In the News:

U.S. LNG exports set another record in December

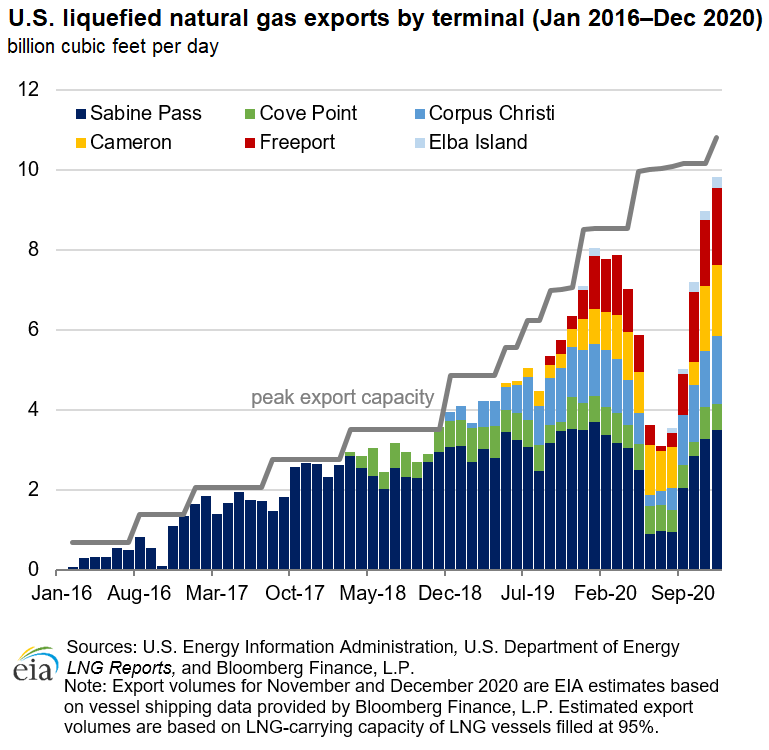

U.S. exports of liquefied natural gas (LNG) set a new record in December after a record-breaking November 2020, averaging 9.8 billion cubic feet per day (Bcf/d), according to the U.S. Energy Information Administration (EIA) estimates based on the shipping data provided by Bloomberg Finance, L.P. U.S. LNG exports in December were more than three times higher than the reduced export levels in the summer of 2020.

Several factors have contributed to higher levels of U.S. LNG exports in recent months. LNG demand increased due to colder-than-normal winter temperatures in key Asian LNG-consuming markets. Moreover, supplies of LNG decreased because of unplanned outages at LNG export facilities in Australia, Malaysia, Qatar, Norway, Nigeria, and Trinidad and Tobago. Reduction in LNG supply led to higher international natural gas and LNG prices in Asia and Europe, attracting higher volumes of flexible LNG supplies from the United States.

From April to July 2020, natural gas and LNG prices in Asia and Europe have declined to all-time historical lows, which affected economic viability of flexible U.S. LNG exports and led to numerous cargo cancelations. Prices began to recover in August, and by December, prices have more than quadrupled compared to the low levels of the summer months. The JKM price benchmark (representing spot and forward LNG prices in Japan, South Korea, Taiwan, and China) averaged $10.82 per million British thermal units (MMBtu) in December 2020, and the TTF—a key European price benchmark—averaged $5.80/MMBtu. By the end of December, JKM prices continued to increase and reached $15.10/MMBtu on December 31, 2020—the highest level in the last seven years, according to pricing data provided by S&P Global Platts.

Since mid-October, natural gas and LNG prices in global spot and futures markets have exceeded prices in crude oil-indexed long-term LNG contracts. Although deliveries under long-term contracts (which account for 70% of global LNG trade) have been increasing since September 2020, supply shortages caused by unplanned outages at various LNG export facilities worldwide reduced contractual export volumes. Higher global prices and reduced exports under term contracts resulted in higher export volumes of flexible LNG, particularly from the United States. The majority of U.S. LNG export contracts do not have fixed destinations in contractual clauses, allowing exporters of U.S. LNG to ship it on a spot and short-term basis to the highest-priced markets worldwide. Since June 2020, more than 50% of U.S. LNG exports went to countries in Asia, about 30% to countries in Europe, and the remaining volumes to countries in the Middle East, Africa, and Latin America, according to the U.S. Department of Energy’s LNG Reports and EIA’s data for November 2020.

EIA expects U.S. LNG exports to remain at record-high levels this winter. In the December 2020 Short Term Energy Outlook (STEO), EIA forecasts that U.S. LNG exports will average 9.5 Bcf/d in the first quarter of 2021 and 8.5 Bcf/d on an annual basis this year, a 30% increase from 2020.

Overview:

(For the week ending Wednesday, December 16, 2020)

- Natural gas spot prices rose at most locations this report week (Wednesday, December 30 to Wednesday, January 6). The Henry Hub spot price rose from $2.39 per million British thermal units (MMBtu) last Wednesday to $2.70/MMBtu yesterday.

- At the New York Mercantile Exchange (Nymex), the price of the February 2021 contract increased 29¢, from $2.422/MMBtu last Wednesday to $2.716/MMBtu yesterday. The price of the 12-month strip averaging February 2021 through January 2022 futures contracts climbed 23¢/MMBtu to $2.837/MMBtu.

- The net withdrawals from working gas totaled 130 billion cubic feet (Bcf) for the week ending January 1. Working natural gas stocks totaled 3,330 Bcf.

- The natural gas plant liquids composite price at Mont Belvieu, Texas, rose by 26¢/MMBtu, averaging $6.50/MMBtu for the week ending January 6. The price of butane fell 21% as logistical constraints were alleviated, allowing butane prices to return to trend after rapid price increase throughout December. The prices of ethane, propane, isobutane, and natural gasoline rose by 10%, 8%, 8%, and 6%, respectively.

- According to Baker Hughes, for the week ending Tuesday, December 29, the natural gas rig count increased by 2 to 81. The number of oil-directed rigs rose by 5 to 263. The total rig count increased by 8, and it now stands at 346.

Prices/Supply/Demand:

Natural gas prices rise at most locations outside of California. This report week (Wednesday, December 30 to Wednesday, January 6), the Henry Hub spot price rose 31¢ from a low of $2.39/MMBtu last Wednesday to $2.70/MMBtu yesterday. Temperatures were generally much warmer than normal for the first week of January across the Lower 48 states. At the Chicago Citygate, the price increased 27¢ from a low of $2.31/MMBtu last Wednesday to $2.58/MMBtu yesterday.

California prices are down. The price at SoCal Citygate in Southern California decreased 78¢ from a high of $4.49/MMBtu last Wednesday to a low of $3.71/MMBtu yesterday. Natural gas demand was relatively weak in Southern California at points during the report week, with natural gas sendout reaching a low of 2.7 Bcf on January 1, contributing to a 0.2 Bcf storage injection on that day. The price at PG&E Citygate in Northern California traded in a narrow range and fell 8¢, down from a high of $3.64/MMBtu last Wednesday to a low of $3.56/MMBtu yesterday.

Northeast prices rise. At the Algonquin Citygate, which serves Boston-area consumers, the price went up 44¢ from $2.55/MMBtu last Wednesday to $2.99/MMBtu yesterday. At the Transcontinental Pipeline Zone 6 trading point for New York City, the price increased 49¢ from $2.31/MMBtu last Wednesday to a high of $2.80/MMBtu yesterday.

The Tennessee Zone 4 Marcellus spot price increased 33¢ from $1.97/MMBtu last Wednesday to $2.30/MMBtu yesterday. The price at Dominion South in southwest Pennsylvania rose 35¢ from $1.97/MMBtu last Wednesday to $2.32/MMBtu yesterday.

Permian Basin basis to Henry Hub goes positive as Permian Highway pipeline enters service. The price at the Waha Hub in West Texas, which is located near Permian Basin production activities, averaged $2.42/MMBtu last Wednesday, 3¢/MMBtu above the Henry Hub price, briefly pushing the basis to the Henry Hub into positive territory. Yesterday, the price at the Waha Hub averaged a weekly high of $2.52/MMBtu, 18¢/MMBtu lower than the Henry Hub price. Kinder Morgan’s Permian Highway pipeline entered service on January 1, adding 2.1 Bcf/d of takeaway capacity out of the Permian Basin to Katy, Texas, near Houston, with connections to the U.S. Gulf Coast and Mexico markets.

Supply rises. According to data from IHS Markit, the average total supply of natural gas rose by 0.2% compared with the previous report week. Dry natural gas production decreased by 0.3% compared with the previous report week. Average net imports from Canada increased by 6.0% from last week.

Demand falls across all domestic sectors. Total U.S. consumption of natural gas fell by 2.9% compared with the previous report week, according to data from IHS Markit. Natural gas consumed for power generation climbed by 2.7% week over week. In the residential and commercial sectors, consumption declined by 7.6%. Industrial sector consumption decreased by 0.9% week over week. Natural gas exports to Mexico increased 8.2%. Natural gas deliveries to U.S. liquefied natural gas (LNG) export facilities (LNG pipeline receipts) were about the same as last week averaging 11.0 Bcf/d.

U.S. LNG exports decrease week over week. Twenty one LNG vessels (seven from Sabine Pass, five from Freeport, four each from Cameron and Corpus Christi, and one from Cove Point) with a combined LNG-carrying capacity of 77 Bcf departed the United States between December 31, 2020 and January 6, 2021, according to shipping data provided by Bloomberg Finance, L.P.

Storage:

The net withdrawals from storage totaled 130 Bcf for the week ending January 1.

According to The Desk survey of natural gas analysts, estimates of the weekly net change to working natural gas stocks ranged from net withdrawals of 120 Bcf to 158 Bcf, with a median estimate of 135 Bcf.

More storage data and analysis can be found on the Natural Gas Storage Dashboard and the Weekly Natural Gas Storage Report.

See also:

| Spot Prices ($/MMBtu) | Thu, 31-Dec |

Fri, 1-Jan |

Mon, 4-Jan |

Tue, 5-Jan |

Wed, 6-Jan |

|---|---|---|---|---|---|

| Henry Hub | 2.39 | Holiday | 2.57 | 2.72 | 2.70 |

| New York | 2.33 | Holiday | 2.69 | 2.79 | 2.80 |

| Chicago | 2.31 | Holiday | 2.49 | 2.59 | 2.58 |

| Cal. Comp. Avg,* | 3.19 | Holiday | 3.00 | 2.99 | 3.04 |

| Futures ($/MMBtu) | |||||

| February Contract | 2.539 | Holiday | 2.581 | 2.702 | 2.716 |

| March Contract | 2.526 | Holiday | 2.561 | 2.673 | 2.684 |

| *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| Spot Prices ($/MMBtu) | Thu, 24-Dec |

Fri, 25-Dec |

Mon, 28-Dec |

Tue, 29-Dec |

Wed, 30-Dec |

|---|---|---|---|---|---|

| Henry Hub | 2.60 | Holiday | 2.33 | 2.37 | 2.39 |

| New York | 2.99 | Holiday | 2.41 | 2.41 | 2.31 |

| Chicago | 2.48 | Holiday | 2.17 | 2.28 | 2.31 |

| Cal. Comp. Avg,* | 3.36 | Holiday | 3.52 | 3.48 | 3.40 |

| Futures ($/MMBtu) | |||||

| January Contract | 2.518 | Holiday | 2.305 | 2.467 | Expired |

| February Contract | 2.512 | Holiday | 2.326 | 2.444 | 2.422 |

| March Contract | 2.498 | Holiday | 2.329 | 2.439 | 2.422 |

| *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| Spot Prices ($/MMBtu) | Thu, 17-Dec |

Fri, 18-Dec |

Mon, 21-Dec |

Tue, 22-Dec |

Wed, 23-Dec |

|---|---|---|---|---|---|

| Henry Hub | 2.70 | 2.69 | 2.66 | 2.77 | 2.68 |

| New York | 5.33 | 2.85 | 3.02 | 2.69 | 2.15 |

| Chicago | 2.54 | 2.57 | 2.49 | 2.61 | 2.59 |

| Cal. Comp. Avg,* | 3.47 | 3.37 | 3.46 | 3.51 | 3.38 |

| Futures ($/MMBtu) | |||||

| January Contract | 2.636 | 2.700 | 2.705 | 2.780 | 2.680 |

| February Contract | 2.637 | 2.681 | 2.689 | 2.749 | 2.588 |

| *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. | |||||

| Source: NGI's Daily Gas Price Index | |||||

| U.S. natural gas supply - Gas Week: (12/31/20 - 1/6/21) | |||

|---|---|---|---|

Average daily values (Bcf/d): |

|||

this week |

last week |

last year |

|

| Marketed production | 102.9 |

103.3 |

107.5 |

| Dry production | 91.1 |

91.4 |

95.5 |

| Net Canada imports | 5.9 |

5.5 |

4.6 |

| LNG pipeline deliveries | 0.3 |

0.1 |

0.2 |

| Total supply | 97.2 |

97.0 |

100.2 |

|

Source: IHS Markit | |||

| U.S. natural gas consumption - Gas Week: (12/31/20 - 1/6/21) | |||

|---|---|---|---|

Average daily values (Bcf/d): |

|||

this week |

last week |

last year |

|

| U.S. consumption | 89.4 |

92.0 |

92.4 |

| Power | 26.8 |

26.1 |

28.3 |

| Industrial | 24.5 |

24.7 |

25.1 |

| Residential/commercial | 38.1 |

41.2 |

39.0 |

| Mexico exports | 5.1 |

4.7 |

4.7 |

| Pipeline fuel use/losses | 7.5 |

7.6 |

8.0 |

| LNG pipeline receipts | 11.0 |

11.0 |

8.4 |

| Total demand | 113.0 |

115.3 |

113.4 |

|

Source: IHS Markit | |||

| Rigs | |||

|---|---|---|---|

Tue, December 29, 2020 |

Change from |

||

last week |

last year |

||

| Oil rigs | 267 |

1.1% |

-60.1% |

| Natural gas rigs | 83 |

0.0% |

-32.5% |

| Note: Excludes any miscellaneous rigs | |||

| Rig numbers by type | |||

|---|---|---|---|

Tue, December 29, 2020 |

Change from |

||

last week |

last year |

||

| Vertical | 17 |

0.0% |

-61.4% |

| Horizontal | 313 |

1.3% |

-55.3% |

| Directional | 21 |

-4.5% |

-58.8% |

| Source: Baker Hughes Co. | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (Bcf) |

||||

| Region | 2021-01-01 |

2020-12-25 |

change |

|

| East | 765 |

810 |

-45 |

|

| Midwest | 923 |

973 |

-50 |

|

| Mountain | 196 |

204 |

-8 |

|

| Pacific | 282 |

289 |

-7 |

|

| South Central | 1,163 |

1,183 |

-20 |

|

| Total | 3,330 |

3,460 |

-130 |

|

|

Source: Form EIA-912, Weekly Underground Natural Gas Storage Report | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (1/1/20) |

5-year average (2016-2020) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 771 |

-0.8 |

737 |

3.8 |

|

| Midwest | 905 |

2.0 |

871 |

6.0 |

|

| Mountain | 173 |

13.3 |

171 |

14.6 |

|

| Pacific | 251 |

12.4 |

274 |

2.9 |

|

| South Central | 1,093 |

6.4 |

1,075 |

8.2 |

|

| Total | 3,192 |

4.3 |

3,129 |

6.4 |

|

| Source: Form EIA-912, Weekly Underground Natural Gas Storage Report | |||||

| Temperature – heating & cooling degree days (week ending Dec 31) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDD deviation from: |

CDD deviation from: |

|||||||

| Region | HDD Current |

normal |

last year |

CDD Current |

normal |

last year |

||

| New England | 205 |

-55 |

2 |

0 |

0 |

0 |

||

| Middle Atlantic | 215 |

-33 |

33 |

0 |

0 |

0 |

||

| E N Central | 267 |

-15 |

95 |

0 |

0 |

0 |

||

| W N Central | 289 |

-18 |

69 |

0 |

0 |

0 |

||

| South Atlantic | 175 |

0 |

80 |

5 |

-1 |

-10 |

||

| E S Central | 168 |

-13 |

79 |

0 |

-1 |

-1 |

||

| W S Central | 96 |

-40 |

11 |

3 |

1 |

-2 |

||

| Mountain | 227 |

-8 |

-19 |

0 |

0 |

0 |

||

| Pacific | 132 |

6 |

-4 |

0 |

0 |

0 |

||

| United States | 202 |

-16 |

44 |

1 |

0 |

-2 |

||

|

Note: HDD = heating degree day; CDD = cooling degree day Source: National Oceanic and Atmospheric Administration | ||||||||

Average temperature (°F)

7-day mean ending Dec 31, 2020

Source: National Oceanic and Atmospheric Administration

Deviation between average and normal (°F)

7-day mean ending Dec 31, 2020

Source: National Oceanic and Atmospheric Administration

{kind=link}