In the News:

The United States became the world’s largest LNG exporter in the first half of 2022

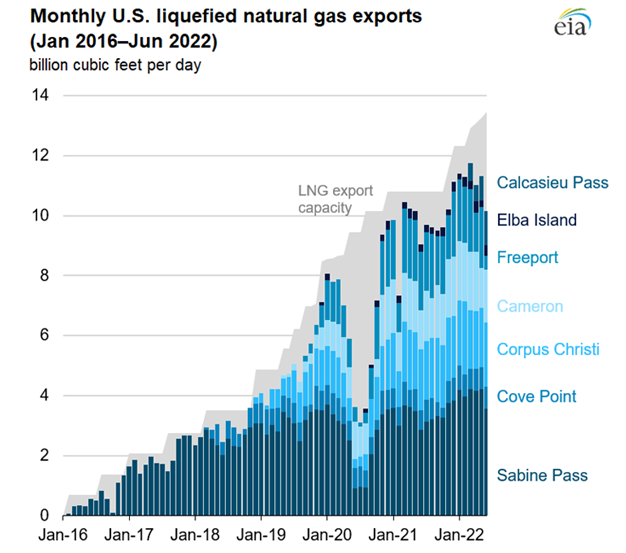

The United States became the world’s largest liquefied natural gas (LNG) exporter during the first half of 2022, according to data from CEDIGAZ. Compared with the second half of 2021, U.S. LNG exports increased by 12% in the first half of 2022, averaging 11.2 billion cubic feet per day (Bcf/d). U.S. LNG exports continued to grow for three reasons—increased LNG export capacity, increased international natural gas and LNG prices, and increased global demand, particularly in Europe.

According to our estimates, installed U.S. LNG export capacity has expanded by 1.9 Bcf/d nominal (2.1 Bcf/d peak) since November 2021. The capacity additions included a sixth train at the Sabine Pass LNG, 18 new mid-scale liquefaction trains at the Calcasieu Pass LNG, and increased LNG production capacity at Sabine Pass and Corpus Christi LNG facilities. As of July 2022, we estimate that U.S. LNG liquefaction capacity averaged 11.4 Bcf/d (13.6 Bcf/d peak), increasing to 13.9 Bcf/d peak capacity once all LNG trains at the new Calcasieu Pass LNG achieve full production.

International natural gas and LNG prices hit record highs in the last quarter of 2021 and first half of 2022. Prices at the Title Transfer Facility (TTF) in the Netherlands have been trading at record highs since October 2021. TTF prices averaged $30.94 per million British thermal units (MMBtu) during the first half of 2022. LNG spot prices in Asia have also been high, averaging $29.50/MMBtu during the same period.

Since the end of last year, countries in Europe have increased imports of LNG to compensate for lower pipeline imports from Russia and to fill historically low natural gas storage inventories. LNG imports into the EU and UK increased by 63% during the first half of 2022 to average 14.8 Bcf/d.

Most U.S. LNG exports went to the EU and the UK during the first five months of this year, accounting for 64%, or 7.3 Bcf/d, of the total U.S. LNG exports. Including Turkey, U.S. LNG exports to Europe accounted for 71% (8.1 Bcf/d) of the total exports. Similar to 2021, the United States accounted for most of EU and UK imports during the first half of the year, providing 47% of the 14.8 Bcf/d total LNG imports, followed by Qatar at 15%, Russia at 14%, and six African countries combined at 19%.

In June, the United States exported 11% less LNG than the 11.4 Bcf/d average exports during the first five months of 2022, mainly as a result of an unplanned outage at the Freeport LNG export facility. Freeport LNG is expected to resume partial liquefaction operations in early October 2022.

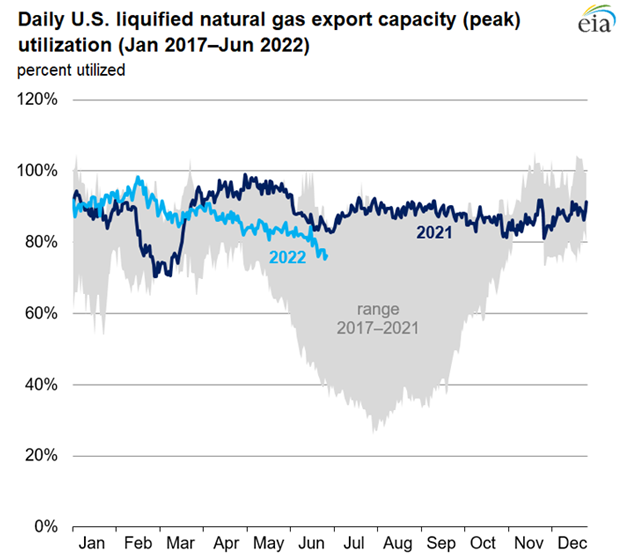

Utilization of the peak capacity at the seven U.S. LNG export facilities averaged 87% during the first half of 2022, mainly before the Freeport LNG outage, which is similar to the utilization on average during 2021.

Market Highlights:

(For the week ending Wednesday, July 27, 2022)Prices

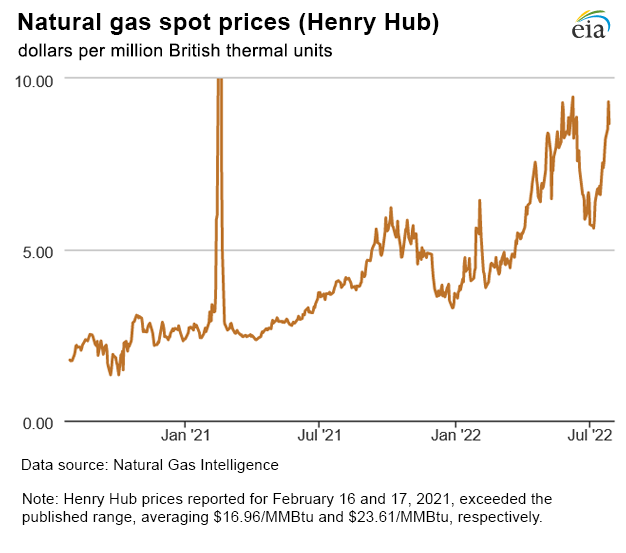

- Henry Hub spot price: The Henry Hub spot price rose $1.12 from $7.56 per million British thermal units (MMBtu) last Wednesday to $8.68/MMBtu yesterday.

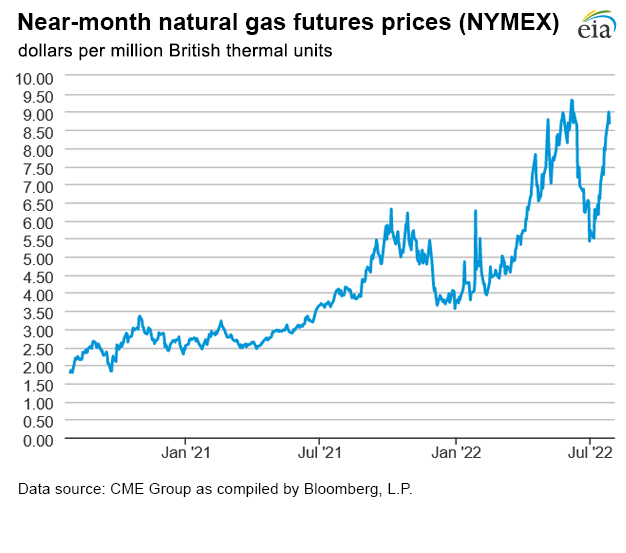

- Henry Hub futures prices: The August 2022 NYMEX contract expired yesterday at $8.687/MMBtu, up 68 cents from last Wednesday. The September 2022 NYMEX contract price increased to $8.554/MMBtu, up 66 cents from last Wednesday to yesterday. The price of the 12-month strip averaging September 2022 through August 2023 futures contracts climbed 35 cents to $6.947/MMBtu.

- Select regional spot prices: Natural gas spot prices rose at most locations this report week (Wednesday, July 20 to Wednesday, July 27). Increases at major pricing hubs ranged from 28 cents at SoCal Citygate in Southern California to $1.15 at PG&E Citygate.

- In the Northeast, at the Algonquin Citygate, which serves Boston-area consumers, the price went down $15.66 from $23.97/MMBtu last Wednesday to $8.31/MMBtu yesterday. This decline follows the week-over-week increase in price of $17.86 reported last week. Last week’s price of $23.97/MMBtu was the highest since January 28, 2022, and the highest July price in at least the last 20 years. At the Transcontinental Pipeline Zone 6 trading point for New York City, the price decreased 20 cents from $8.28/MMBtu last Wednesday to $8.08/MMBtu yesterday. High Algonquin Citygate prices this report week reflected elevated temperatures in New England. Temperatures in the Boston Area averaged above 80°F for most of the week, more than 7°F above normal. In the New York City Area, the daily high temperature reached a record 95°F two consecutive days this week, resulting in increased natural gas consumption in the electric power sector to meet air-conditioning demand. Consumption in the electric power sector increased by 10%, or 0.1 billion cubic feet per day (Bcf/d), in New England and by 9%, or 0.3 Bcf/d, in the New York and New Jersey area, according to data from PointLogic.

- In the Appalachia producing region, the Tennessee Zone 4 Marcellus spot price increased 87 cents from $6.91/MMBtu last Wednesday to $7.78/MMBtu yesterday. The price at Eastern Gas South in southwest Pennsylvania rose 95 cents from $6.87/MMBtu last Wednesday to $7.82/MMBtu yesterday. On July 13, Kinder Morgan, operator of the Tennessee Gas Pipeline, announced force majeure on Line 1 near Clermont, Pennsylvania, in McKean County that remains in effect. The reduction in operating pressure could affect estimated available capacity on that segment of Line 1 by as much as 235 million cubic feet per day (MMcf/d).

- In the Pacific Northwest, the price at Sumas on the Canada-Washington border rose $1.07 from $6.88/MMBtu last Wednesday to $7.95/MMBtu yesterday. Although the volume of natural gas consumed in the electric power sector in the Pacific Northwest is small relative to other regions, consumption increased 55%, or 0.3 Bcf/d, this week as result of warmer-than-normal temperatures. In the Seattle-Tacoma area, the daily high temperature reached a record 94°F on Tuesday.

- The price at PG&E Citygate in Northern California rose $1.15, up from $8.49/MMBtu last Wednesday to $9.64/MMBtu yesterday, following price increases in the Northwest. The price at the Malin, Oregon hub, the northern delivery point into the PG&E system, rose by 87 cents, from $7.49/MMBtu last Wednesday to $8.36/MMBtu yesterday. The price at SoCal Citygate in Southern California increased 28 cents from $8.78/MMBtu last Wednesday to $9.06/MMBtu yesterday. Natural gas consumption in the electric power sector decreased by 11%, or 0.3 Bcf/d, according to data from PointLogic. After falling to 42% of power generation capacity, use of natural gas in power generation relative to other fuels returned to 53% of generation capacity by Tuesday.

- International futures prices: International natural gas futures prices increased this report week. According to Bloomberg Finance, L.P., weekly average futures prices for liquefied natural gas (LNG) cargoes in East Asia increased $1.85 to a weekly average of $39.96/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas spot market in Europe, increased $6.04 to a weekly average of $53.64/MMBtu, the second-highest weekly average on record behind the $61.08/MMBtu weekly average reported for early March, after Russia’s full-scale invasion of Ukraine.

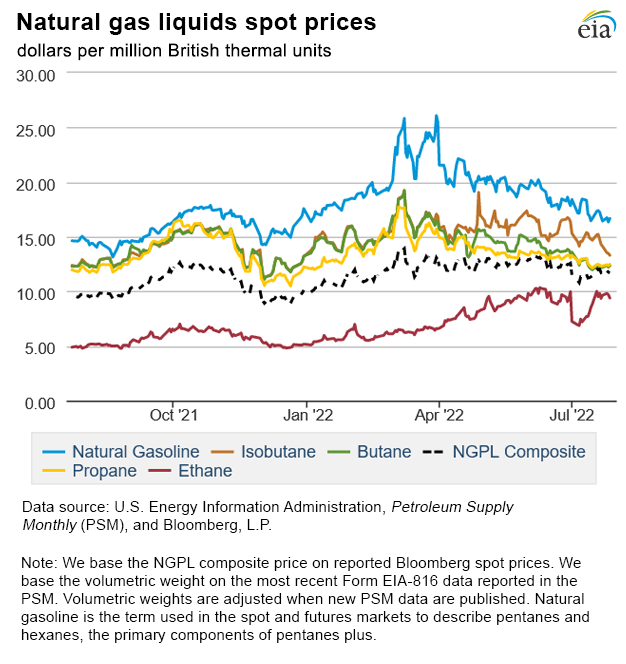

- Natural gas plant liquids prices: The natural gas plant liquids composite price at Mont Belvieu, Texas, fell by 2 cents/MMBtu, averaging $11.76/MMBtu for the week ending July 27. The ethane price rose 3% to $9.58/MMBtu. Natural gas prices at the Houston Ship Channel rose 19%, narrowing the ethane premium to natural gas by 43%. Although the price of ethylene rose 2%, the increase in ethane prices narrowed the ethylene to ethane spread by 4%. The Brent crude oil price fell 4%, pulling down the prices of heavier NGPLs. The natural gasoline price fell 2%, while the isobutane price fell 8%. Normal butane and propane prices remained relatively unchanged. The propane discount to crude oil narrowed by 13%.

Daily spot prices by region are available on the EIA website.

Supply and Demand

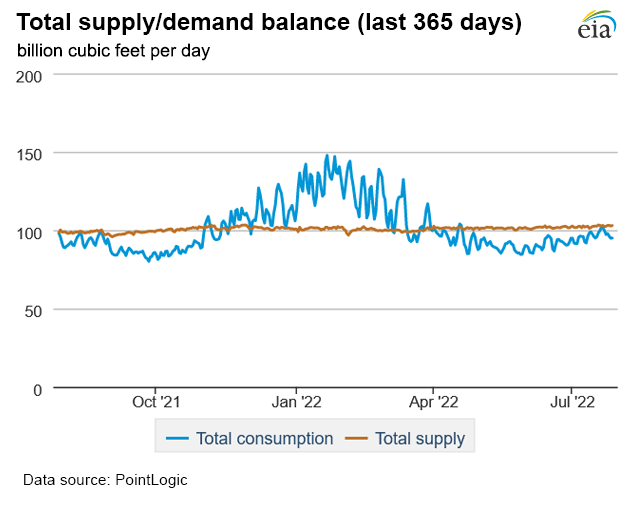

- Supply: According to data from PointLogic, the average total supply of natural gas rose slightly this report week, averaging 102.8 Bcf/d. Dry natural gas production grew by 0.1% (0.1 Bcf/d) compared with the previous report week, offset by a decline in average net imports from Canada, which fell by 1.1% (0.1 Bcf/d) from last week.

- Demand: Total U.S. consumption of natural gas rose by 0.2% (0.1 Bcf/d) compared with the previous report week, according to data from PointLogic. Weather remained hot throughout most of the United States. Natural gas consumed for power generation declined by 0.1% (0.1 Bcf/d) week over week and industrial sector consumption decreased by 0.3% (0.1 Bcf/d). In the residential and commercial sectors, consumption increased by 2.6% (0.2 Bcf/d). Natural gas exports to Mexico decreased 5.6% (0.3 Bcf/d). Natural gas deliveries to U.S. LNG export facilities (LNG pipeline receipts) averaged 10.8 Bcf/d, or 0.1 Bcf/d lower than last week.

Liquefied Natural Gas (LNG)

- Pipeline receipts: Natural gas deliveries to LNG export terminals in South Louisiana decreased by 2%, or 0.2 Bcf/d, this report week, while deliveries to most of the other export terminals were effectively flat. Cheniere, operator of the Creole Trail Pipeline, reported deliveries to the Sabine Pass LNG export terminal declined by approximately 0.3 Bcf/d. An increase of 175 MMcf/d in deliveries to the Calcasieu Pass terminal, also in South Louisiana, as well as minor increases to other terminals, somewhat offset this decline, resulting in an overall decline of 0.1 Bcf/d in feed gas this report week.

- Vessels departing U.S. ports: Eighteen LNG vessels (seven from Sabine Pass, four from Corpus Christi, three from Cameron, two from Calcasieu Pass, and one each from Cove Point and Elba Island) with a combined LNG-carrying capacity of 67 Bcf departed the United States between July 21 and July 27 according to shipping data provided by Bloomberg Finance, L.P.

- LNG export terminals: Venture Global Calcasieu Pass, LLC, received approval from the Federal Energy Regulatory Commission to introduce hazardous fluids to Liquefaction Block 9. This permit is among the last ones needed in the commissioning process for the terminal to operate all 18 liquefaction trains.

Rig Count

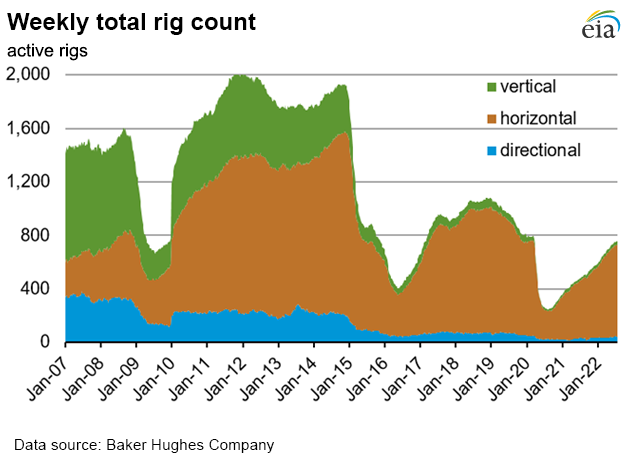

- According to Baker Hughes, for the week ending Tuesday, July 19, the natural gas rig count increased by 2 rigs from a week ago to 155 rigs. The Permian added one rig, and one rig was added in an unspecified producing region. The number of oil-directed rigs was unchanged at 599 rigs this week. The total rig count now stands at 758 rigs, which is 267 rigs more than the same week last year

Storage

- The net injections into storage totaled 15 Bcf for the week ending July 22, compared with the five-year (2017–2021) average net injections of 32 Bcf and last year's net injections of 38 Bcf during the same week. Working natural gas stocks totaled 2,416 Bcf, which is 12%, or 345 Bcf, lower than the five-year average and 11%, or 293 Bcf, lower than last year at this time.

- According to The Desk survey of natural gas analysts, estimates of the weekly net change to working natural gas stocks ranged from net injections of 11 Bcf to 28 Bcf, with a median estimate of 19 Bcf.

- The average rate of injections into storage is 6% lower than the five-year average so far in the refill season (April through October). If the rate of injections into storage matched the five-year average of 8.7 Bcf/d for the remainder of the refill season, the total inventory would be 3,300 Bcf on October 31, which is 345 Bcf lower than the five-year average of 3,645 Bcf for that time of year.

See also:

Data source: U.S. Department of Energy LNG Reports and U.S. Energy Information Administration Liquefaction Capacity Table

Data source: U.S. Department of Energy LNG Reports and U.S. Energy Information Administration Liquefaction Capacity TableNote: June 2022 LNG exports are EIA estimates based on tanker shipping data. LNG export capacity is an estimated peak LNG production capacity of all operational U.S. LNG facilities.

Data source: U.S. Department of Energy LNG Reports and U.S. Energy Information Administration Liquefaction Capacity Table

Data source: U.S. Department of Energy LNG Reports and U.S. Energy Information Administration Liquefaction Capacity TableNote: Daily utilization of U.S. liquefied natural gas (LNG) export capacity is calculated as a 30-day moving average.

| Spot Prices ($/MMBtu) | Thu, 21-Jul |

Fri, 22-Jul |

Mon, 25-Jul |

Tue, 26-Jul |

Wed, 27-Jul |

|---|---|---|---|---|---|

| Henry Hub |

7.95 |

8.25 |

8.53 |

9.32 |

8.68 |

| New York |

9.37 |

8.62 |

7.88 |

8.42 |

8.08 |

| Chicago |

7.81 |

8.10 |

8.29 |

8.75 |

8.41 |

| Cal. Comp. Avg.* |

8.51 |

8.61 |

9.00 |

9.57 |

8.95 |

| Futures ($/MMBtu) | |||||

| August contract | 7.932 |

8.299 |

8.727 |

8.993 |

8.687 |

| September contract |

7.815 |

8.195 |

8.571 |

8.825 |

8.554 |

| Data source: Natural Gas Intelligence and CME Group as compiled by Bloomberg, L.P. *Avg. of NGI's reported prices for: Malin, PG&E Citygate, and Southern California Border Avg. |

|||||

| U.S. natural gas supply - Gas Week: (7/21/22 - 7/27/22) | |||

|---|---|---|---|

Average daily values (billion cubic feet) |

|||

this week |

last week |

last year |

|

| Marketed production | 108.9 |

108.7 |

105.8 |

| Dry production | 96.7 |

96.6 |

93.2 |

| Net Canada imports | 6.0 |

6.0 |

5.2 |

| LNG pipeline deliveries | 0.1 |

0.1 |

0.1 |

| Total supply | 102.8 |

102.7 |

98.4 |

|

Data source: PointLogic | |||

| U.S. natural gas consumption - Gas Week: (7/21/22 - 7/27/22) | |||

|---|---|---|---|

Average daily values (billion cubic feet) |

|||

this week |

last week |

last year |

|

| U.S. consumption | 74.1 |

74.0 |

70.4 |

| Power | 43.3 |

43.4 |

40.8 |

| Industrial | 21.0 |

21.0 |

21.2 |

| Residential/commercial | 9.8 |

9.6 |

8.4 |

| Mexico exports | 5.8 |

6.2 |

6.4 |

| Pipeline fuel use/losses | 6.8 |

6.7 |

6.4 |

| LNG pipeline receipts | 10.8 |

10.9 |

10.6 |

| Total demand | 97.5 |

97.8 |

93.7 |

|

Data source: PointLogic | |||

| Rigs | |||

|---|---|---|---|

Tue, July 19, 2022 |

Change from |

||

last week |

last year |

||

| Oil rigs | 599 |

0.0% |

54.8% |

| Natural gas rigs | 155 |

1.3% |

49.0% |

| Note: Excludes any miscellaneous rigs | |||

| Rig numbers by type | |||

|---|---|---|---|

Tue, July 19, 2022 |

Change from |

||

last week |

last year |

||

| Vertical | 31 |

3.3% |

63.2% |

| Horizontal | 687 |

0.1% |

56.5% |

| Directional | 40 |

0.0% |

21.2% |

| Data source: Baker Hughes Company | |||

| Working gas in underground storage | ||||

|---|---|---|---|---|

Stocks billion cubic feet (Bcf) |

||||

| Region | 2022-07-22 |

2022-07-15 |

change |

|

| East | 532 |

521 |

11 |

|

| Midwest | 625 |

608 |

17 |

|

| Mountain | 144 |

144 |

0 |

|

| Pacific | 253 |

253 |

0 |

|

| South Central | 862 |

874 |

-12 |

|

| Total | 2,416 |

2,401 |

15 |

|

| Data source: U.S. Energy Information Administration Form EIA-912, Weekly Underground Natural Gas Storage Report | ||||

| Working gas in underground storage | |||||

|---|---|---|---|---|---|

Historical comparisons |

|||||

Year ago (7/22/21) |

5-year average (2017-2021) |

||||

| Region | Stocks (Bcf) |

% change |

Stocks (Bcf) |

% change |

|

| East | 580 |

-8.3 |

606 |

-12.2 |

|

| Midwest | 699 |

-10.6 |

690 |

-9.4 |

|

| Mountain | 184 |

-21.7 |

175 |

-17.7 |

|

| Pacific | 246 |

2.8 |

275 |

-8.0 |

|

| South Central | 999 |

-13.7 |

1,015 |

-15.1 |

|

| Total | 2,709 |

-10.8 |

2,761 |

-12.5 |

|

| Data source: U.S. Energy Information Administration Form EIA-912, Weekly Underground Natural Gas Storage Report | |||||

| Temperature – heating & cooling degree days (week ending Jul 21) | ||||||||

|---|---|---|---|---|---|---|---|---|

HDDs |

CDDs |

|||||||

| Region | Current total |

Deviation from normal |

Deviation from last year |

Current total |

Deviation from normal |

Deviation from last year |

||

| New England | 0 |

-1 |

0 |

69 |

26 |

8 |

||

| Middle Atlantic | 0 |

-1 |

0 |

81 |

23 |

6 |

||

| E N Central | 1 |

-1 |

0 |

68 |

11 |

16 |

||

| W N Central | 0 |

-3 |

0 |

92 |

20 |

33 |

||

| South Atlantic | 0 |

0 |

0 |

102 |

5 |

1 |

||

| E S Central | 0 |

0 |

0 |

105 |

10 |

17 |

||

| W S Central | 0 |

0 |

0 |

149 |

24 |

37 |

||

| Mountain | 0 |

-4 |

0 |

106 |

27 |

20 |

||

| Pacific | 1 |

-3 |

0 |

70 |

26 |

10 |

||

| United States | 0 |

-2 |

0 |

92 |

18 |

14 |

||

|

Data source: National Oceanic and Atmospheric Administration Note: HDDs=heating degree days; CDDs=cooling degree days | ||||||||

Average temperature (°F)

7-day mean ending Jul 21, 2022

Data source: National Oceanic and Atmospheric Administration

Deviation between average and normal temperature (°F)

7-day mean ending Jul 21, 2022

Data source: National Oceanic and Atmospheric Administration

{kind=link}