Crude oil prices to remain relatively low through 2016 and 2017

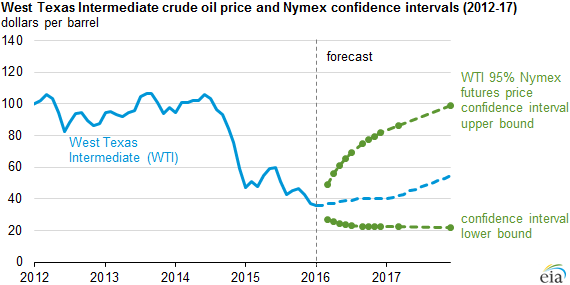

Note: Confidence interval derived from futures options prices for the five trading days ending Jan. 7, 2016. Intervals not calculated for months with sparse trading in near-the-money options contracts.

The Short-Term Energy Outlook (STEO) released on January 12, which is the first STEO to include projections for 2017, forecasts Brent crude oil prices will average $40 per barrel (b) in 2016 and $50/b in 2017. West Texas Intermediate (WTI) crude oil prices are expected to be $2/b lower than Brent in 2016 and $3/b lower than Brent in 2017.

EIA recognizes that there is still high uncertainty in the crude oil price outlook. For example, EIA's forecast for the average WTI price in April 2016 is $37/b, while the market expects WTI prices to range from $25/b to $56/b (at the 95% confidence interval) based on the recent prices of futures and options contracts for April 2016 delivery.

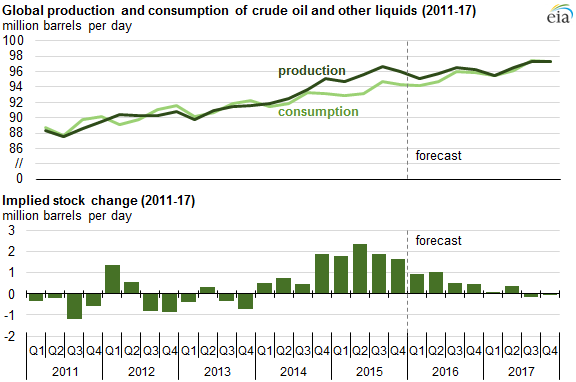

Crude oil prices are expected to remain low as supply continues to outpace demand in 2016 and more crude oil is placed into storage. EIA estimates that global oil inventories increased by 1.9 million b/d in 2015, marking the second consecutive year of inventory builds. Inventories are forecast to rise by an additional 0.7 million b/d in 2016, before the global oil market becomes relatively balanced in 2017. The first forecasted draw on global oil inventories is expected in the third quarter of 2017, marking the end of 14 consecutive quarters of inventory builds.

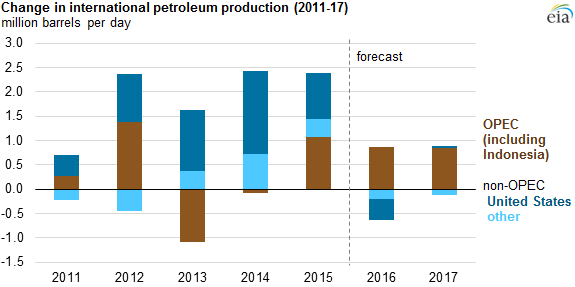

Since 2012, the United States has been the source of much of the global increase in production of petroleum and other liquids. In 2016 and 2017, however, members of the Organization of the Petroleum Exporting Countries (OPEC) are expected to account for most of production growth. EIA expects non-OPEC production to decline by 0.6 million b/d in 2016, which would be the first decline in non-OPEC production since 2008. About two-thirds of this forecasted decline in 2016 comes from the United States.

Note: Production from Indonesia, which recently regained OPEC membership, is included in OPEC totals for both history and forecasts.

Changes in non-OPEC production are driven by changes in U.S. tight oil production, which is characterized by high decline rates and relatively short investment horizons that make it among the most price-sensitive production globally. Forecast total U.S. liquid fuels production declines by 0.4 million b/d in 2016 and remains relatively flat in 2017, as low oil prices contribute to drilling rig counts falling below levels required to sustain current production rates.

OPEC crude oil production is forecast to increase by 0.5 million b/d in 2016, with Iran accounting for most of that increase. Iran is expected to increase its production once international sanctions targeting its oil sector are suspended. Although uncertainty remains as to the timing of sanctions relief, EIA assumes this occurs in the first quarter of 2016. EIA's timing reflects Iran's progress in meeting key obligations required under the Joint Comprehensive Plan of Action, which has been faster than previously anticipated.

EIA expects global consumption of petroleum and other liquid fuels to grow by 1.4 million b/d in both 2016 and 2017. Forecast real gross domestic product (GDP) for the world, weighted by oil consumption, which increased by an estimated 2.4% in 2015, rises by 2.7% in 2016 and by 3.2% in 2017.

Principal contributor: Hannah Breul