Released: November 28, 2012

Next Release: December 5, 2012

Market Implications of Increased Domestic Production of Light Sweet Crude Oil

Rising domestic production of light sweet crude oil, especially from tight oil formations in North Dakota and Texas, is already leading to adjustments in oil markets. U.S. Gulf Coast refineries are using these high-quality domestically produced streams to replace imported oil from West Africa and other sources. Flows of light sweet crude oil via rail to both East and West Coast refiners are also increasing.

If U.S. light sweet crude oil production continues to rise strongly over the next several years, Gulf Coast refiners may be able to satisfy all of their current demand for light sweet crude oil with domestic production. Gulf Coast refiners could probably absorb additional volumes of light sweet crude oil to replace some imports of heavier crude oil streams that many of the refineries in the region are designed to use, but this could reduce the production of some high-value products and also reduce operating rates of some sophisticated refinery units used to convert low-quality, lower-priced heavy crudes into high-value products. Traditional price premiums for light crude would probably have to fall to incentivize such behavior. For this reason, increased exports may be a more attractive option for producers if an excess of light sweet crude oil in the Gulf Coast market actually develops. In the November Short-Term Energy Outlook, the U.S. Energy Information Administration (EIA) projected that U.S. crude oil production will reach 6.85 million barrels per day (bbl/d) in 2013, a 0.52-million-bbl/d increase from the 2012 level that is itself projected to be 0.78 million bbl/d above the 2011 level.

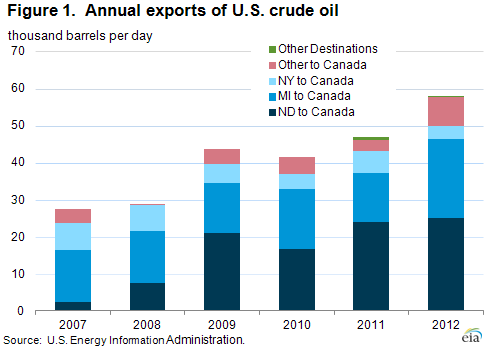

Currently, crude oil produced in the United States can be exported only when a license is granted by the Bureau of Industry and Security (BIS), which is a part of the U.S. Department of Commerce, under regulations promulgated in the Code of Federal Regulations Title 15 Part 754.2. Notwithstanding these requirements, export volumes are growing. Year-to-date (through August) exports of crude oil averaged 58,000 bbl/d, more than twice the volume exported in 2007 (Figure 1). Most exported crude oil is shipped from the Midwest to Canada.

According to the regulation, BIS will approve applications to export crude oil for the following kinds of transactions if BIS determines that the export is consistent with the specific requirements pertinent to that export:

• Exports from Alaska's Cook Inlet

• Exports to Canada for consumption or use therein

• Exports in connection with refining or exchange of Strategic Petroleum Reserve oil

• Exports of 25,000 bbl/d of California heavy crude oil

• Exports that are consistent with findings made by the president under an applicable statute

• Exports of foreign-origin crude oil where, based on written documentation satisfactory to BIS, the exporter can demonstrate that the oil is not of U.S. origin and has not been commingled with oil of U.S. origin.

Outside of these conditions, the regulation stipulates that BIS will review all other applications to export crude oil on a case-by-case basis, and will approve such applications if it determines that the proposed export is consistent with the national interest and the purposes of the Energy Policy and Conservation Act (EPCA). License exceptions are provided for certain types of crude oil exports, including Alaska North Slope crude transported through the Trans-Alaska Pipeline System.

When BIS grants a license to export crude oil, the license is granted for a defined period of time, limited to one year from date of issue, and for a specific dollar value, as opposed to a specific volume of crude oil. Licenses for export of crude oil to Canada are regularly requested, and BIS is obligated by statute to approve such requests so long as they meet the requirement that the crude oil be processed in Canada, rather than stored and then re-exported.

As noted, exports of crude oil from the United States have been increasing and, at 58,000 bbl/d year-to-date through August, are on pace to be the highest since 1999, when the United States exported 118,000 bbl/d of crude oil, more than half of which came from Alaska. Most of the growth in export volumes has come from North Dakota. Year-to-date through August, North Dakota has exported 25,000 bbl/d of crude oil to Canada, up from just 2,000 bbl/d in 2007. Prior to the growth in North Dakota exports, the largest volumes came from Michigan for processing in refineries in Sarnia, Ontario. Other significant export flows from the United States to Canada have come from New York. Prior to 2007, licenses were also granted to export Alaskan North Slope crude to the Pacific Rim countries, most notably South Korea. Some limited volumes have also gone to Latin American countries such as Mexico and Costa Rica.

Since 2011, applications received by BIS to export crude have increased along with the increase in light sweet crude production from tight oil formations in Texas and North Dakota (Eagle Ford and Bakken). As light sweet crude oil production in the United States continues to increase, applications to export crude oil are also likely to rise.

Gasoline and diesel fuel prices both increase

The U.S. average retail price of regular gasoline increased a penny last week to $3.44 per gallon, 13 cents higher than last year at this time. Prices east of the Rockies increased, while those in the West decreased. The largest increase came in the Midwest, where the average price rose four cents to $3.39 per gallon, while both the East Coast and Gulf Coast prices increased a penny, to $3.49 per gallon and $3.17 per gallon, respectively. The Rocky Mountain price is now $3.47 per gallon and the West Coast price is $3.67 per gallon, both decreases of four cents from last week.

The national average diesel fuel price increased six cents to $4.03 per gallon, seven cents higher than last year at this time. The only decrease came in the Rocky Mountain region, where the price is down less than a penny to remain at $4.06 per gallon. The largest increase came in the Midwest, where the price increased 11 cents to $4.02 per gallon. The East and Gulf Coast prices both increased four cents, to $4.09 per gallon and $3.90 per gallon, respectively. The Gulf Coast is now the only region where the price is less than $4 per gallon. Rounding out the regions, the West Coast price remains the highest in the Nation at $4.12 per gallon, an increase of two cents from last week.

Propane inventories post unseasonal build

Total U.S. inventories of propane increased 0.2 million barrels last week to end at 72.8 million barrels, 22 percent higher than the same week a year ago. The Gulf Coast region led the gain, with 0.5 million barrels. Meanwhile, Midwest, Rocky Mountain/West Coast, and East Coast stocks each fell 0.1 million barrels. Propylene non-fuel-use inventories represented 5.8 percent of total propane inventories.

Residential heating fuel prices increase, wholesale changes mixed

Residential heating oil prices increased during the period ending November 26, 2012. The average residential heating oil price increased by 3 cents to $4.00 per gallon, nearly 11 cents per gallon higher than the same time last year. Wholesale heating oil prices rose less than 5 cents per gallon last week to reach $3.25 per gallon, almost 19 cents per gallon more than last year at this time.

The average residential propane price increased by less than a penny last week to slightly more than $2.41 per gallon, 43 cents per gallon lower than the same period last year. Wholesale propane prices decreased by 2 cents to $0.92 per gallon for the week ending November 26, 2012, 53 cents per gallon lower than the November 28, 2011 price.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

|

|

||||||

| Retail Data | Change From Last | Retail Data | Change From Last | ||||

| 11/26/12 | Week | Year | 11/26/12 | Week | Year | ||

| Gasoline | 3.437 | Heating Oil | 4.004 | ||||

| Diesel Fuel | 4.034 | Propane | 2.414 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Change From Last | Stocks Data | Change From Last | ||||

| 11/23/12 | Week | Year | 11/23/12 | Week | Year | ||

| Crude Oil | 374.1 | Distillate | 112.0 | ||||

| Gasoline | 204.3 | Propane | 72.847 | ||||