Overview: Monday, December 10, 2001

Price surges on Monday and

Friday of last week overshadowed 3 straight days of decreases midweek, as

nearly every major market location showed Friday-to-Friday gains. At the Henry Hub, the spot price gained 36

cents from the previous Friday to end the week at $2.11 per million Btu

(MMBtu). On the futures market, in its

first full week of trading as the near-month contract, the price of the NYMEX

contract for January delivery at the Henry Hub declined $0.133 per MMBtu to

settle on Friday at $2.568. The

unseasonably warm temperatures that have blanketed nearly the entire country

east of the Rocky Mountains continued, with specific-day high-temperature

records being set at numerous locations in the Northeast, Midwest, and

Midcontinent (Temperature

Map)(Temperature

Deviation Map). On Thursday, the spot price

of West Texas Intermediate (WTI) crude oil fell nearly $1.00 per barrel, as the

Organization of Petroleum Exporting Countries (OPEC) announced that it would

delay an expected oil-production cut that it hopes will shore up sagging world

crude oil prices. For the week

(Friday-to-Friday), the WTI spot price fell $0.43 per barrel to $19.08, or

$3.29 per MMBtu.

Prices:

Spot prices rebounded last week on the strength of

strong increases on Monday and Friday.

Monday’s price surge was the larger of the two, with increases in

average spot prices ranging from 15 to over 80 cents per MMBtu at virtually

every price point tracked by Natural Gas Intelligence. Increases were greatest in the Rockies in

anticipation of Tuesday’s maintenance outage affecting supply into the Opal

(WY) hub. At the Henry Hub, the average spot price climbed 35 cents per MMBtu

to $2.10. With the lack of

weather-related swing demand, some market observers attributed the increases to

various participants coming out of bid week and into the new month with short

supply portfolios that needed to be covered.

Indeed, November’s spring-like temperatures experienced by most of the

nation persisted through the first week of December. The resulting weak demand reasserted itself in markets on Tuesday

through Thursday, sending cash prices steadily downward and more than offsetting

Monday’s gains at some locations.

However, National Weather Service forecasts for cooler, near-normal

temperatures over the weekend for the Northeast and Midwest reversed the

downward trend, sending prices up in a 20-40 cent range at most locations. California was the major exception, where

somewhat warmer temperatures and a PG&E high inventory operational flow

order (OFO) for the weekend had prices declining by a few cents to over a dime. By Friday, prices in most markets had

climbed back above $2 per MMBtu. For

the week, the spot prices for gas for delivery to New York and Chicago

citygates were $2.53 and $2.15, up $0.46 and $0.29 per MMBtu,

respectively. The PG&E citygate

price had dropped 2 cents to $2.42, while the average price for gas at the

Southern California border rose 17 cents to $2.36. Trading was also characterized by somewhat reduced within-day

volatility compared with the previous two weeks. At the Henry Hub, the spread between the low and high values for

daily spot prices ranged from $0.10 to $0.21 per MMBtu. Last week this spread ranged from $0.13 to

$0.40, and the week before, from $0.27 to $0.38.

Prices on the NYMEX futures market also were

affected early in the week by the continuing warm weather. The futures contract

settlement prices for January through March began the week with 3 consecutive

days of declines in the range of about 4 to 8 cents per MMBtu. Out-month contracts followed suit for the

most part, with somewhat smaller declines.

However, on Thursday, settlement prices got a slight boost, with

increases of about a nickel for contracts over the ensuing 12 months. From

Friday-to-Friday, the near-month contract declined $0.133 per MMBtu to end the

week at $2.568. On its first day of

trading as the near-month contract, the January contract fell $0.171 to $2.561

per MMBtu. In 6 days of trading since then, its cumulative price change has

been almost nil–as of Friday, its settlement price was a scant $0.007 higher

than its first settlement price as the near-month contract.

|

Spot Prices ($ per MMBTU)-Selected

Trading Centers |

Mon.

12/03 |

Tue. 12/04 |

Wed. 12/05 |

Thur. 12/06 |

Fri.

12/07 |

|

Henry Hub |

2.10 |

1.99 |

1.89 |

1.83 |

2.11 |

|

New York citygates |

2.50 |

2.30 |

2.16 |

2.13 |

2.53 |

|

Chicago citygates |

2.18 |

2.08 |

1.97 |

1.88 |

2.15 |

|

PG&E Citygates |

2.87 |

2.74 |

2.55 |

2.50 |

2.42 |

|

Southern California

Bdr. Average |

2.55 |

2.45 |

2.36 |

2.31 |

2.36 |

|

Futures (Daily

Settlement, $MMBTU) |

|

|

|

|

|

|

January Delivery |

2.634 |

2.563 |

2.491 |

2.565 |

2.568 |

|

February Delivery |

2.746 |

2.703 |

2.624 |

2.675 |

2.681 |

|

Source: NGI's

Daily Gas Price Index (http://intelligencepress.com) |

|||||

Storage:

Net withdrawals from storage totaled 16 Bcf for the week

ended November 30 according to the American Gas Association (AGA). This snapped an unprecedented run of more

than 3 weeks in a row of net storage additions this heating season. Net withdrawals in the West were 19 Bcf

compared with the 6-year average for the week of 5 Bcf. This unusually high drawdown equals a

reduction of nearly 4 percent of the region’s total working gas in storage and

is attributable to the colder than normal temperatures that prevailed in the

region during most of the week. Working

gas inventories in the East were unchanged, while the Producing region recorded

net injections of 3 Bcf. At 3,140 Bcf,

working gas in storage is nearly 14 percent greater than the 6-year average and

nearly as large as the 6-year high of 3,155 Bcf for the report week.

|

All Volumes

in BCF |

Current

Stocks (Fri,11/30) |

Estimated

6-Year (1995-2000) Average |

Percent

Difference from 6 Year Average |

Net Change

from Last Week |

One-Week Prior

Stocks (Fri,11/23) |

|

|

East Region |

1,851 |

1,699 |

9.0% |

0 |

1,851 |

|

|

West Region |

382 |

352 |

8.4% |

-19 |

401 |

|

|

Producing Region |

907 |

710 |

27.7% |

3 |

904 |

|

|

Total Lower 48 |

3,140 |

2,761 |

13.7% |

-16 |

3,156 |

|

|

Note: net change data are estimates published by

AGA on Wednesday of each week. All

stock-level Figures are EIA estimates based on EIA monthly survey data and

weekly AGA net-change estimates.

Column sums may differ from Totals because of independent rounding. |

||||||

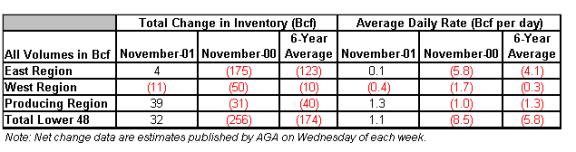

Until the final week of November, overall storage

stocks increased each week this heating season. This pattern contrasts greatly

with storage activity typical for this time of year, and especially with the

high drawdowns during November 2000.

The atypical storage activity in November 2001 was largely the result of

warmer than normal temperatures across the United States, which contrasts

sharply with last year when colder than normal temperatures drove large withdrawals

from storage. In November 2001, heating

degree-days were almost 25 percent below normal in the United States, while

heating degree-days were 16 percent above normal in November 2000. The difference in monthly storage activity

between 2000 and 2001 reflects this large differential in heating

degree-days. In November 2000,

withdrawals from storage totaled 256 Bcf, 47 percent larger than the 6-year

average, while in November 2001, the net change in storage was a net addition

of 32 Bcf.

During the past 6 years, net withdrawals from

storage averaged roughly 123 Bcf in November in the East; this year net

additions to storage in the East were roughly 4 Bcf. This difference was even stronger in the Producing region. In

contrast with the 6-year average net withdrawal of 40 Bcf during

November, the Producing region, which did not record a net withdrawal in the

AGA reports during November 2001, injected 39 Bcf into storage. Net withdrawals in the West region were

slightly higher than the 6-year average: 11 Bcf in 2001 compared with 10

Bcf. However, extraordinarily large net

withdrawals in the final week of the month accounted for all of the net weekly

withdrawals from storage. Up until the

final week of November, the West did not record a week with a net withdrawal

from storage, injecting 8 Bcf into storage.

Other Market

Trends:

In its latest Short-Term

Energy Outlook, released on Thursday, December 6, the Energy

Information Administration (EIA) projects that natural gas wellhead prices will

average $1.96 per thousand cubic feet

(or about $1.91 per MMBtu, using an average heat content of 1,027 Btu

per cubic foot of dry natural gas) in 2002.

Price weakness is attributed to warm weather, the continued weakness in

U.S. industrial production, and the atypical build in natural gas storage

levels in November. Barring some very

cold weather in the near term, EIA projects that natural gas demand for the

fourth quarter of 2001 and first quarter of 2002 will decline by 5.0 percent

compared with growth of 6.7 percent last winter. Moreover, EIA concludes that, “…under base case (normal weather)

assumptions, spot wellhead prices, which averaged $6.49 per thousand cubic feet

last winter, are expected to be two-thirds lower this winter at about $2.15 per

thousand cubic feet.”

Summary:

Spot

gas trading began and ended the week with price surges that were only partially

offset by midweek declines, as intra-day price volatility moderated. Futures prices trended down for a second

consecutive week, but with significantly smaller cumulative declines. NWS near-term weather forecasts call for a

continuation of the warmer-than-normal weather pattern in the eastern

two-thirds of the nation at least through the middle of December.

{kind=link}

{kind=link}