Released: September 26, 2012

Next Release: October 3, 2012

The Impact of U.S. Crude Oil Production on Gulf Coast Crude Imports

Increased production of U.S. domestic crude oil, particularly light sweet crude from tight oil formations in Texas and North Dakota, has been replacing imports of foreign light crude oil processed by U.S. Gulf Coast refineries. With Gulf Coast imports of heavier crude oil remaining steady, this shift in light crude supply from imports to domestic production has changed the average quality of crude oil imported into the U.S. Gulf Coast (PADD 3).

One of the primary characteristics that distinguishes different grades of crude oil is density, or how light or heavy the oil is. Crude oil density is typically measured as American Petroleum Institute (API) gravity, which is a scale expressing the specific gravity, or density, of liquid petroleum products in degrees; the higher the API gravity, the lighter the crude oil.

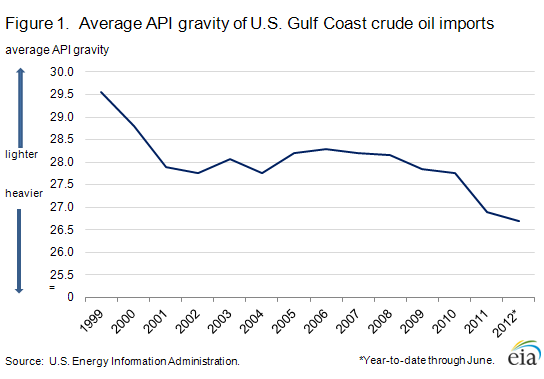

Since 2007, as domestic production of light sweet crude has increased, overall crude imports have fallen and become, on average, heavier. The average API gravity of crude imports processed in PADD 3 has dropped from more than 28Ḟ API to less than 27Ḟ API (Figure 1). This move to a higher percentage of heavier oil imports accelerated in 2011 when volumes of domestic light sweet crude oil production increased significantly, reducing the need for imports. Going forward, the growing production of domestic light crude may strain the capability of refineries to balance crude slates by reducing light crude imports and may put downward pressure on light crude prices on the U.S. Gulf Coast. Normally, light crude warrants a premium over heavier crude.

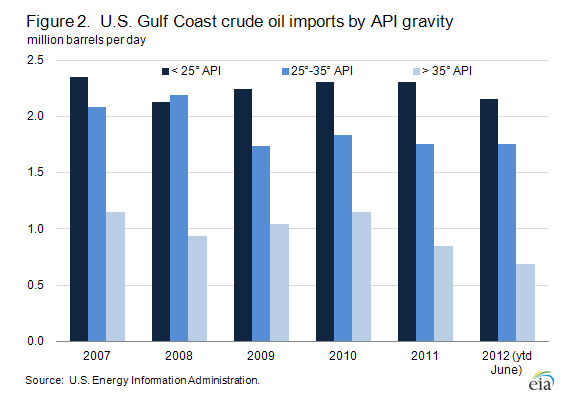

The volume of imported light crude oil (API gravity greater than 35Ḟ) (Figure 2) has decreased since 2010 to make room for the increasing volumes of light crudes from Eagle Ford (Texas) and Bakken (North Dakota) tight oil plays as well as for additional light sweet crude moving down the Seaway pipeline from Cushing, Oklahoma. While the absolute volume of imported heavy crude oil (API gravity less than 25Ḟ) has decreased since 2010 as well, the volume of heavy crude imports as a percentage of total PADD 3 imports has increased from 44 percent in 2010 to 47 percent in 2012.

The increased light sweet crude oil production from the Eagle Ford and Bakken fields has primarily displaced foreign light crudes from Africa. In total, light crude imports processed in PADD 3 have decreased to less than 0.7 million barrels per day (bbl/d) for the first half of 2012 from an average of 1.2 million bbl/d in 2010 (lowering the light crude imports to PADD 3 to 15 percent from 22 percent). To maintain a balanced crude slate with increased light crude availability, refiners have reduced imports of light crude and replaced them with domestic production. Imports of heavy crude processed in PADD 3 have continued as much of the heavy crude is either under long-term contract, is processed in equity refineries, or is needed to blend with domestic light crudes to balance the refinery crude slate.

The availability of domestic light crude to U.S. Gulf Coast refineries is expected to continue increasing as pipeline expansions allow more crude to move to the U.S. Gulf Coast. This increased light crude supply could exert downward pressure on Gulf Coast light crude prices.

Light crude generally contains less sulfur than heavier crudes and is easier to process. As a result, it is normally priced at a premium to heavier crude oils. However, processing large amounts of light low-sulfur crude can unbalance refinery processing units. Refineries on the U.S. Gulf Coast in particular are designed to process heavy crude oils. Catalytic crackers, hydrocrackers, and coking units convert the very heavy compounds in the crude oil into lighter and more valuable products. Processing lighter crude oil could underload the cracking units that handle the heavier components and overload the units that process the lighter components, causing refineries to operate less economically than they would with a more balanced crude slate. To process more light sweet crude, PADD 3 refiners would need to readjust refinery crude runs, revamp refinery equipment to run a higher percent of light crude, or reduce the use of heavy crude upgrading equipment, which may have adverse impacts on operations. Each of these alternatives carries a cost and, as a result, refiners may not be willing to pay as much for light crude (compared to heavy crude), and light crude prices could decline.

Gasoline and diesel fuel prices fall for the first time in 12 weeks

The U.S. average retail price of regular gasoline decreased five cents last week to $3.83 per gallon, 32 cents per gallon higher than last year at this time. Prices decreased in all regions of the Nation except the Rocky Mountains, where the price was up less than a penny to remain at $3.77 per gallon. The West Coast price decreased less than a penny to remain at $4.07 per gallon. The largest decrease came in the Midwest, where the price is $3.81 per gallon, down eight cents from last week. The Gulf Coast price decreased six cents to $3.60 per gallon, while the East Coast price dropped a nickel to $3.83 per gallon.

The national average diesel fuel price decreased a nickel to $4.09 per gallon, 30 cents per gallon higher than last year at this time. The largest decrease came on the West Coast, where the price is down eight cents to $4.32 per gallon. The Midwest price decreased six cents to $4.02 per gallon. The prices in the East Coast, Gulf Coast, and Rocky Mountain regions all decreased three cents to $4.09 per gallon, $4.00 per gallon, and $4.23 per gallon, respectively.

Propane stocks edge up slightly

Inventories of propane showed signs of leveling off last week, as the winter build season nears its end. Total U.S. inventories grew by 0.3 million barrels to end at 74.3 million barrels, 18 million barrels (32 percent) higher than a year ago. Midwest regional stocks were up by 0.3 million barrels, and East Coast stocks added 0.1 million barrels. Gulf Coast inventories dropped by 0.2 million barrels, and Rocky Mountain/West Coast regional stocks were up slightly. Propylene non-fuel-use inventories represented 6.1 percent of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

| Retail Data | Change From Last | Retail Data | Change From Last | ||||

| 09/24/12 | Week | Year | 09/24/12 | Week | Year | ||

| Gasoline | 3.826 | Diesel Fuel | 4.086 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Change From Last | Stocks Data | Change From Last | ||||

| 09/21/12 | Week | Year | 09/21/12 | Week | Year | ||

| Crude Oil | 365.2 | Distillate | 127.7 | ||||

| Gasoline | 195.8 | Propane | 74.290 | ||||