Overview (Wednesday, February 27, to Wednesday, March 5)

Released: March 6, 2008

Next release: March 13, 2008

·

Since Wednesday,

February 27, natural gas prices increased on both the spot and futures markets.

There were a few scattered exceptions to the increases, but these were mostly

confined to the Northeast.

·

The spot price

at the Henry Hub increased 16 cents per million Btu (MMBtu) or 1.7 percent on

the week, averaging $9.37 per MMBtu yesterday, the highest price since January

2006.

·

Boosted by

record-high crude oil prices and declining working gas in storage, the prices

of natural gas futures contracts increased on the week, reaching levels not

seen in the market in more than 2 years. The price of the futures contract for

April 2008 delivery increased 68 cents per MMBtu to $9.741.

·

Natural gas in

storage was 1,484 Bcf as of February 29, which is 4 percent above the 5-year

average.

·

The spot price

for West Texas Intermediate (WTI) crude oil increased $4.86 per barrel to a new

record-high price of $104.45 per barrel or $18.01 per MMBtu.

Cold weather that blanketed much of the

country, with the exception of the Northeast, as well as the high crude oil

prices, led to price increases at nearly all natural gas spot market locations.

Spot price increases in the Lower 48

States ranged mostly between 20 and 50 cents per MMBtu, although several

trading locations in the Rocky Mountains recorded increases of up to 62 cents

per MMBtu. As of yesterday, the average regional price in the Rockies was $8.69

per MMBtu, the lowest regional price in the Lower 48 States.

The Henry Hub spot price increased 16

cents on the week to $9.37 per MMBtu.

While the weekly price increase at the Henry Hub was comparatively low,

yesterday’s price was the highest for this location since January 3, 2006, when

the Henry Hub spot price reached $9.91 per MMBtu.

Warmer weather in the Northeast during

the report week led to spot prices that were significantly below prices on

Wednesday, February 27. In this

region, price decreases averaged $3 per MMBtu or 19 percent, although several

trading locations, including Algonquin, Iroquois, and Transco Zone 6 (both New

York and non-New York delivery), recorded price declines that exceeded $4 and

reached as high as $8.02 per MMBtu. Despite these sizeable decreases, 10 out of

13 locations in the Northeast traded at $10 or more per MMBtu yesterday, and

the Northeast had the highest regional spot prices in the Lower 48 States.

Boosted by rising crude oil prices and declining

working gas in storage, the NYMEX futures contract for April delivery at the

Henry Hub settled yesterday, March 5, at $9.741 per MMBtu, after increasing 68

cents or 7.5 percent on the week. Yesterday’s settlement price for the

April 2008 contract was the highest near-month settlement price since the

February 2006 contract settled at $10.197 per MMBtu on January 4, 2006. During

the first week of trading as the near-month contract, the price of the April

2008 contract increased in three out of five trading sessions.

Prices for contracts in the other

refill season months of 2008 increased across the board with the

May-through-October futures strip gaining about 65 cents per MMBtu, or about 7 percent

since last Wednesday. As of

yesterday, the price of the refill-season-contract strip (April-October) was

$9.871 per MMBtu. With storage levels likely to finish the current heating

season below last year’s levels, demand for gas for underground storage

injections between April and October is expected to exceed that of last year.

The current higher prices for future deliveries reflect the expected tightness

in the natural gas market over the next 6 months, which results from the

significant volume of natural gas that will be required for storage injection.

Recent Natural Gas Market Data

Working gas in storage decreased to 1,484 Bcf as of

Friday, February 29, according to the EIA Weekly

Natural Gas Storage Report (see Storage Figure). Storage inventories are currently 4.4 percent above

the 5-year average, but about 10 percent below last year’s storage level at

this time. The implied net withdrawal of 135 Bcf is 22 percent more than the

5-year average withdrawal of 111 Bcf and about 36 percent higher than last

year’s withdrawal of 99 Bcf. With the latest net withdrawal of 135 Bcf, this

year’s natural gas volume in storage already has dipped below last year’s low

of 1,511 Bcf, which was reported for the week ending March 23, 2007.

The East and Producing regions recorded net

withdrawals that were 24 and 64 percent, respectively, higher than the 5-year

average withdrawals for the week. The relatively large drawdowns

of gas reflect the impact of the unusually cold temperatures during the week,

which kept demand for heating relatively high.

For the week ending February 28, temperatures were 13.3 percent colder

than normal and about 10 percent colder than last year, according to degree-day

data published by the National Weather Service. All of the Census Divisions,

with the exception of the Mountain and Pacific Census Divisions, experienced

temperatures that were colder than normal (see Temperature Maps and Data). The Census Divisions with large

population centers that consume large volumes of natural gas for space heating,

such as the East North Central and Middle Atlantic, recorded temperatures that

were between 10 and 22 percent colder than normal.

Below-average net withdrawals of 7 Bcf occurred in

the West region as temperatures were at or warmer than normal. The relatively small withdrawal reduced the

difference between current and last year’s volumes in the region. However, as

of last Friday, the 189 Bcf being stored in the West region was still 11.7

percent below the 5-year average for the region.

Other Market Trends:

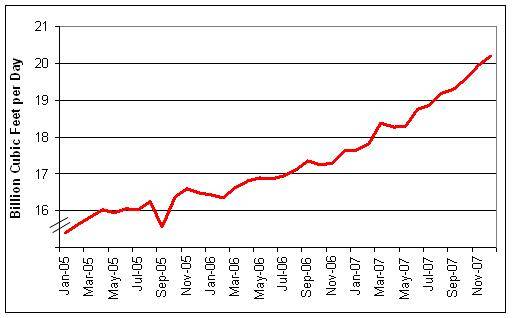

Gross Natural Gas Production in Texas

Exceeds 20 Bcf per Day. In December

2007 gross withdrawals of natural gas in Texas hit their highest production level

since the data series began in 1991. Gross withdrawals reached 20.2 Bcf per day

in December, which was about 14.5 percent higher than the year-ago production

volume of 17.6 Bcf per day. Texas recorded an 11.2-percent increase in annual

gross production in 2007 compared with 2006, reaching 6.9 Tcf (18.9 Bcf per

day) in 2007. Factors contributing to

the increased production include increased drilling activity and continued

success from unconventional resources. While the State is considered a mature

producing area, exploration and production of unconventional gas resources,

such as the Barnett Shale in northeastern Texas, play a major role in natural

gas production. Production from unconventional resources, including coalbed

methane, tight sands, and gas shales, make up the largest portion of production

in the onshore Lower 48 States. According to EIA’s Annual Energy Outlook 2008, unconventional resources are projected

to account for 8.73 Tcf or 57.5 percent of total Lower 48 onshore production in

2007.

Since

January 2005, Texas gross withdrawals have exhibited a generally increasing

trend, with the exception of a significant dip in September 2005 that resulted

from the production disruption associated with hurricanes Katrina and Rita. As

a result, State gross production fell to 15.6 Bcf per day in September 2005, a

4.1-percent decline from the preceding month’s level, but it returned to

pre-hurricane levels by October 2005 (16.4 Bcf per day). Texas annual gross

production totaled 5.8 Tcf (16.0 Bcf per day) in 2005, followed by 6.2 Tcf

(16.9 Bcf per day in 2006.

Drilling

activity in Texas increased during this time, when the average number of oil

and gas rigs drilling climbed 21 and 22 percent in 2005 and 2006,

respectively. The rate of increase in

rigs in Texas hit a peak in early 2007, from which it declined and then leveled

off during the final 8 months of the year.

The average rig count in Texas grew about 1 percent between 2006 and

2007. According to Baker Hughes, Incorporated, the weekly average number of

rigs drilling in Texas was 748 in 2007, which was on average 2 rigs more per

week than in 2006.

For

more information on the latest natural gas data, see the February 2008 edition

of the Natural Gas Monthly. Additional data on gross natural gas

production can be found in the Form EIA-914 Monthly Natural Gas Production Report.

EIA Releases Updated Report on Imports and Exports. The Energy

Information Administration (EIA) has released a special report titled U.S. Natural Gas

Imports and Exports: 2006, which examines recent trends in U.S.

international trade of natural gas. In 2006, when U.S. natural gas consumption

and prices decreased, international supplies of natural gas to the United

States also fell. The United States imported natural gas from six different

countries and exported natural gas to three countries. In 2006, net imports to the United States totaled 3,462 Bcf, a decrease of 150

Bcf, or 4.2 percent, from the previous year, and net U.S. exports to Mexico and

Japan declined by 5 Bcf. As in years past, the U.S. imports came

primarily via pipeline from Canada (85.8 percent of total imports). However, import volumes from Canada fell by

110 Bcf to 3,590 Bcf. The average price

for all U.S. imports declined to $6.72 per million British thermal units or

$6.88 per thousand cubic feet). Imports

of liquefied natural gas (LNG) declined 7.6 percent from the 2005 level to 584

Bcf. Although LNG imports declined

during 2006, the industry continued with plans to expand infrastructure in the

United States in anticipation of bringing LNG from a variety of countries.

The report includes extensive historical tables with natural gas import and

export data through 2006 for both pipeline and LNG trade.

EIA Releases Revised Annual Energy Outlook 2008. The Energy Information Administration (EIA)

on March 4 released a revised Annual Energy

Outlook 2008 (AEO2008) reference case. The revised analysis replaces the early

release version issued shortly before the December 2007 enactment of the Energy Independence and Security Act of 2007

(EISA2007) and includes the impact of that enactment. In the AEO2008 reference case, real

world crude oil prices (defined as the price of light, low-sulfur crude oil

delivered in Cushing, Oklahoma, in 2006 dollars) decline gradually from current

levels to $57 per barrel in 2016 ($68 per barrel in nominal dollars),

thereafter rising to $70 per barrel. The real wellhead price of natural gas (in

2006 dollars) is expected to decline from current levels through 2016, as new

supplies enter the market. After 2016, real natural gas prices rise to $6.56

per thousand cubic feet in 2030. The higher prices reflect an increase in

production costs and the higher oil prices.

Total consumption of

natural gas is projected to increase from 21.7 trillion cubic feet (Tcf) in 2006

to 23.9 Tcf in 2016, then decline to 22.7 Tcf in 2030. Under current laws and regulations, natural

gas is expected to lose market share to coal in the electric power sector as a

result of continued increase in natural gas prices in the latter half of the

projection and slower growth in electricity demand.

Total domestic natural gas

production, including supplemental natural gas supplies, increases from 18.6

Tcf in 2006 to a projected 20.1 Tcf in 2022 before declining to 19.6 Tcf in

2030. While onshore conventional production is expected to decline steadily,

lower-48 offshore production peaks in 2017. Lower-48 production of

unconventional natural gas, particularly gas from shale, is expected to be a

key contributor to growth in U.S. natural gas supplies, increasing from 8.5 Tcf

in 2006 to 9.5 Tcf in 2030. The Alaska natural gas pipeline is expected to be

completed in 2020, later than previously anticipated, because of delays in the

resolution of issues between Alaska’s State Government and industry participants.

Net pipeline imports of

natural gas in the AEO2008 reference case fall from 2.9 Tcf in 2006 to a

projected 0.3 Tcf in 2030, reflecting both resource depletion in Alberta and

Canada’s growing domestic demand. Total net imports of liquefied natural gas

(LNG) to the United States are expected to increase from 0.5 Tcf in 2006 to 2.8

Tcf in 2030. The future direction of the global LNG market, with many new

international players entering LNG markets and strong competition for available

supply, is one of the key uncertainties in the AEO2008 reference

case.

The complete AEO2008,

which EIA will release in April, includes a large number of alternative cases

intended to examine uncertainties surrounding the projections.

Natural Gas

Transportation Update:

·

Mississippi

River Transmission Corporation (MRT) issued a system protection warning (SPW)

March 4 and until further notice. The

warning was issued as a result of forecasted cold weather. During the SPW, MRT will not schedule volumes

that might result in a daily short position.

If actual deliveries exceed scheduled volumes, shippers may be required

to add supply or reduce their takes from MRT.

·

Trunkline Gas

Company announced that on March 4 and 5, it will be inspecting the Quicksand

Creek Lateral in southwestern Louisiana

for corrosion and defects, a procedure known as “pigging.” During that time,

four meters will be shut in.

·

Questar Pipeline

Company announced that it will be performing a required water washing of all

three units at its Oak Spring compressor station in Carbon County, Utah. To

facilitate the work, the main line 104 capacity will be reduced to 400,000

decatherms (Dth) per day for gas day March 18 and to 290,000 Dth per day for

March 19 and 20.

·

TransColorado

Pipeline between the TransColorado/REX Love Ranch interconnect and Greasewood

Compressor Station (Segment 180) in northwestern Colorado has been temporarily

shut in and isolated for emergency repairs. Consequently, some pipeline

interconnects have been shut in until further notice. TransColorado is working

with point operators and does not anticipate any impact to shippers.

{kind=link}

{kind=link}