Oil and Natural Gas Resources and Technology

Release Date: 3/26/18

Future growth in U.S. crude oil and natural gas production is projected to be driven by the development of tight oil [1] and shale gas [2] resources. However, a great deal of uncertainty surrounds this result. In particular, future domestic tight oil and shale gas production depends on the quality of the resources, the evolution of technological and operational improvements to increase productivity per well and to reduce costs, and the market prices determined in a diverse market of producers and consumers, all of which are highly uncertain. This article provides background on the analysis of the estimated ultimate recovery per well (EUR) [3], a key assumption underlying the projections, and it provides a detailed discussion of the sensitivity of results across Annual Energy Outlook 2018 (AEO2018) cases.

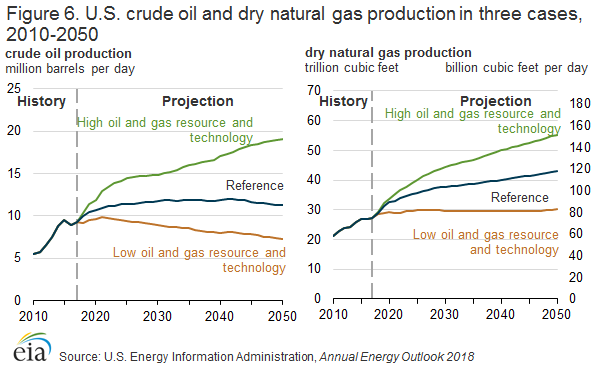

The outlook for domestic crude oil and natural gas production is highly sensitive to resource and technology assumptions. In the AEO2018 Reference case, domestic crude oil production increases over the next five years and then generally flattens after 2022, staying about 11 million to 12 million barrels per day (b/d) through 2050. Similarly, domestic dry natural gas production increases rapidly (more than 5% annually) through 2021 and then slows to an annual average growth rate of 1% through 2050, reaching 43.0 trillion cubic feet (Tcf) per year in 2050 in the Reference case. In the High Oil and Gas Resource and Technology case, domestic crude oil and dry natural gas production increases through 2050, reaching 19.1 million b/d and 55.3 Tcf/year, respectively, in 2050. In the Low Oil and Gas Resource and Technology case, domestic crude oil production decreases for most of the projection period, and dry natural gas production stays near 30 Tcf/year from 2018 through 2050.

Background

Production profiles from currently producing wells provide the basis for calculating existing EURs and provide insight about the potential productivity of new wells drilled in the same play. In examining the trend of EURs in a play, the life cycle of development provides a good framework for analyzing the results. Geology, technology, and economic conditions specific to the area being developed also need to be considered. Using the example of the Eagle Ford, the following discussion illustrates the common trends affecting the EUR of a horizontal oil well in a particular play. [4]

The development life cycle of a tight oil or shale gas play consists of four phases: (1) exploration and appraisal, (2) early development, (3) stabilization of production, and (4) maximization of recovery. Even though the play may have many producers with varying lease positions and specific operational objectives, the general pattern of the life cycle of a play follows this pattern. The length of each phase is largely determined by the quality and size of the resource, the availability of infrastructure and experienced personnel, and current market conditions during development.

Phase I—exploration and appraisal.

The primary objective during this phase is to identify formations with potential commercial development by evaluating geologic characteristics (i.e., depth, porosity, thickness, total organic carbon, fluid saturations, etc.). Seismic and geophysical data are interpreted to assess potential crude oil and natural gas in the ground. Exploration and appraisal wells are also drilled to determine the size, quality and geographical extent of the play.

Phase II—early development.

During this phase, more wells are drilled over a broader area of the play, and areas with the greatest potential (sweet spots [5]) are identified. In addition, this phase may see high levels of technological and operational innovations as producers determine how to more efficiently extract the hydrocarbons at the lowest per-unit costs. The average EUR for the formation usually increases the fastest during this phase.

Phase III—stabilization of production.

During this phase, producers optimize lateral lengths, [6] well spacing, and completion design to account for their improved understanding of the resource to focus on reducing per-unit production costs. This optimization often results in a well production profile that has higher initial production rates, higher initial decline rates, and longer production tails than previous wells drilled in the same area but not necessarily an increase in the overall average EUR.

Phase IV—maximization of recovery.

During this phase, drilling continues in core areas (reducing well spacing and increased well interference) and expands to less productive areas. As a result, the average EUR for the formation tends to decrease.

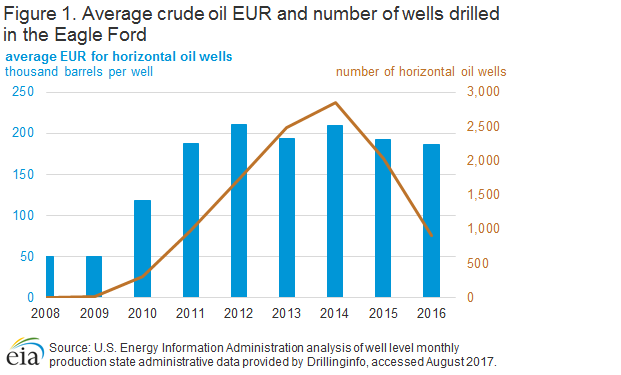

Development of a play usually begins slowly as producers secure leases and start drilling to determine if oil can be produced from that play given current technology. If the areas of exploration are determined to be economically viable, drilling will speed up quickly. For example, horizontal oil drilling in the Eagle Ford increased rapidly in 2010 when the West Texas Intermediate (WTI) spot oil price averaged slightly less than $90 per barrel (in real 2017 dollars) and continued to increase through 2014 as the WTI spot price remained higher than $97 per barrel (Figure 1). At the same time, the average EUR per horizontal oil well increased from about 50,000 barrels per well in 2008 to more than 200,000 barrels per well in 2014 as producers targeted the most productive counties and improved extraction techniques and operations to increase the productivity of the play.

figure data

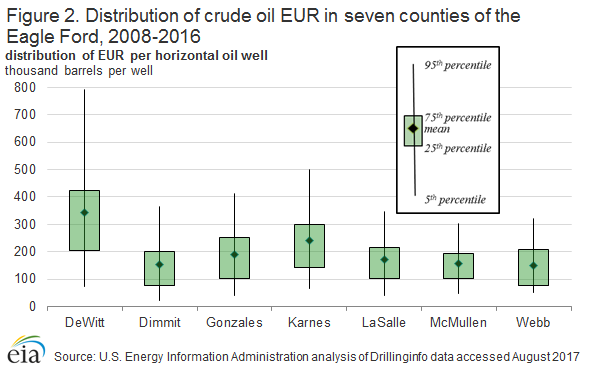

The range of EURs across counties and within each county can be large, as shown in Figure 2. More than 70% of the horizontal oil wells drilled in the Eagle Ford from 2008–2016 were drilled in seven counties: the western counties—Dimmit, La Salle, McMullen, and Webb—and the central counties—DeWitt, Gonzales, and Karnes.

figure data

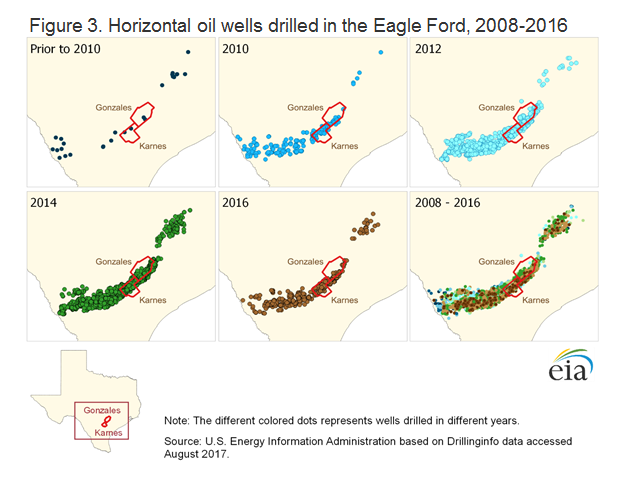

When the WTI spot price dropped to $50 per barrel in the winter of 2014–2015, the number of horizontal oil wells drilled in 2015 and 2016 in the Eagle Ford slowed appreciably. The average EUR decreased slightly because continued drilling in the sweet spots resulted in diminishing returns as wells began to interfere with each other. Producers then reduced drilling in the less productive areas and continued to make operational improvements. The progression of horizontal oil well drilling in the Eagle Ford over time is shown in Figure 3.

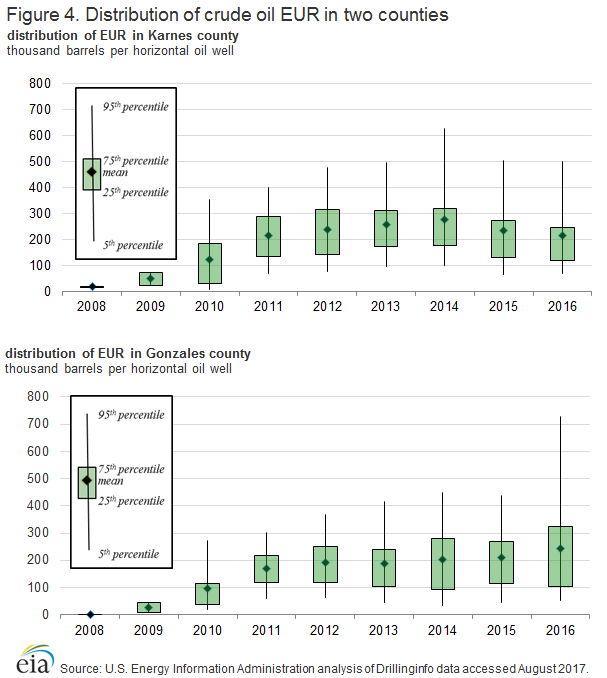

Not surprisingly, for many of the counties in Eagle Ford, the change in EUR over time looks similar to the change in EUR for the whole play as illustrated in, Karnes County, one of the major areas of development in the area (Figure 4). However, the life cycle of a play does not necessarily proceed equally across all counties, as shown by another area in the play, Gonzales County. Thus, understanding the geology within a county is important to help identify the extent of sweet spots in the county, if any, to better reflect the productive potential as the county is drilled out.

As development of a tight oil or shale gas play continues, the EUR per well decreases. This relationship means that higher prices or significant reduction in costs are needed to spur an additional increase in drilling to maintain constant production levels in a particular play.

Results

Even though the AEO2018 projections in the Reference case show a rapid increase in the production of oil and natural gas, particularly in the mid-term years, these results vary widely across the side cases constructed to measure the sensitivity of the results to the assumptions in the Reference case. These differences also affect the balance of trade related to oil and natural gas and other related energy markets.

Reference case

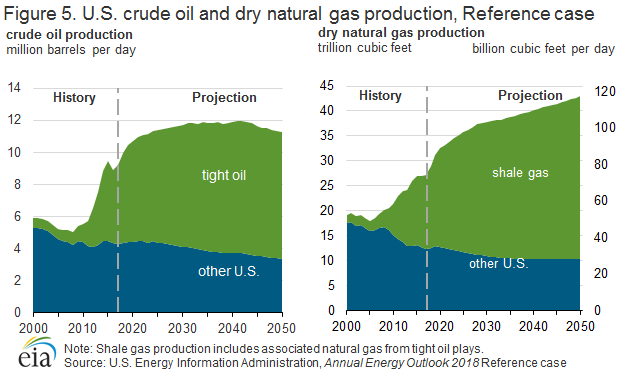

Over the past 10 years, tight oil and shale gas production in the United States has increased dramatically, accounting for 54% of crude oil production and 55% of dry natural gas production in 2017, compared with 17% for each in 2008 (Figure 5). This growth has been supported by development in the Appalachian Basin, the Williston Basin, the Western Gulf Basin and, more recently, the Permian Basin.

Total U.S. crude oil production in the AEO2018 Reference case increases over the next five years, from 9.2 million b/d in 2017 to 11.1 million b/d in 2022, and then generally flattens after 2022, staying about 11 million to 12 million b/d through 2050. Similarly, domestic dry natural gas production increases rapidly (more than 5% annually) through 2021 and then slows to an annual average growth rate of 1% through 2050 in the Reference case. With the increasing development of tight and shale resources (particularly in the Marcellus and Permian Basin plays), natural gas plant liquids production in the Reference case also increases through 2050, reaching almost 5.6 million b/d in 2050 compared with 3.7 million b/d in 2017.

However, a great deal of uncertainty exists concerning the recovery of tight oil and shale gas resources in known plays, and in the potential for production from additional plays or other layers within currently productive formations that have not been tested. The AEO Assumptions Report chapter for the Oil and Gas Supply Module provides a summary table (Table 9.3) of EURs, well spacing, and other parameters by play for tight oil and shale gas.

Refinements to current technologies and new technological advances also can have significant (but uncertain) impacts on the recoverability of tight oil and shale gas in the United States. The AEO2018 uses a simplified approach to modeling the impact of technology advancement on U.S. crude oil and natural gas costs and productivity to capture a continually changing technological landscape. This approach incorporates assumptions about average annual improvement rates that represent ongoing innovation in upstream technologies.

Areas in tight oil, tight gas [7] , and shale gas plays are divided into two productivity tiers with different assumed rates of technology change. The first tier (Tier 1) encompasses actively developing areas, and the second tier (Tier 2) encompasses areas not yet developing. Once development begins in a Tier 2 area (Tier 2 drilling ramp-up period), the rate of technological improvement doubles for wells drilling in the early development phase as producers determine how to efficiently extract the hydrocarbons and where the sweet spots are located (learning by doing). This area is then converted to Tier 1 so technological improvement for continued drilling will reflect the rates assumed for Tier 1 areas. This conversion captures the effects of diminishing returns on a per-well basis from decreasing well spacing as development progresses, the quick market penetration of technologies, and the ready application of industry practices and technologies at the time of development. The assumptions for the annual average rate of technological improvement are shown in Table 1.

| Crude Oil and Natural Gas Resource Type | Drilling Cost | Lease Equipment & Operating Cost | EUR-Tier 1 | EUR-Tier 2 | EUR-Tier 2 drilling ramp-up period |

|---|---|---|---|---|---|

| Tight oil, tight gas, & shale gas | -1.00% | -0.50% | 1.00% | 3.00% | 6.00% |

| All other | -0.25% | -0.25% | 0.25% | NA | NA |

| Source: U.S. Energy Information Administration, Annual Energy Outlook 2018 | |||||

Side cases

The AEO2018 High and Low Oil and Gas Resource and Technology cases are sensitivity cases that are based on assumptions resulting in higher and lower estimates of technically recoverable crude oil and natural gas resources than those in the Reference case. These cases allow for an examination of the potential effects of higher and lower domestic supply on spot prices, imports, and other energy markets (e.g., the electricity market), but they do not represent upper and lower bounds for future domestic oil and natural gas supply. The EUR for future drilling and rates of technological progress are critical assumptions and have a major effect on the outlook for domestic crude oil and natural gas production.

The High Oil and Gas Resource and Technology case reflects an assumed broad-based future increase across all crude oil and natural gas resources, not limited to tight oil and shale gas. In this case, the following assumptions differ from those used in the Reference case:

- 50% higher EURs for tight oil, tight gas, and shale gas wells

- Additional tight oil resources to capture the possibility that additional layers or new areas of low-permeability zones will be identified and developed

- 50% higher assumed rates of technological improvements that reduce costs and increase productivity in the United States

- 50% higher technically recoverable undiscovered resources in Alaska and the offshore Lower 48 states, reflecting more favorable resolution of the uncertainty surrounding undeveloped areas that have had little or no exploration and development activity, and where modern seismic survey data are lacking

In the Low Oil and Gas Resource and Technology case, the EURs per tight oil, tight gas, or shale gas well in the United States and undiscovered resources in Alaska and the offshore Lower 48 states are assumed to be 50% lower than in the Reference case. Rates of technological improvement that reduce costs and increase productivity in the United States are also 50% lower than in the Reference case. These assumptions increase the per-unit cost of crude oil and natural gas development in the United States. All other resource assumptions are unchanged from those in the Reference case.

Impact on domestic crude oil and dry natural gas production

In the High Oil and Gas Resource and Technology case, U.S. crude oil and dry natural gas production increases through 2050, reaching about 19.1 million b/d and 55.3 Tcf per year, respectively, in 2050 (Figure 6). Domestic crude oil production decreases for most of the projection period, and dry natural gas production stays near 30 Tcf/year from 2018 through 2050 in the Low Oil and Gas Resource and Technology case.

The difference in overall production across cases mostly reflects differences in tight oil and shale gas production. In the High Oil and Gas Resource and Technology case, higher well productivity reduces development and production costs per unit, which results in more and earlier development of tight oil and shale gas resources than in the Reference case. From 2017 through 2050, cumulative tight oil production in the High Oil and Gas Resource and Technology case is about 139 billion barrels, compared with about 93 billion barrels in the Reference Case, and cumulative shale gas production is about 1,109 Tcf in the High Oil and Gas Resource and Technology case, compared with 909 Tcf in the Reference case.

In the Low Oil and Gas Resource and Technology case, lower well productivity and rates of technological progress result in U.S. crude oil and dry natural gas production profiles that grow more slowly and result in lower levels in 2050 compared with the Reference case. Tight oil production peaks at 5.6 million b/d in 2021 and then declines through 2050. Cumulative tight oil production from 2017 through 2050 is about 63 billion barrels in the Low Oil and Gas Resource case, or 32% less than in the Reference Case. Shale gas production increase through 2050 but only reaches 22.1 Tcf in 2050 in the Low Oil and Gas Resource and Technology case compared with 32.7 Tcf in the Reference case. Cumulative shale gas production is about 663 Tcf in the Low Oil and Gas Resource and Technology case, or 27% less than in the Reference case.

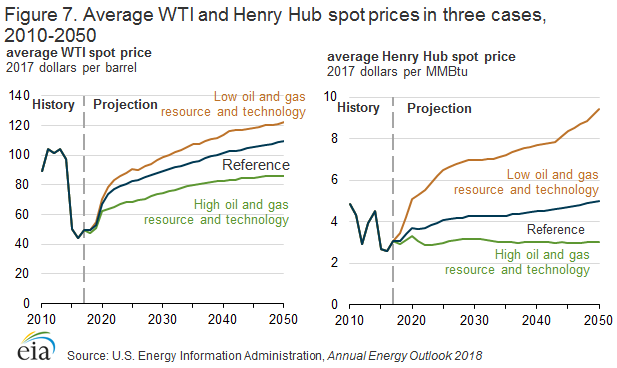

Impact on spot prices

As a result of higher volumes of lower cost crude oil and natural gas supply in the High Oil and Gas Resource and Technology case, U.S. crude oil and natural gas spot prices are lower than in the Reference case (Figure 7). The West Texas Intermediate (WTI) spot price averages $86 per barrel (2017 dollars) in 2050 in the High Oil and Gas Resource and Technology case, compared with $110 per barrel in the Reference case. The Henry Hub spot price for natural gas remains relatively flat throughout the projection period, averaging $3 per million British thermal units (MMBtu) from 2017–2050.

In the Low Oil and Gas Resource and Technology case, higher cost resources drive domestic prices higher than Reference case prices. Both the WTI and Henry Hub spot prices continue to generally increase through 2050—reaching $122 per barrel and more than $9 per MMBtu (2017 dollars) in 2050, respectively.

Impact on U.S. net import

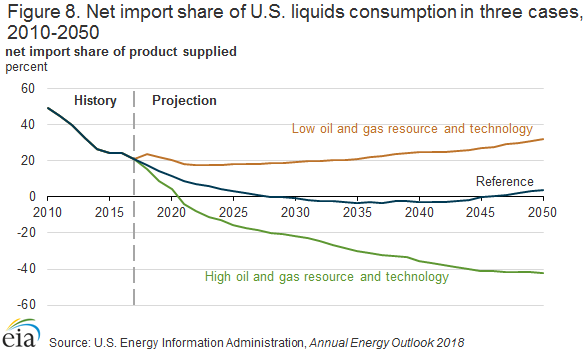

The variation in the domestic petroleum supply outlook across the Reference case and the High and Low Oil and Gas Resource cases results in significant variations in the share of net imports in total U.S. liquid fuels consumption (Figure 8). The net import share of liquids consumption has generally been declining since the high of near 60% in 2005 and was about 21% in 2017. In the Reference case, the United States becomes a net exporter of product supplied from 2029 through 2045. In the High Oil and Gas Resource and Technology case, the United States is a net exporter of petroleum on a volume basis from 2021 through 2050. Given declining domestic crude oil production in the Low Oil and Gas Resource and Technology case, net import share of liquids consumption remains higher than 18%, reaching almost 32% in 2050 in that case.

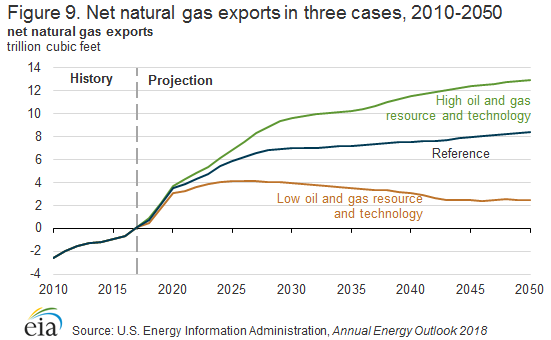

Similarly, the variation in U.S. natural gas prices across these sensitivity cases results in significant variations in the level of net exports of natural gas, especially liquefied natural gas (LNG) (Figure 9). In all cases, the United States remains a net exporter of natural gas through 2050. In the High Oil and Gas Resource and Technology case, U.S. net exports of natural gas reach nearly 13 Tcf in 2050, as low U.S. natural gas prices make U.S. LNG exports competitive relative to other suppliers. With the higher U.S. natural gas prices in the Low Oil and Gas Resource and Technology case, cumulative net U.S. natural gas exports from 2017 through 2050 are more than 50% lower than in the Reference case.

Impact on other energy markets

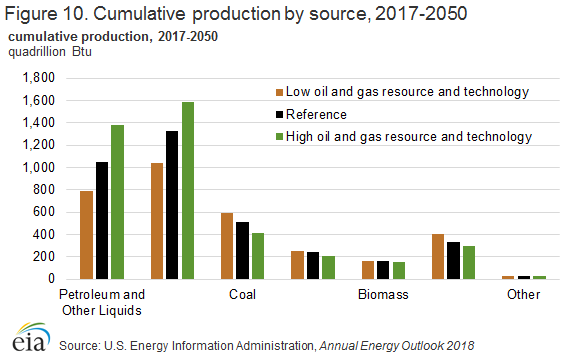

Changes in natural gas supply and the resulting change in prices have the greatest impact on coal and renewable production because demand in the electric power sector for these energy sources competes directly with natural gas (Figure 10). In the Low Oil and Gas Resource and Technology case with the Henry Hub spot price averaging almost $7 per MMBtu (2017 dollars) over the 2017–2050 period (compared with $4 per MMBtu in the Reference case), cumulative coal and other renewables production from 2017 through 2050 is 15% and 23% higher than in the Reference case on a Btu basis, respectively. With the average Henry Hub price at $3 per MMBtu in the High Oil and Gas Resource and Technology case over the same period, cumulative coal production is 96 quadrillion Btu (or 19%) lower than in the Reference case, and other renewables production is 33 quadrillion Btu (or 10%) lower than in the Reference case.

Endnotes

-

The term tight oil does not have a specific technical, scientific, or geologic definition. Tight oil is an industry convention that generally refers to oil produced from very low-permeability shale, sandstone, and carbonate formations, with permeability being a measure of the ability of a fluid to flow through the rock. In limited areas of some very low-permeability formations, small volumes of oil have been produced for many decades.

-

Shale gas production includes associated natural gas production in tight oil plays.

-

Monthly production is fit to a decline curve for each well drilled with initial production in 2008 or later and that has at least four months of production data available. The mathematical form of the curve is initially hyperbolic, but it shifts to exponential when the annual decline rate reaches 10%. The EUR is the sum of actual past production from the well, as reported in the data, and an estimate of future production based on the fitted production decline curve over a 30-year well lifetime. For more detail, see Appendix 2C in the documentation of the Oil and Gas Supply Module. (https://www.eia.gov/outlooks/aeo/nems/documentation/ogsm/pdf/m063(2017).pdf).

-

U.S. Energy Information Administration, Annual Energy Outlook 2014, Issues in Focus article “U.S. tight oil production: Alternative supply projections and an overview of EIA’s analysis of well-level data aggregated to the county level,” https://www.eia.gov/outlooks/archive/aeo14/section_issues.cfm#tight_oil

Sweet spot is an industry term for those select and limited areas within a play where the well EURs are significantly higher than those for the rest of the play—sometimes as much as 10 times higher than those for the lower-production areas within the play.

-

Lateral lengths are the horizontal sections of a well.

-

The identification of tight gas as a separate production category began with the passage of the Natural Gas Policy Act of 1978 (NGPA), which established tight gas as a separate wellhead natural gas pricing category that could obtain unregulated market-determined prices. With the full deregulation of wellhead natural gas prices and the repeal of the associated Federal Energy Regulatory Commission (FERC) regulations, tight gas no longer has a specifically defined meaning (https://pubs.naruc.org/pub.cfm?id=5380A188-2354-D714-5108-9FFD2F8F1A72 Accessed 2/9/2018). These resources have been in production since the early 1980s and refer to natural gas produced from low-permeability sandstone and carbonate reservoirs. Tight gas and shale gas are reported separately in the AEO; however, the distinction between tight gas and shale gas is fading because both are produced from low-permeability rock primarily with horizontal drilling and hydraulic fracturing.