Request Summary

This report responds to a request to the U.S. Energy Information Administration (EIA) from Senators Kerry, Graham, and Lieberman for an analysis of the American Power Act of 2010 (APA).1 The APA, as released by Senators Kerry and Lieberman on May 12, 2010, regulates emissions of greenhouse gases through market-based mechanisms, efficiency programs, and other economic incentives.

APA Title I consists of incentives designed to accelerate the development and deployment of specified energy technologies. These include tax credits, loan guarantees, streamlined licensing of new facilities, appropriation of research and development funding, technology-specific allocation of emissions allowances, and other incentives. Some key provisions are:

- Nuclear Power – Subtitle A expands the loan guarantee program from the $18.5 billion authorized in the Energy Policy Act of 2005 to $54 billion; allows for 5-year accelerated depreciation on new nuclear power plants; makes these plants eligible for the Investment Tax Credit (ITC); and expands eligibility for the production tax credit. It also requires the Nuclear Regulatory Commission (NRC) to investigate ways of improving the process of licensing of new plants, and authorizes additional funding for advanced nuclear power research.

- Offshore Oil and Gas – Subtitle B allows for the revenue earned through offshore drilling in areas that as of January 1, 2000, had no oil or natural gas production and are not a Gulf producing State to be shared with the adjacent coastal State. It also allows for States to prohibit drilling within 75 miles of their coastline.

- Carbon Capture and Storage (CCS) – Subtitle C establishes the Carbon Capture and Sequestration Program Partnership Council, which is responsible for overseeing the commercialization of CCS throughout the United States. It authorizes the collection of approximately $20 billion over a 10-year period to be funded through a surcharge on electricity that is generated using fossil fuels and sold to consumers. Subtitle C also includes a provision allocating bonus allowances to owners of electric power and industrial facilities that have installed carbon capture systems, and mandates that all new coal-fired plants initially permitted after 2008 meet specific performance standards limiting carbon dioxide (CO2) emissions.

- Renewable Energy and Energy Efficiency – Subtitle D authorizes funding and low-interest loans for State and rural utility district projects on energy efficiency and renewable energy.

- Clean Transportation – Subtitle E establishes a pilot program for electric vehicles, directs the Department of Transportation and metropolitan planning organizations to identify potential greenhouse gas (GHG) savings through transportation planning, and directs additional allowances to “Clean Energy Technology Development.”

Title II of the APA, the primary focus of this analysis, creates a cap-and-trade program for GHG emissions. It explicitly covers seven gases: CO2, methane (CH4), nitrous oxide (NO2), sulfur hexafluoride (SF6), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and nitrogen trifluoride (NF3). The program establishes a cap on the covered GHG emissions that declines steadily from 2013 through 2050. The policy aims to reduce emissions from their 2005 level by 17 percent in 2020, 42 percent in 2030, and 83 percent in 2050. Each year, regulated entities must hold allowances or offset credits that cover their past year’s direct emissions and attributable emissions. The method through which allowances are distributed changes over the life of the policy, from one of mostly free allocation to emitters and other entities to an auction-based approach. Emissions associated with refined fuels are covered by the allowance requirement, but refiners purchase the allowances for these emissions from the Environmental Protection Agency and the allowance fee is linked to the allowance fee that evolves under the cap-and-trade program.

Allowances can be banked, meaning that unused allowances in a given year may be used for compliance in the future. A limited amount of allowances can also be borrowed from future years. The APA also includes a cost containment reserve (CCR), which allows covered entities to purchase allowances at a fixed price that rises from $25 (in constant 2008 dollars) to approximately $76 in 2035.2 The CCR acts as an allowance price ceiling as long as sufficient allowances are available in the reserve and covered entities do not individually exceed a 15-percent limit on the use of CCR allowances for compliance.

In addition to allowances, entities may purchase offset credits as part of their compliance obligation. Offset credits include registered reductions and avoided emissions of uncovered GHGs both domestically and internationally. Up to 2 billion metric tons CO2 equivalent (BMT) of offsets may be used each year, with up to 1.5 BMT coming from domestic offsets and 0.5 BMT coming from international offsets. If sufficient domestic offsets are not available, the limit on international offsets may be increased to 1 BMT.

While the emissions caps in the APA cap-and-trade program decline through the year 2050, the modeling horizon in this report runs only through 2035, the current projection horizon of the EIA National Energy Modeling System (NEMS). As in EIA analyses of earlier cap-and-trade proposals, the need to pursue higher-cost emissions reductions beyond 2035, driven by tighter caps and continued economic and population growth, is reflected by assuming that a positive bank of allowances will be held at the end of 2035.

APA Titles III and IV contain provisions designed to limit consumer impacts and address potential impacts on manufacturing jobs. Title III requires that revenues generated from the sale of allowances be allocated to regulated electricity and natural gas local distribution companies to offset cost impacts on consumers and promote efficiency, as well as to States for credits on home heating oil bills. It also creates a universal trust fund that directs allowance auction revenue to be applied toward household rebates. Title IV allocates allowances to energy-intensive industrial sectors. It also includes incentives for entities that manufacture and sell natural gas vehicles domestically. Titles V and VI define the role of the United States in international climate change mitigation programs, as well as addressing domestic climate change adaptation strategies.

This report considers the energy-related provisions in APA that can be analyzed using NEMS. The starting point for the analysis is a Reference case similar to the Annual Energy Outlook 2010 (AEO2010) Reference case issued in December 2009. The slight differences in the Reference case for this report reflect modeling changes required to analyze the legislation, such as emissions coverage definitions and minor structural changes to represent the bill’s incentives and programs.

This analysis represents the following key provisions of APA in its policy cases:

- The cap and trade program for GHGs, except for hydro-fluorocarbons (HFCs). It includes the provisions allowing for allowance trading, banking and borrowing, the cost containment reserve, and accounts for the potential availability of domestic and international offsets. The policy cases also represent the allocation of emissions allowances to electricity and natural gas local distribution companies and States for home heating oil users, as well as other consumers and energy intensive industries specified in the bill.

- Financial incentives designed to spur the development of new nuclear power plants. These include allowing accelerated depreciation schedules, investment and production tax credits, and expansion of the nuclear loan guarantee program.

- Allocation of bonus allowances for eligible CCS projects as specified in the bill. The surcharge on electricity designed to fund the development and deployment of carbon capture, storage, and conversion technologies is also included.

- Use of allowance revenue from allocations to State energy efficiency and renewable energy programs to accelerate efficiency improvements of residential and commercial buildings, as well as to foster adoption of distributed renewables in the form of rebates for solar water heaters, solar photovoltaic and distributed wind for public buildings.

- Tax credits for qualifying natural gas fueled vehicles.

While this analysis is as comprehensive as possible given time constraints, it does not address all the provisions of the APA. Provisions that are not represented include any resulting changes in the Nuclear Regulatory Commission (NRC) licensing process, the offshore oil and gas incentives, increased investment in energy research and development, a separate cap-and-trade system for HFC emissions, any of the transportation planning or funding sections, vehicle GHG standards beyond those in current law, and the rural energy savings program.

Like other EIA analyses of energy and environmental policy proposals, this report focuses on the impacts of those proposals on energy choices made by consumers and producers in all sectors and the implications of those decisions for the economy. This focus is consistent with EIA’s statutory mission and expertise. The study does not account for the health or environmental benefits associated with curtailing GHG emissions.

Analysis Cases

EIA prepared a range of analysis cases for this report. Detailed results tables can be found at http://www.eia.gov/oiaf/service_rpts.htm. The six analysis cases discussed, while not exhaustive, focus on several key areas of uncertainty that impact the analysis results. All of these cases are compared to the Reference case, except for the High Natural Gas Resource case which is compared with an alternative reference case using the same natural gas resource assumptions.

The role of offsets is a large area of uncertainty in any analysis of the APA. The 2 BMT annual limit on total offsets is equivalent to one-third of total energy-related GHG emissions in 2008, and it represents nearly four times the growth in energy-related emissions through 2035 in the Reference case. Furthermore, additional offsets may be used in connection with replenishing allowances sold from the cost containment reserve.

While the ceiling on use of direct offsets clear, their actual use is an open question. Beyond the usual uncertainties related to the technical, economic, and market supply of offsets, the future use of offsets for APA compliance also depends on regulatory decisions that are yet to be made. Their usage also depends on the timing and scope of negotiations on international agreements or arrangements between the United States and countries where offset opportunities may exist, and on emissions reduction commitments made by other countries. Also, limits on offset use in the APA apply individually to each covered entity, so that offset “capacity” that goes unused by one or more covered entities cannot be used by other covered entities. For some major entities covered by the cap-and-trade program, decisions regarding the use of offsets could potentially be affected by regulation at the State level. Given the many technical factors and implementation decisions involved, it is not surprising that analysts’ estimates of international offset use span a very wide range.

For the period prior to 2035, another key issue is the availability and cost of low- and no-carbon baseload electricity technologies, such as nuclear power and fossil (coal and natural gas) with CCS, which can potentially displace a large amount of conventional coal-fired generation. However, technology availability over an extended horizon is a two-sided issue. Research and development breakthroughs over the next two decades could expand the set of reasonably priced and scalable low- and no-carbon energy technologies across all energy uses, including transportation, with opportunities for widespread deployment beyond 2035. The achievement of significant near-term progress toward such an outcome could in turn significantly reduce the size of the bank of allowances that covered entities and other market participants would want to carry forward to meet compliance requirements beyond 2035.

There is also uncertainty about the role that increased use of natural gas might play in reducing U.S. GHG emissions. While recent years have seen strong growth in the development of shale gas resources, there is significant uncertainty about the extent of those resources and the economics of developing them.

With these key uncertainties in mind, the six analysis cases discussed in this report are as follows:

- The APA Basic case represents an environment where key low-emissions technologies, including nuclear, fossil with CCS, and various renewables, are developed and deployed on a large scale in a timeframe consistent with the emissions reduction requirements of the APA without encountering any major obstacles. It also assumes that the use of offsets, both domestic and international, is not instantaneous but is also not severely constrained by cost, regulation, or the pace of negotiations with key countries. In anticipation of increasingly stringent caps and rising allowance prices after 2035, covered entities and investors are assumed to amass an aggregate allowance bank of approximately 10 BMT by 2035 through a combination of offset usage and emission reductions that exceed the level required under the emission caps.

- The APA Zero Bank case is similar to the Basic case except that no banked allowances are held in 2035, reflecting the assumed availability post-2035 of a broad array of reasonably priced low- and no-carbon technologies that can provide an alternative path to compliance with the tightening emissions caps.

- The APA High Natural Gas Resource case is similar to the Basic case, except that it assumes a larger resource for shale gas based on the High Shale Gas Resource sensitivity casein the AEO2010. The unexploited portion of each shale gas play is assumed to be able to support twice as many new wells as in the Reference case, increasing the unproved shale gas resource base from 347 trillion cubic feet in the Reference case to 652 trillion cubic feet. This case is not directly comparable to the Reference case shown in the report because of the alternative natural gas resource base assumed. Instead, an alternative High Natural Gas Resource Reference case that incorporates the same natural gas resource assumptions as in this APA case is used for comparison and is available on the EIA web site along with the detailed results from all the cases discussed.

- The APA High Cost case is similar to the Basic case, except that the overnight capital costs of nuclear, fossil with CCS (including CCS retrofit), and dedicated biomass generating technologies are assumed to be 50 percent higher than in the Reference case. Covered entities are also assumed to amass an aggregate 12 BMT allowance bank by 2035. As with the High Natural Gas Resource case, this case should not be compared to the Reference case because of the alternative assumptions about generating technology costs. However, because the affected technologies play a fairly small role in the Reference case, comparisons should only be slightly affected.

- The APA No International case is similar to the Basic case, but it represents an extreme where the use of international offsets is eliminated by cost, regulation, and/or slow progress in reaching international agreements or arrangements covering offsets in key countries and sectors. Covered entities are assumed to amass an aggregate 12 BMT allowance bank by 2035 in this case.

- The APA Limited/No International case combines the treatment of offsets in the No International case with the assumption that the deployment of key technologies, including nuclear, fossil with CCS, and dedicated biomass, is limited to the Reference case levels through 2035. There is great uncertainty about how fast these technologies, the industries that support them, and the regulatory infrastructure that licenses/permits them might be able to grow and, for fossil with CCS, when the technology will be fully commercialized. Covered entities are assumed to amass an aggregate 15 BMT allowance bank balance by 2035 in this case. The extreme limits on many of the key emissions reduction options in this case make compliance extremely challenging and lead to rapid shifts in the remaining alternatives that may be difficult to achieve. This should be kept in mind when reviewing the results in this case.

EIA cannot attach probabilities to the individual policy cases. However, both theory and common sense suggest that cases reflecting an unbroken chain of either failures or successes in a series of independent factors are inherently less likely than cases that do not assume that everything goes either wrong or right. In this respect, the Limited/No International and Zero Bank cases might be viewed as more pessimistic and optimistic scenarios, respectively, which bracket a set of more likely cases.

Findings3

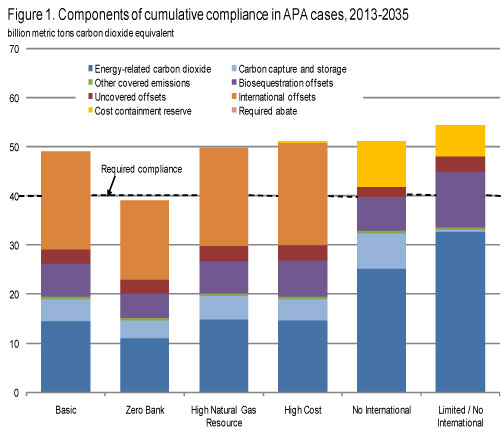

Offsets account for the majority of the compliance through 2035, except for cases where no international allowances are assumed to be available. In the Basic case, offsets, including those purchased from the cost containment reserve that is to be refilled with offsets, account for 57 percent of overall compliance (Figure 1 and Table 1). Reductions in U.S. emissions of energy-related CO2 account for more than half of the cumulative compliance through 2035 only in the cases where no international offsets are assumed to be available.

Allowances purchased from the cost containment reserve are most important if the supply of offsets is limited. In these cases, allowances purchased from the cost containment reserve account for between 12 percent and 18 percent (6 to 9 BMT) of overall compliance through 2035. The reliance on the cost containment reserve is smaller in the Limited/No International case than in the No International case, primarily because funds available for replenishing the reserve can buy fewer domestic offsets given their higher price in this case. In other words, the amount of offsets that can be purchased for a given amount of cost containment reserve funds is lower in the Limited/No International case, and the cost containment reserve is depleted much faster.

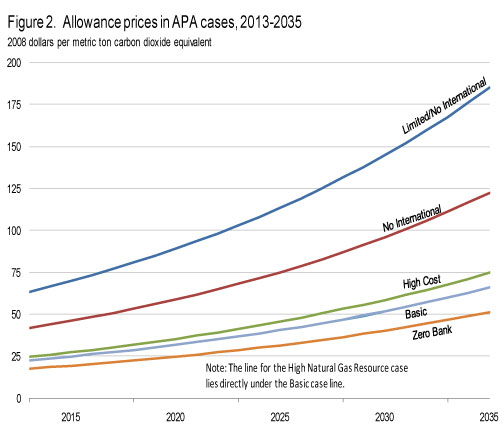

GHG allowance prices are sensitive to the cost and availability of emissions offsets and low-and no-carbon electricity generation technologies. Allowance prices in the Basic case remain below the cost containment reserve ceiling price, reaching $32 per metric ton in 2020 and $66 per metric ton in 2035 (Figure 2). The same is true in the High Natural Gas Resource case, while in the High Cost case allowance prices are contained to the cost containment reserve ceiling price. In the Zero Bank case, allowance prices are well below the cost containment reserve ceiling price, reaching $25 per metric ton in 2020 and $51 per metric ton in 2035. In this case covered entities choose not to build a bank of allowances for post-2035 use because of the possibility that technological breakthroughs will make future emissions reductions cheaper. The only cases where the cost containment reserve does not set a ceiling on allowance prices are those where the reserve is exhausted and it is assumed that international offsets are unavailable to refill it. As a result, the allowance prices in the No International and Limited/No International cases range from $59 to $89 per metric ton in 2020 and from $122 to $185 per metric ton in 2035 (both in 2008 dollars).

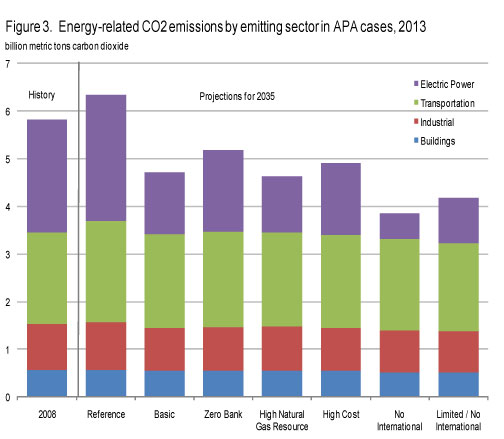

The vast majority of reductions in energy-related emissions occur in the electric power sector. Across the APA cases, the electricity sector accounts for between 78 percent and 86 percent of the total reduction in U.S. energy-related CO2 emissions relative to the appropriate Reference case in 2035 (Figure 3). Reductions in electricity-sector emissions are primarily achieved by reducing the role of conventional coal-fired generation, which in 2008 provided 48 percent of total U.S. generation, and increasing the use of no- or low-carbon generation technologies that either exist today (e.g., renewables and nuclear) or are under development (fossil with CCS). In addition, a portion of the electricity-related CO2 emissions reductions results from reduced electricity demand stimulated by the energy efficiency provisions of APA as well as consumer responses to higher electricity prices. Electricity consumption is 3 to 7 percent below the Reference case level in 2035 in five of the six main cases. In the Limited/No International case, electricity consumption is 13 percent below the Reference case level in 2035.

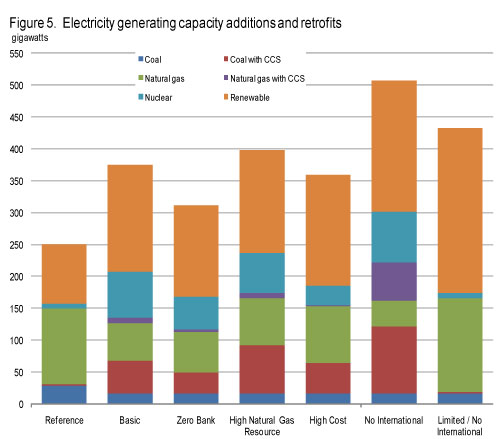

If new nuclear, renewable, and fossil plants with CCS are not developed and deployed in a timeframe consistent with emissions reduction requirements under APA, covered entities respond by increasing their purchases from the cost containment reserve, increasing their use of offsets, if available, and turning to increased natural gas use to replace reductions in conventional coal-fired generation. The share of generation from coal plants falls from 48 percent in 2008 to between 7 and 32 percent in 2035 in the APA cases (Figures 4 and 5). Natural gas generation rises above Reference case levels until 2027 in all cases and only falls below those levels in the later years in some cases as lower emitting technologies are brought on line in larger quantities. However, greater use of natural gas could be especially important if the deployment of lower emitting technologies or the supply of offsets is more costly, limited, or delayed. In the Limited/No International case the share of total generation coming from natural gas plants reaches 39 percent in 2035, nearly double the share in 2008.

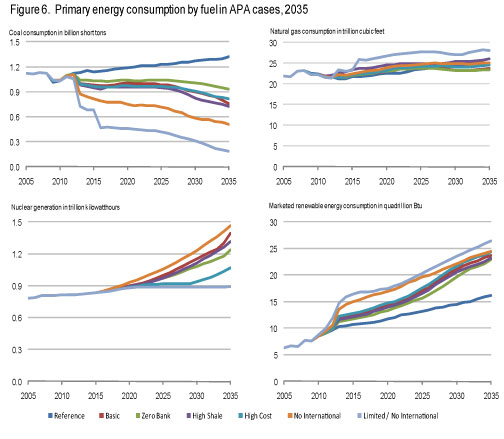

Emissions reductions from changes in direct fossil fuel use in residential and commercial buildings and in the industrial and transportation sectors are small relative to those in the electric power sector. The overall changes in the use of fossil fuels other than coal are relatively modest (Figure 6). Taken together, changes in fossil fuel use in the buildings, industrial, and transportation sectors account for between 14 percent and 22 percent of the total reduction in energy-related CO2 emissions relative to the Reference case in 2035. This reflects both smaller percentage changes in delivered fossil fuel prices than experienced by the electricity generation sector and also the low availability of alternatives in many applications. For example, motor gasoline prices in the Basic case are 26 cents per gallon (8 percent) higher than in the Reference case in 2020 and 38 cents per gallon (10 percent) higher in 2035 (in 2008 dollars).

In an additional case that incorporated the building code changes called for in the American Clean Energy Leadership Act of 2009 (S. 1462), further energy consumption reductions occurred. However, since building stock turnover occurs at a relatively slow pace, the impacts are modest, reducing building energy consumption in 2035 by 2 percent below the level in the Basic case.

APA reduces liquid fuel consumption, increases domestic oil production, increases biofuel use, and reduces oil imports. The higher fuel prices resulting from APA lead consumers to reduce their consumption, while suppliers increase their production of biofuels. Across the APA cases, total liquid fuel consumption in 2035 is between 0.2 and 1.3 million barrels per day (bpd) below the Reference case level. At the same time, consumption of ethanol and other biofuels (all of which are treated as having zero net GHG emissions) is between 21.7 and 25.3 billion gallons above the Reference case level.

Moreover, the combination of allowance costs on GHG emissions and incentives designed to stimulate the deployment of CCS technology causes power companies and other large industrial companies to install equipment to capture CO2 that would otherwise be released into the atmosphere. In cases that allow additional CCS, this captured CO2 then becomes available for use in enhanced oil recovery operations, and as a result domestic oil production increases by roughly 0.2 to 0.4 million bpd in the APA cases in 2020 and 0.8 to1.0 million bpd in 2035.

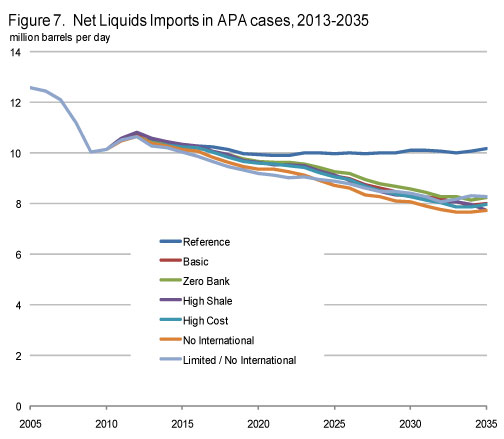

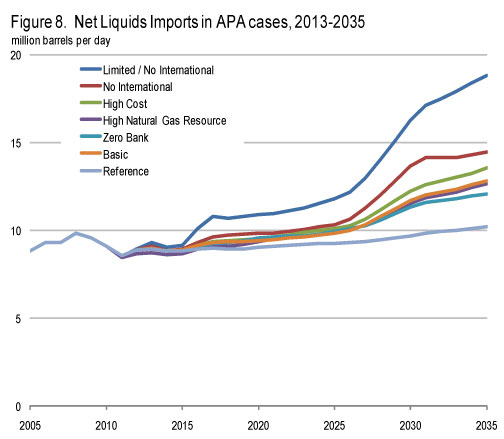

The combination of lower liquid fuel use, increased domestic oil production, and increased use of biofuels leads to a reduction in crude oil imports of 0.3 to 0.8 million bpd in 2020 and 1.9 to 2.4 million bpd in 2035 in the APA cases that do not limit the deployment of CCS (Figure 7). While world oil prices fall in this study because of the decrease in U.S. oil use, the actual change could be larger if the policies adopted in other countries led to reductions in their oil use. If this were to occur, the gross domestic product (GDP) impacts of the policy as well as the reduction in U.S. imports shown here could be dampened.

APA increases energy prices, but the effects on electricity and natural gas bills of consumers are substantially dampened through 2025 by the allocation of free allowances to regulated electricity and natural gas distribution companies. Except for the Limited/No International case, electricity prices in five of the six APA cases range from 9.4 to 9.8 cents per kilowatthour in 2020, only 4 to 9 percent above the Reference case level (Figure 8).4 Average impacts on electricity prices in 2035 are substantially greater, reflecting both higher allowance prices and the phaseout of the free allocation of allowances to distributors between 2025 and 2030. By 2035, electricity prices in the Basic case are 12.8 cents per kilowatthour, 26 percent above the Reference case level, with a wider band of 12.1 cents to 14.5 cents (18 to 42 percent above the Reference case level) across five of the six cases.

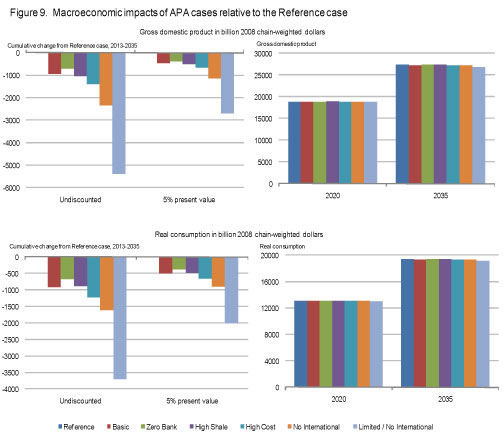

The APA increases the cost of using energy, which reduces real economic output, reduces purchasing power, and lowers aggregate demand for goods and services. The result is that real GDP generally falls relative to the Reference case. In the Reference case, GDP rises 92 percent, from $14.3 trillion in 2008 to $27.4 trillion in 2035. Total present value5 GDP losses over the 2013-2035 time period are $452 billion (-0.2 percent) in the Basic case, with a range from $381 billion (-0.1 percent) to $1.1 trillion (-0.4 percent) in five of the six cases. The present value GDP losses over the same time period are larger in the Limited/No International case, reaching $2.7 trillion (-1.0 percent) (Table 2 and Figure 9).

Similarly, the cumulative discounted losses for personal consumption are $500 billion (-0.3 percent) in the Basic case and range from $386 billion (-0.2 percent) to $901 billion (-0.5 percent) in five of the six cases. As with GDP, consumption losses over the same time period are larger in the Limited/No International case, reaching $2.0 trillion (-1.0 percent). In all cases, real consumption starts to return to Reference case levels over the last few years of the projection, as the amount of allowance revenue devoted to the universal refund sharply increases in 2030 and beyond. In 2026, the starting year of the universal refund, its share of allowance revenue is 6 percent, and by 2035 it reaches nearly 60 percent.

The allocation of allowance revenue to eligible taxpayers dampens the direct economic impact of the cap-and-trade program on consumers. Two major uses of allowance revenues reduce the possible impacts of the cap-and-trade program on consumers, leading to higher impacts on production compared to consumption losses. Roughly 12 percent of the allowance revenues starting in 2013 and continuing throughout the projection horizon is aimed at low-income taxpayers. In addition, the universal refund, defined as the amount of revenue remaining after deficit reduction and the defined uses of revenue have been allocated, increases late in the projections as the bill’s defined uses expire starting in 2026. By 2035, the universal refund accounts for over half of the allowance revenue, totaling $196 billion nominal in the Basic case.

Consumption impacts can also be expressed on a per household basis. The annualized value of household consumption losses from 2013 to 2035 is $206 (2008 dollars) in the Basic case, with a range of $153 to $336 across five of the six APA cases. In the Limited/No International case it is $814 per household.6

Employment impacts are fairly small in most of the APA cases. Overall employment stays within 0.1 to 0.2 percent of the Reference case level in most years. Only in the No International and Limited/No International cases, which have much higher allowance prices and GDP impacts than the other cases, does employment fall measurably below the Reference case level in the later years of the projections.

Additional Insights

The role of baseline assumptions. The choice of a baseline is one of the most influential assumptions for any analysis of global climate change legislation. This analysis uses the AEO2010 Reference case as a starting point or, in the case of the High Natural Gas Resource case, an alternative reference case with the same resource assumptions. EIA recognizes that projections of energy markets over a 25-year period are highly uncertain and subject to many events that cannot be foreseen, such as supply disruptions, policy changes, and technological breakthroughs. In addition to these phenomena, long-term trends in technology development, demographics, economic growth, and energy resources may evolve along a different path than shown in the projections. Generally, differences between cases, which are the focus of our report, are likely to be more robust than the specific projections for any one case. The published AEO2010,which includes numerous cases reflecting a variety of alternative futures for the economy, energy markets, and technology, is a resource that can be used to examine the implications of alternative baselines.

Free allowance allocation to electricity and natural gas distributors. The analysis shows that the free allocation of allowances to electricity and natural gas distributors significantly dampens impacts on consumer electricity and natural gas prices prior to 2025, after which it starts to be phased out. While this result may serve goals related to regional and overall fairness of the program, the efficiency of the cap-and-trade program is reduced to the extent that the price signal that would encourage cost-effective changes by consumers in their use of electricity and natural gas is delayed.

Electricity capacity siting challenges. Besides changing the mix of new electricity generation capacity, compliance with the APA would also significantly increase the total amount of new electric capacity that must be added between now and 2035. This is due to the retirement of many existing coal-fired power plants that would otherwise continue to operate beyond 2035. Obstacles to siting major electricity generation projects and/or the transmission facilities needed to support the greatly expanded use of renewable energy sources are not explicitly considered in this report. However, the additional capacity requirements in all the APA cases suggest the need for review of siting processes so that they would be able to support a large-scale transformation of the U.S. electricity infrastructure by 2035.

Challenges beyond 2035. As previously noted, the modeling horizon for this analysis ends in 2035. Unless substantial progress is made in identifying low- and no-carbon technologies outside of electricity generation, the APA emissions targets for the 2035-2050 period are likely to be very challenging, as opportunities for further reductions in power sector emissions are exhausted and reductions in other sectors are thought to be more expensive.

Notes

1 The request letter from Senators Kerry, Graham, and Lieberman is provided in Appendix A.

2 APA calls for the cost containment reserve price to start at $25 in 2013 and rise at 5 percent above the increase in the all urban consumer price index. In chain-weighted GDP real dollars, this equates to an annual increase of approximately 5.2 percent, such that the 2035 cost containment reserve price in 2035 will be approximately $76.

3 Detailed spreadsheets for all the cases discussed in this report are available at: http://www.eia.gov/oiaf/service_rpts.htm. Readers are also referred to the report, Energy Market and Economic Impacts of H.R. 2454, the American Clean Energy and Security Act of 2009, for further discussion of the methodology used in EIA greenhouse gas analysis reports.

4 The average electricity price in the Limited/No International case is 11.0 cents per kilowatthour in 2020 and 18.8 cents per kilowatthour in 2035.

5 Present value figures are discounted at a rate of 5 percent.

6 The values are calculated as per household annuity payments over the 2013-2035 period. |