Released: April 30, 2014

Next Release: May 7, 2014

Domestic crude makes up half of U.S. East Coast refinery receipts in January 2014

Receipts of domestic crude oil at East Coast (PADD 1) refineries in January were approximately equal to receipts of foreign crude oil (Figure 1), reflecting a very significant change from recent experience. In January 2013, domestic crude oil was only 18% of total PADD 1 crude receipts, and in January 2012 domestic crude accounted for just 5% of PADD 1 receipts.

Rising U.S. crude oil production in the Bakken formation in North Dakota combined with the expansion of crude-by-rail infrastructure, which has facilitated movement of Bakken crude to PADD 1, have contributed to the increase in domestic crude oil supply to East Coast refineries.

Bakken crude oil is a good fit for most East Coast refineries, which generally favor a light sweet crude slate. As previously discussed in TWIP, there has been substantial investment in crude-by-rail infrastructure on the East Coast to accommodate receipts of Bakken crude at PADD 1 refineries and many crude-by-rail unloading facilities are now operational. Merchant terminal operators Global Partners LP and Buckeye Partners LP own storage terminals in Albany, New York, into which crude is delivered by rail and from which crude is shipped out by barge, down the Hudson River to refineries in New York Harbor and Philadelphia. PBF Energy Inc., which owns and operates two refineries on the East Coast, in Delaware City, Delaware, and Paulsboro, New Jersey, built a crude-by-rail unloading facility at its Delaware City refinery that has an estimated capacity of 120,000 barrels per day (bbl/d). Additionally, Sunoco Logistics owns a 40,000-bbl/d rail unloading facility in New Jersey, near the Philadelphia refining center.

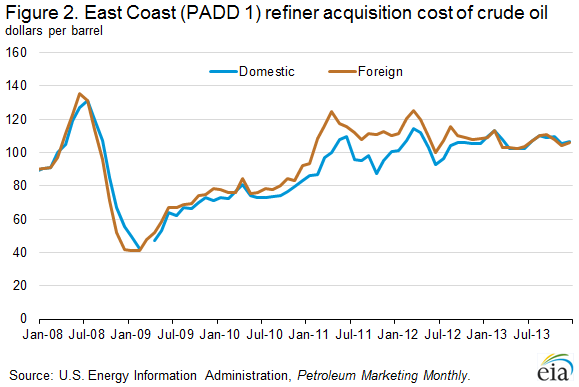

The lower cost of Bakken crude oil compared to imported crude oil has provided the impetus for investing in the crude-by-rail facilities that enable PADD 1 refiners to receive more domestic crude. The U.S. Energy Information Administration (EIA) collects data from refiners on the acquisition cost of both domestic and imported crude oil. The refiner acquisition cost of crude oil (RAC) is the weighted average cost of crude oil, including transportation and other fees paid by the refiner. From 2004 through 2008, East Coast RAC for domestic crude oil averaged $2.30 per barrel (bbl) more than for imported crude oil and was higher than imported RAC in 80% of months during that 5-year range. Since 2009, the opposite has been true. Domestic RAC has averaged $5.80/bbl below imported RAC. As the discount for domestic RAC increased to nearly $15/bbl in 2011, reflecting the changing relationship of U.S. and global crude oil prices, investment in rail unloading facilities increased. In 2012 the domestic RAC discount narrowed to less than $8/bbl and in 2013 domestic and imported RACs converged as the cost to acquire and move Bakken crude oil to the East Coast reached parity with the cost to import waterborne crude oil from the Atlantic Basin.

Although EIA does not collect monthly crude-by-rail statistics, it is possible to estimate crude-by-rail movements to PADD 1 by subtracting regional crude production and PADD-to-PADD crude oil movements via pipeline, tanker, and barge from the region's total domestic crude receipts. This calculation indicates that East Coast refinery receipts of domestic crude oil by rail were roughly 400,000 bbl/d in January and February 2014.

Total East Coast receipts of domestic crude oil have increased significantly in recent years. After averaging less than 80,000 bbl/d in 2012, PADD 1 domestic crude receipts rose to more than 290,000 bbl/d in 2013 and reached nearly 490,000 bbl/d in January 2014. Production in PADD 1 is limited, having averaged 31,000 bbl/d in 2013 and in January 2014. Crude oil movements from PADDs 2 (Midwest) and 3 (Gulf Coast) to PADD 1 via pipeline, tanker, and barge averaged less than 50,000 bbl/d in 2013 and were just under 40,000 bbl/d in January 2014. Because PADD 1 refinery receipts of domestic crude oil have consistently exceeded the sum of regional production and pipeline and marine movements from adjacent PADDs, it suggests that crude oil is entering the area by modes of transportation for which EIA does not collect data, primarily rail.

As East Coast refineries have increased receipts of domestic crude oil, imports to the region have steadily declined. East Coast imports of crude oil, which averaged 1.1 million bbl/d from 2008 to 2012, reached a record low of 775,000 bbl/d in 2013 and were just 524,000 bbl/d in January 2014.

Access to Bakken crude oil has provided PADD 1 refiners with crude selection flexibility, but refinery crude slates will continue to be a function of relative crude prices. In February 2014 (the latest month for which data are available), East Coast receipts of imported crude oil were slightly higher than domestic receipts, suggesting that refiners in the region can react to price movements in their crude sourcing decision.

Gasoline and diesel fuel prices increase

The U.S. average retail gasoline price increased three cents this week to $3.71 per gallon as of April 28, 2014, 19 cents more than the same time last year. The West Coast price rose five cents to $4.07 per gallon, while the East Coast and Rocky Mountain prices both increased four cents, to $3.71 per gallon and $3.48 per gallon respectively. The Midwest price rose two cents to $3.66 per gallon, and Gulf Coast prices were unchanged at $3.49 per gallon.

The U.S. average diesel fuel price rose by less than a penny to $3.98 per gallon, 12 cents more than the same time last year. The West Coast price increased three cents to $4.06 per gallon. The Rocky Mountain price rose by less than a penny to remain at $3.98 per gallon, while Gulf Coast and Midwest prices remained flat, at $3.82 per gallon and $3.95 per gallon respectively. Prices on the East Coast showed the only decline, falling half a cent to remain at $4.07 per gallon.

Propane inventories gain

U.S. propane stocks increased by 2.0 million barrels last week to 31.5 million barrels as of April 25, 2014, 8.9 million barrels (22.1%) lower than a year ago. Midwest and Gulf Coast inventories both increased by 0.8 million barrels. East Coast inventories increased by 0.4 million barrels, while Rocky Mountain/West Coast inventories remained unchanged. Propylene non-fuel-use inventories represented 10.1% of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

| Retail Data | Change From Last | Retail Data | Change From Last | ||||

| 04/28/14 | Week | Year | 04/28/14 | Week | Year | ||

| Gasoline | 3.713 | Diesel Fuel | 3.975 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Change From Last | Stocks Data | Change From Last | ||||

| 04/25/14 | Week | Year | 04/25/14 | Week | Year | ||

| Crude Oil | 399.4 | Distillate | 114.4 | ||||

| Gasoline | 211.6 | Propane | 31.537 | ||||