- Key takeaways from the Reference case and side cases

- The Annual Energy Outlook 2022 explores long-term energy trends in the United States

- What is the AEO2022 Reference case?

- What are the side cases?

- Motor gasoline remains the most prevalent transportation fuel despite electric vehicles gaining market share

- Energy-related carbon dioxide (CO2) emissions dip through 2035 before climbing later in the projection years

- Energy consumption increases through 2050 as population and economic growth outweighs efficiency gains

- Electricity continues to be the fastest-growing energy source in buildings, with renewables and natural gas providing most of the incremental electricity supply

- Electricity demand grows slowly across the projection period, which increases competition among fuels

- Renewable electricity generation increases more rapidly than overall electricity demand through 2050

- Battery storage complements growth in renewables generation and reduces natural gas-fired and oil-fired generation during peak hours

- As coal and nuclear generating capacity retire, new capacity additions come largely from wind and solar technologies

- U.S. production of natural gas and petroleum and other liquids rises amid growing demand for exports and industrial uses

- Driven by rising prices, U.S. crude oil production in the Reference case returns to pre-pandemic levels in 2023 and stabilizes over the long term

- Refinery closures lower domestic crude oil distillation operating capacity, but refinery utilization rates remain flat over the long term

- Consumption of renewable diesel increases as a share of the domestic fuel mix

Consumption of biofuels as a share of the domestic fuel mix increases in AEO2021

Biofuels consumption decreases less than petroleum consumption

Although response to the COVID-19 pandemic affected demand for all liquid fuels in 2020, biofuel consumption has not decreased as much as petroleum-based fuels. AEO2021’s Reference case shows biofuels production returning to 2019 levels in 2021, slightly faster than petroleum-based transportation fuels (motor gasoline and diesel), contributing to an increasing share of biofuels in the domestic fuel mix.

Biofuels consumption is supported by regulation

Biofuels consumption returns to 2019 levels faster than petroleum-based fuels mainly because of regulatory support, such as the federal Renewable Fuel Standard (RFS) program, which is administered by the U.S. Environmental Protection Agency (EPA) and is used to set annual U.S. renewable fuel volume targets. In the model, the RFS is a minimum level that must be met, so even when total transportation fuel demand drops, the RFS still requires a certain level of renewable fuel. State policy such as California’s Low Carbon Fuel Standard (LCFS) is also designed to encourage domestic biofuels production.

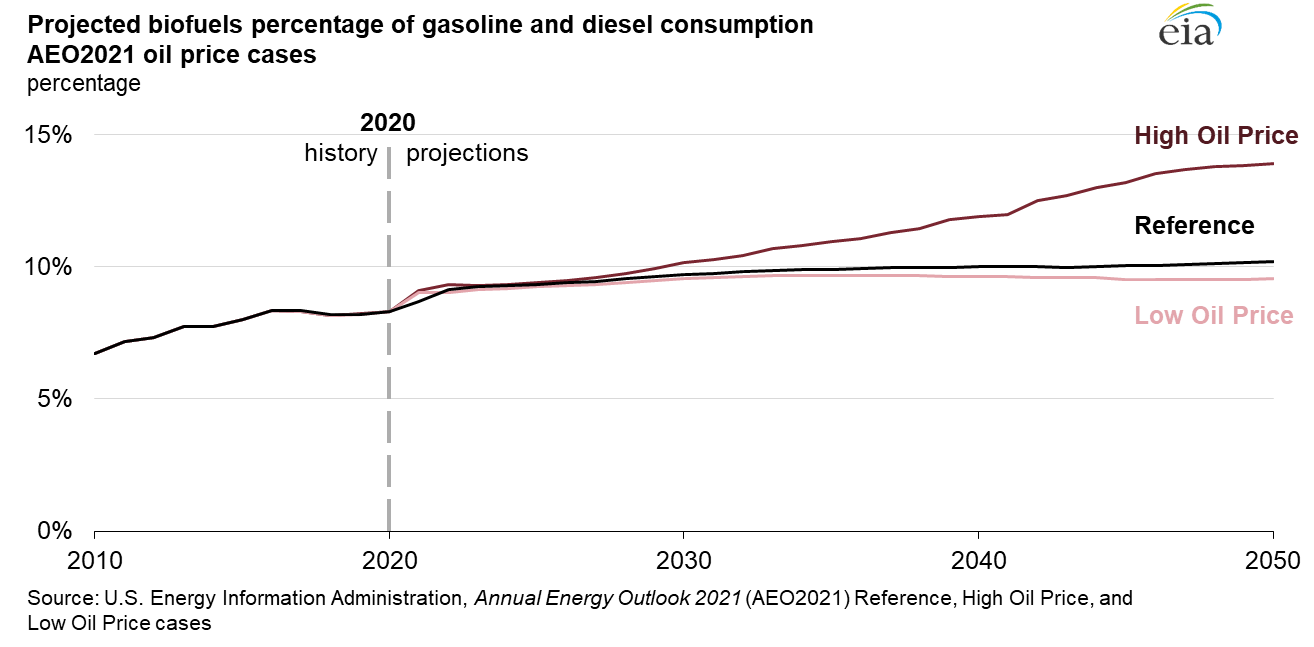

Biofuels use increases as a share of the total in the Reference case

In this year’s Reference case, EIA projects that the percentage of biofuels (including, ethanol, biodiesel, and other biomass) blended into the U.S. fuel pool (gasoline and diesel) will increase and slowly grow across the entire projection period. In the High Oil Price case, the share of biofuels consumed in the United States rises to a greater percentage as higher prices for gasoline and diesel make biofuels more competitive. The share of biofuels in the Low Oil Price case remains relatively unchanged when compared with the Reference case because of regulations like those previously mentioned. For example, the LCFS encourages the use of biomass-based diesel because renewable diesel has one of the lowest carbon intensities of the approved pathways for LCFS compliance.

Individual biofuels supply

Biomass-based diesel, for the most part, tracks overall diesel demand. Biomass-based diesel is supported by policy including the renewed biodiesel mixture tax credit, and so it is likely to continue to gain market share through 2050. EIA projects diesel demand in the Reference case to almost return to pre-COVID levels in 2021, but never quite reach 2019’s peak. EIA expects biodiesel to grow slightly, maintaining a steady level of production through 2050.

Several new renewable diesel plants have been announced this year, both domestically and overseas. A few domestic refineries have shuttered to convert to renewable diesel production, or they have made plans to do so in the near future, contributing to projected increases in renewable diesel supply.

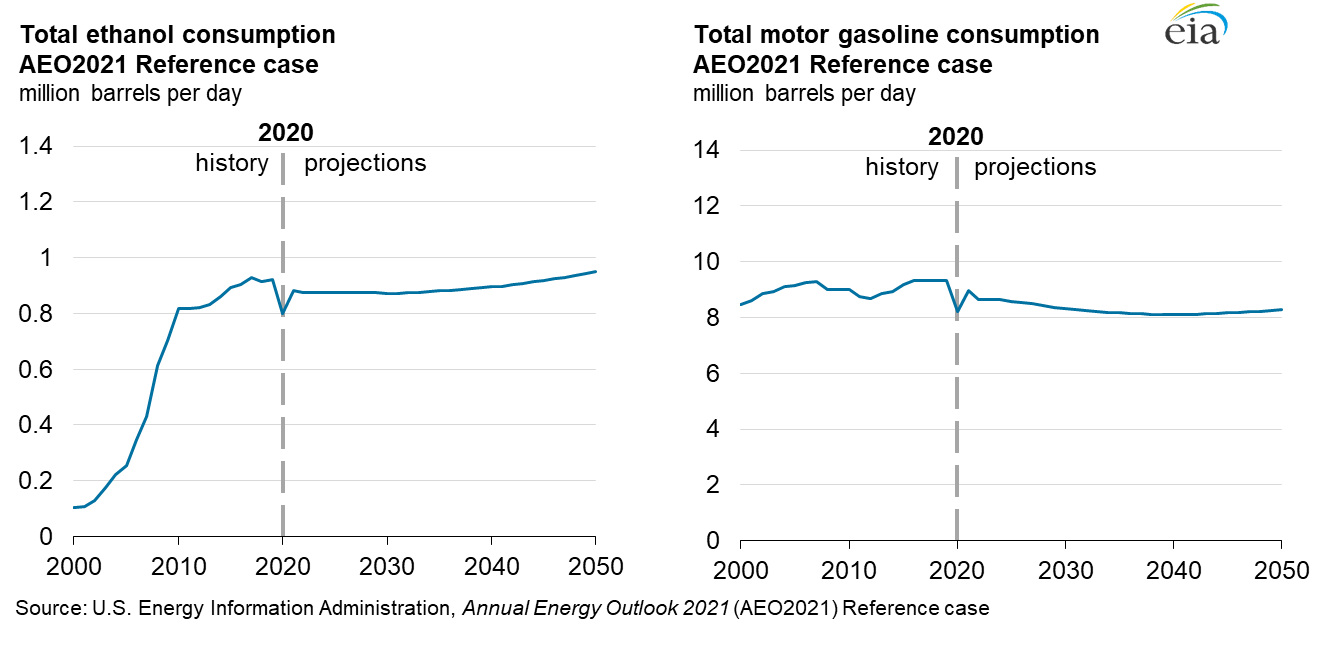

For ethanol, because almost all finished motor gasoline sold in the United States is blended with 10% ethanol (E10), reductions in gasoline demand have driven similar decreases in fuel ethanol demand, and, correspondingly, fuel ethanol production. Consumption of both ethanol and gasoline in 2020 have dropped by more than 10%, and both return in 2021 to almost reach 2019 levels at a similar pace. After this near-term return to 2019 levels, motor gasoline and diesel follow a pattern of general decrease, never fully returning to pre-COVID levels. On the other hand, ethanol does return to pre-COVID levels in the later years of the projection period, steadily growing through 2050 because of higher ethanol blends making their way into the on-road transportation pool.

Regulations support biofuels growth in the domestic on-road fuel mix.

-

Additional information:

-

Previous Editions of the AEO

-

Documentation and Assumptions