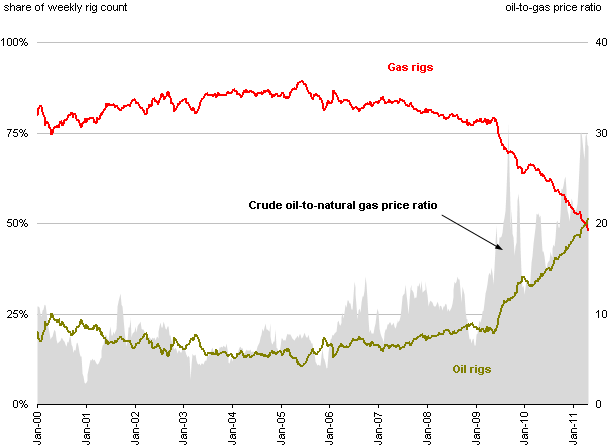

U.S. oil rig count overtakes natural gas rig count

Note: The crude oil-to-natural gas price ratio is calculated by dividing the spot prices of Brent crude oil ($/barrel) by the spot price of natural gas at the Henry Hub ($/MMBtu.) In the past, the crude oil price most utilized for this calculation was West Texas Intermediate (WTI). Under current market conditions, with the WTI price having diverged from other crude oil streams due to transportation bottlenecks at its Cushing, OK delivery point, the price of Brent crude oil is more representative of the broader crude oil market.

The Baker Hughes rig count presently shows a virtually even split between oil-directed and gas-directed rigs. This represents a major departure from the historical rig distribution. Natural gas rigs generally accounted for between 80% and 90% of the total weekly rig count throughout most of the 2000s. However, starting in about

mid-2009 (when the overall rig count reached its low point after peaking in September 2008), the number of rigs targeting oil deposits has climbed sharply.

Two factors are chiefly responsible for this shift: an increase in oil prices relative to natural gas prices and efficiency gains related to horizontal drilling for natural gas. The ratio between the spot prices of crude oil and natural gas gauges the fuels' relative market value. As can be seen in the chart, the crude oil-to-natural gas price ratio, which averaged about 9 from 2000 through mid-2009, has since risen considerably. The ratio (calculated by dividing the spot price of crude oil, dollars per barrel, by the spot price of natural gas, dollars per MMBtu) surpassed 30 in September 2009 and averaged close to that in April 2011. Moreover, operators can produce more natural gas with fewer rigs now due to greater reliance on horizontal drilling and improvements in rig efficiencies such as drilling more wells per rig and shortening drilling duration.

Higher relative crude prices encourage operators to focus more sharply on crude oil and natural gas liquids developments. This shift can be clearly seen in the significant redistribution of the Nation's rig fleet since mid-2009.