|

Analysis of Crude Oil Production in the Arctic National Wildlife Refuge |

|

|

Methodology and Assumptions The effects of opening the coastal plain area of ANWR were determined by incorporating the ANWR region into the National Energy Modeling System (NEMS).5 The key assumptions required to project crude oil production from the coastal plain of ANWR include:

Timing of First Production At the present time, there has been no crude oil production in the ANWR coastal plain region. This analysis assumes that enactment of the legislation in 2008 would result in first production from the ANWR area in 10 years, i.e., 2018. The primary constraints to a rapid development of ANWR oil resources are the limited weather “windows” for collecting seismic data and drilling wells (a 3-to-4 month winter window) and for ocean barging of heavy infrastructure equipment to the well site (a 2-to-3 month summer window). The assumption that ANWR oil production would begin 10 years after legislation approves the Federal oil and natural gas leasing in the 1002 Area is based on the following 8-to-12 year timeline:

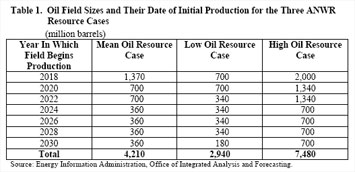

The 10-year timeline for developing ANWR petroleum resources assumes that there is no protracted legal battle in approving the BLM’s draft Environmental Impact Statement, the BLM’s approval to collect seismic data, or the BLM’s approval of a specific lease-development proposal. The Alaska North Slope Badami and Alpine oil fields are recent examples of how long it might take to develop new ANWR oil fields. Located near the western border of ANWR, on State lands, the Badami field was discovered in 1990 and went into production in 1998, thereby taking 8 years between the oil discovery and initial production.6 On the western border of the State lands, near the National Petroleum Reserve-Alaska, the Alpine field was discovered in 1994 and initial oil production occurred in 2000, thereby taking 6 years from discovery.7 These Alaska North Slope oil field development time delays do not include the time delays associated with BLM leasing, the collection and interpretation of seismic data, and the drilling of exploratory wells. Timing of Continuing Development This analysis assumes that much of the oil resources in ANWR, like the other oil resources on Alaska's North Slope, could be profitably developed given the current levels of technology and at current and projected oil prices. This analysis also assumes that new fields in ANWR will begin development 2 years after a prior ANWR field begins oil production. The decision to use a 2-year time lag in bringing ANWR fields into production is driven by four factors. First, there is the large expected size of the ANWR fields, which complicates the logistical problems associated with their development. Second, there is considerable investment infrastructure required both to begin production in these fields and to link these fields to the TransAlaska Pipeline System (TAPS). Third, there is competition in investment and drilling resources from other domestic and foreign projects, which potentially limits the resources available for ANWR development. Finally, increasing the rate of ANWR development might also require an expansion of TAPS throughput capacity. This study does not assume that the expected rate of technological change in the oil and natural gas industry will affect the rate of development of ANWR. While a higher rate of technological development might reduce costs and lead to more efficient development of ANWR resources, the primary impediment to the development of ANWR resources is the current legal restriction that precludes access to these oil resources. Field Size Distributions The current analysis uses the USGS assessment of potential field sizes in the coastal plain area, based on its assessment of the underlying geology. For the purposes of evaluating the impact of opening ANWR for U.S. markets, EIA assumed that State and Native lands within the coastal plain of ANWR would be opened for development. In the mean oil resource case, the total volume of technically recoverable crude oil projected to be found within the coastal plain area is 10.4 billion barrels, compared to 5.7 billion barrels for the 95-percent probability estimate, and 16.0 billion barrels for the 5-percent probability estimate. Because the USGS 5-percent and 95-percent probability oil resource estimates are asymmetric around the mean estimate, the expected field size distribution and, in turn, the distribution of projected oil production are also asymmetric with respect to the mean estimate’s field sizes and projected production.

In the mean oil resource case, the largest projected field in ANWR is nearly 1.4 billion barrels. While considerably smaller than the 13.5-billion-barrel Prudhoe Bay field,8 this would be larger than any new domestic onshore field brought into production in decades. Subsequent fields, which are developed through 2030 in the mean resource case, are expected to be smaller, with two additional fields each with 700 million barrels of oil and four additional fields each with 360 million barrels of oil (Table 1). To put these field sizes in context with recent North Slope Alaska oil discoveries, the Alpine Oil field, the largest field to start producing in recent years, is estimated to have 540 million barrels of ultimate recovery.9 Because the larger fields are generally easier to find and cheaper to develop, EIA’s analysis assumes that the largest oil fields are developed first. Because the USGS assessment of ANWR oil resources has not changed since 2001, the ANWR field sizes used in this analysis are the same as those used in EIA’s 2004 ANWR analysis. Production Profiles Potential production from ANWR fields is based on the size of the field discovered and the production profiles of other fields of the same size in Alaska with similar geological characteristics. In general, fields are assumed to take 3 to 4 years to reach peak production, maintain peak production for 3 to 4 years, and then decline until they are no longer profitable and are closed. Identical production profiles were used in the prior EIA report. Current Oil Market Conditions Alaska North Slope crude oil prices have increased dramatically, rising from $23.62 per barrel in 2000 to $47.05 per barrel in 2005, a 99 percent increase, and to $63.69 in 2007, a 170 percent increase.10 Alaska North Slope oil prices have continued to increase in 2008, in line with other crude prices. The price of West Texas Intermediate crude oil, which typically has a price premium of $5 to $8 per barrel over Alaska North Slope crude, has recently exceeded $120 per barrel. Considered in isolation, higher prices alone might raise an expectation of higher ultimate recovery from whatever oil resource exists in place.11 Higher prices can motivate efforts to increase the recovery factor through more intensive drilling and through the application of advanced techniques to increase recovery factors. While the menu of available methods may in some cases be limited by the features of the Alaska North Slope environment, for example, steam-injection enhanced oil recovery of the near-surface West Sak heavy oil deposits could endanger the permafrost, some techniques would likely still be suitable. Higher prices also make it more attractive to go after very small fields that are in close proximity to the larger fields that are presumed to be the initial development targets. However, as discussed below, the main impact of such approaches on the amount of oil actually recovered from ANWR is likely to occur after 2030, the current time horizon for EIA analyses. As previously noted, there is a strong incentive for serial development of the ANWR resource, starting with the largest fields first. As shown in Table 1, the expected size of fields developed in each year through 2030 declines over time. Based on the field size distributions provided for USGS for each of the resource cases, the expected target field in 2030 is estimated to contain 180 million barrels of recoverable oil in the low (most unfavorable) resource case and even more oil in the other two resource cases. Based on recent development practice, oil fields smaller than 10 million barrels of recoverable oil that lie in close proximity to existing developed fields in Alaska were deemed desirable development targets even when crude oil prices were substantially below their current level.12 Oil fields of 180 million barrels in proximity to even larger developed fields within ANWR are likely to present attractive development opportunities even at prices well below today’s level. Crude oil prices could be a significant factor in determining whether much smaller fields within ANWR would also be attractive to develop. However, decisions regarding such smaller fields would most likely be taken sometime after 2030, affecting production levels only after such fields are actually brought on line. A similar timing issue arises with respect to the application of advanced techniques to raise ultimate recovery factors in fields of various sizes. With all new fields already assumed to be developed in an efficient manner if ANWR resources are opened to leasing and development, investments in such techniques would predominantly occur well after fields are first developed. While prices can influence decisions regarding the application of advanced techniques, the timing of ANWR development is such that the major impact on production from large fields in ANWR is not likely to be felt before 2030. However, a more significant impact could be realized in later years. The increase in drilling costs over time is another important consideration that mitigates against an immediate impact of higher oil prices on the production profile following initial development in a scenario where ANWR resources are open to leasing and development. For example, the American Petroleum Institute’s (API) Joint Association Survey of Drilling Costs (JAS) reports, that for the 10,000 to 12,499-foot well-depth interval, the average cost of drilling a domestic13 onshore oil well increased from $111 per foot-drilled in 2000 to $294 per foot-drilled in 2005, a 165-percent cost increase.14 For the same well-depth interval, Alaska onshore oil well drilling costs increased from $283 per foot-drilled in 2000 to $1,880 per foot-drilled in 2005, a 564-percent cost increase.15 The vast majority of the oil wells drilled in Alaska occur on the North Slope. These API well drilling cost averages illustrate two aspects of Alaska North Slope oil field development costs. First, Alaska oil fields have always been more expensive to develop than lower-48 oil fields due to the North Slope’s remote location, harsh winters, and the environmental requirement to maintain the permafrost layer. Second, in the current market environment, where producers are completing for scarce oil field equipment, drilling rigs, and skilled labor, the remoteness of the Alaska North Slope and its limited drilling season works to its detriment, causing oil field development costs to increase more than that witnessed in the lower-48. In the lower-48, a drilling company might move a land rig only a couple of miles, or at most, a couple of hundred miles to another drilling site. In contrast, the deployment of new rigs to the Alaska North Slope requires that they be transported many thousands of miles without any option for quick redeployment. Over the long-term, both lower-48 and Alaska North Slope oil field development costs are expected to subside as the supply of drilling rigs, oil field equipment, and skilled labor increases to catch up with demand. However, it is unlikely that Alaska North Slope oil field development costs will decline to year 2000 levels. In summary, the basic intuition that higher crude oil prices would likely result in higher ultimate recovery from whatever resource exists in place is sound. However, given the timing and cost considerations outlined above, EIA does not expect the recent increase in oil prices to affect the projected profile of ANWR development and production activities prior to 2030, the end of the time horizon for this analysis. Therefore, this current analysis of projected production from ANWR through 2030 parallels our prior recent analyses of this topic that have used similar or identical information on ANWR resources notwithstanding the recent run-up in world crude oil prices. |