scale shale gas production did not occur until Mitchell Energy and Development Corporation experimented during the 1980s and 1990s to make deep shale gas production a commercial reality in the Barnett Shale in North-Central Texas. As the success of Mitchell Energy and Development became apparent, other companies aggressively entered the play, so that by 2005, the Barnett Shale alone was producing nearly 0.5 trillion cubic feet of natural gas per year. As producers gained confidence in the ability to produce natural gas profitably in the Barnett Shale, with confirmation provided by results from the Fayetteville Shale in Arkansas, they began pursuing other shale plays, including Haynesville, Marcellus, Woodford, Eagle Ford, and others.

Although the U.S. Energy Information Administration's (EIA) National Energy Modeling System (NEMS) and energy projections began representing shale gas resource development and production in the mid-1990s, only in the past 5 years has shale gas been recognized as a "game changer" for the U.S. natural gas market. The proliferation of activity into new shale plays has increased dry shale gas production in the United States from 1.0 trillion cubic feet in 2006 to 4.8 trillion cubic feet, or 23 percent of total U.S. dry natural gas production, in 2010. Wet shale gas reserves increased to about 60.64 trillion cubic feet by year-end 2009, when they comprised about 21 percent of overall U.S. natural gas reserves, now at the highest level since 1971.3Oil production from shale plays, notably the Bakken Shale in North Dakota and Montana, has also grown rapidly in recent years.

To gain a better understanding of the potential U.S. domestic shale gas and shale oil resources, EIA commissioned INTEK, Inc. to develop an assessment of onshore Lower 48 States technically recoverable shale gas and shale oil resources. This paper briefly describes the scope, methodology, and key results of the report and discusses the key assumptions that underlie the results. The full report prepared by INTEK is provided in Attachment A. The shale gas and shale oil resource assessment contained in the INTEK report and summarized here was incorporated into the Onshore Lower 48 Oil and Gas Supply Submodule (OLOGSS) within the Oil and Gas Supply Module (OGSM) of NEMS to project oil and natural gas production for the Annual Energy Outlook 2011 (AEO2011). EIA also anticipates using the assessment to inform other analyses and projections and to provide a starting point for future work.

Scope and Results

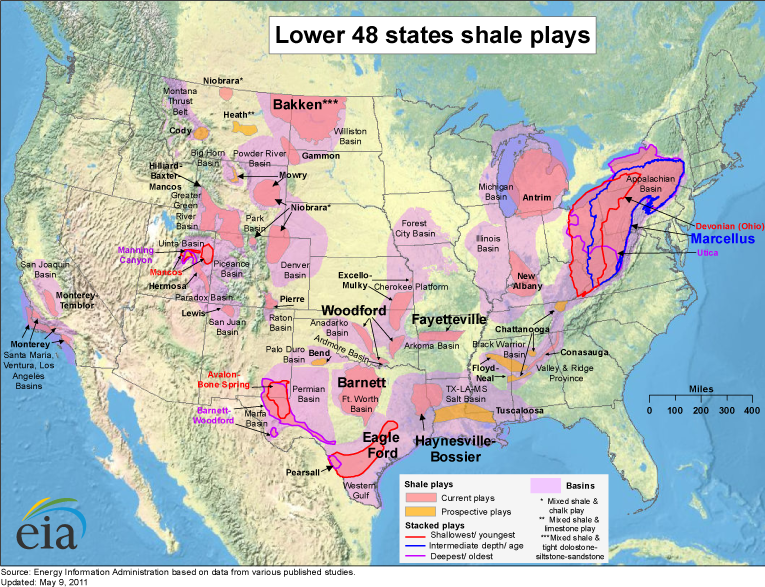

The INTEK shale resources report estimates shale gas and shale oil resources for the undeveloped portions of 20 shale plays that have been discovered (Table 1). Eight of those shale plays are subdivided into 2 or 3 areas, resulting in a total of 29 separate resource assessments. The total of 750 trillion cubic feet shown in Table 1 excludes three additional components of resources: proven reserves, inferred reserves in actively developed areas and undiscovered resources as estimated by the U.S. Geological Survey (USGS). The map in Figure 1 shows the location of the shale plays in the Lower 48 States.

Figure 1. Map of U.S. shale gas and shale oil plays (as of May 2011)

Figure 1. Map of U.S. shale gas and shale oil plays (as of May 2011)

Eighty-six percent of the total 750 trillion cubic feet of technically recoverable shale gas resources identified in Table 1 are located in the Northeast, Gulf Coast, and Southwest regions, which account for 63 percent, 13 percent, and 10 percent of the total, respectively. In the three regions, the largest shale gas plays are the Marcellus (410.3 trillion cubic feet, 55 percent of the total), Haynesville (74.7 trillion cubic feet, 10 percent of the total), and Barnett (43.4 trillion cubic feet, 6 percent of the total).

Table 1 also summarizes the INTEK shale report's assessment of technically recoverable shale oil resources, which amount to 23.9 billion barrels in the onshore Lower 48 States. The largest shale oil formation is the Monterey/Santos play in southern California, which is estimated to hold 15.4 billion barrels or 64 percent of the total shale oil resources shown in Table 1. The Monterey shale play is the primary source rock for the conventional oil reservoirs found in the Santa Maria and San Joaquin Basins in southern California.4 The next largest shale oil plays are the Bakken and Eagle Ford, which are assessed to hold approximately 3.6 billion barrels and 3.4 billion barrels of oil, respectively.

The 750 trillion cubic feet of shale gas resources in the INTEK shale report is a subset of the AEO2011 onshore Lower 48 States natural gas shale technically recoverable resource estimate of 862 trillion cubic feet. The AEO2011 includes 35 trillion cubic feet of proved reserves reported to the Securities and Exchange Commission (SEC) and the EIA5, 20 trillion cubic feet of inferred reserves not included in the INTEK shale report, and 56 trillion cubic feet of undiscovered resources estimated by the USGS.

Table 1. INTEK estimates of undeveloped technically recoverable shale gas and shale oil resources remaining in discovered shale plays as of January 1, 2009 |

|||

|---|---|---|---|

| Onshore Lower-48 Oil and Gas Supply Submodule region | Shale play | Shale gas resources (trillion cubic feet) | Shale oil resources |

| Northeast | Marcellus | 410 | -- |

| Antrim | 20 | -- | |

| Devonian Low Thermal Maturity | 14 | -- | |

| New Albany | 11 | -- | |

| Greater Sittstone | 8 | -- | |

| Big Sandy | 7 | -- | |

| Cincinnati Arch* | 1 | -- | |

| Subtotal | 472 | -- | |

| Percent of total | 63% | -- | |

| Haynesville | 75 | -- | |

| Eagle Ford | 21 | 3 | |

| Floyd-Neal & Conasauga | 4 | -- | |

| Subtotal | 100 | 3 | |

| Percent of total | 13% | 14% | |

| Mid-Continent | Fayetteville | 32 | -- |

| Woodford | 22 | -- | |

| Cana Woodford | 6 | -- | |

| Subtotal | 60 | -- | |

| Percent of total | 8% | -- | |

| Southwest | Barnett | 43 | -- |

| Barnett-Woodford | 32 | -- | |

| Avalon & Bone Springs | -- | 2 | |

| Subtotal | 76 | 2 | |

| Percent of total | 10% | 7% | |

| Rocky Mountain | Mancos | 21 | -- |

| Lewis | 12 | -- | |

| Williston-Shallow Niobraran* | 7 | -- | |

| Hilliard-Baxter-Mancos | 4 | -- | |

| Bakken | -- | 4 | |

| Subtotal | 43 | 4 | |

| Percent of total | 6% | 15% | |

| West Coast | Monterey/Santos | -- | 15 |

| Subtotal | -- | 15 | |

| Percent of total | -- | 64% | |

| Total onshore Lower-48 States | 750 | 24 | |

*Note: From previous EIA estimates and thus not assessed in the INTEK shale report. Subtotals and total may not equal sum of components due to independent rounding. |

|||

Methodology

The resource estimates shown in Table 1 were developed by INTEK from publicly available company data and commercial databases6 for wells and acreage currently in production. The estimates of technically recoverable resources shown in Table 1 are based on the area, well spacing, and average expected ultimate recovery (EUR) for each shale play or subportion of the play.7 An effective recovery factor has been applied which reflects: (a) a probability factor that takes into account the results from current shale gas activity as an indicator of how much is known or unknown about the shale play; (b) a recovery factor that takes into account prior experience in how production occurs, on average, given a range of factors (including mineralogy and geologic complexity) that affect the response of the geologic play to the application of best-practice shale gas recovery technology; and (c) resources in the play that have already been produced or added into proved reserves.

Estimates of technically recoverable shale gas resources are certain to change over time as new wells go into production and new technologies are developed. For example, the gas resource estimates in the INTEK shale report are predicated on the assumption that natural gas production rates for current wells covering only a limited portion of a play are representative of an entire play or play sub-area; however, across a single play or play sub-area there can be significant variations in depth, thickness, porosity, carbon content, pore pressure, clay content, thermal maturity, and water content. As a result, individual well production rates and recovery rates can vary by as much as a factor of 10.

There is considerable uncertainty regarding the ultimate size of technically recoverable shale gas and shale oil resources, including but are not limited to the following:

- Because most shale gas and shale oil wells are only a few years old, their long-term productivity is untested. Consequently, the long-term production profiles of shale wells and their estimated ultimate recovery of oil and natural gas are uncertain.

- In emerging shale plays, production has been confined largely to those areas known as "sweet spots" that have the highest known production rates for the play. If the production rates for the sweet spots are used to infer the productive potential of entire plays, their productive potential probably will be overstated. The INTEK shale report mitigates this problem by differentiating the productivity of a play's sweet spot from the productivity for rest of that play.8

- Many shale plays are so large (e.g., the Marcellus shale) that only portions have been extensively production tested.

- Technical advancements could lead to more productive and less costly well drilling and completion.

- Currently untested shale plays, such as thin-seam plays or untested portions of existing plays, could prove to be highly productive.

Estimating the technically recoverable oil and natural gas resource base in the United States is an evolving process. For shale gas and oil, the evolution of resource estimates is likely to continue for some time. The size of the technically recoverable oil and natural gas resource base in the United States becomes evident only as producers drill into geologic deposits with oil and gas potential and attempt to produce from them on a commercial basis. As producers find plays to be more or less bountiful than expected, resource estimates are adjusted to reflect that information. As time passes and our knowledge of the resource base and future technologies and management practices improves, estimates of the technically recoverable resource base will be refined. Consequently, the resource estimates in the current report will be modified over time as more wells are drilled and completed, technologies evolve, and the long-term performance of shale wells becomes better established.

The estimates of shale oil and shale gas resources provided here represent a reasonable estimate of the resource potential for those shale plays for which public information is currently available. The potential impacts of the current uncertainty regarding shale gas resources on projected natural gas supply, consumption, and prices are described in the AEO2011 Issues in Focus article, "Prospects for shale gas."9

Footnotes

1G.E. King, Apache Corporation, "Thirty Years of Gas Shale Fracturing: What Have We Learned?", presentation SPE

133456, SPE Annual Technical Conference and Exhibition (Florence, Italy, September 2010),

www.spe.org/atce/2010/pages/schedule/tech_program/documents/spe1334561.pdf; and U.S. Department of

Energy, "DOE's Early Investment in Shale Gas Technology Producing Results Today" (February 2, 2011),

www.netl.doe.gov/publications/press/2011/11008-DOE_Shale_Gas_Research_Producing_R.html.

2U.S. Energy Information Administration, Drilling Sideways—A Review of Horizontal Well Technology and Its Domestic Application, DOE/EIA-TR-0565 (Washington, DC, April 1993), ftp://tonto.eia.doe.gov/pub/oil_gas/natural_gas/analysis_publications/drilling_sideways_well_technology/pdf/tr0565.pdf.

3U.S. Energy Information Administration, U.S. Crude Oil, Natural Gas, and Natural Gas Liquids Reserves (Washington,

DC, November 30, 2010),

www.eia.doe.gov/oil_gas/natural_gas/data_publications/crude_oil_natural_gas_reserves/cr.html.

4American Association of Petroleum Geologists, "Monterey Shale Gets New Look," Explorer, Vol. 31, No. 11 (November 2010), http://www.aapg.org/explorer/2010/11nov/monterey1110.cfm.

5Additional information and comparisons of the SEC and EIA reserves can be found in the EIA report "U.S. Crude Oil, Natural Gas, and Natural Gas Liquids Proved Reserves, 2009" and a supplemental report "Top 100 Operators: Proved Reserves and Production, Operated vs Owned, 2009". http://www.eia.gov/oil_gas/natural_gas/data_publications/crude_oil_natural_gas_reserves/cr.html.

6HPDI, LLC production database, and Nehring Associates (NRG), Significant Oil and Gas Fields of the United States Database.

7The EURs presented in this report do not include natural gas plant liquids.

8In the INTEK report, the "sweet spot" portion of the formation is referred to as the "active area." The remaining portion of the formation that has seen little or no drilling activity is referred to as the "undeveloped area."

9U.S. Energy Information Administration, Annual Energy Outlook 2011, DOE/EIA-0383(2011) (Washington, DC, April 2011), "Prospects for shale gas," www.eia.gov/forecasts/aeo/IF_all.cfm#prospectshale.