Released: September 10, 2014

Next Release: September 17, 2014

Changes in heating oil sulfur specifications in the U.S. Northeast will likely increase ultra-low sulfur diesel demand this winter

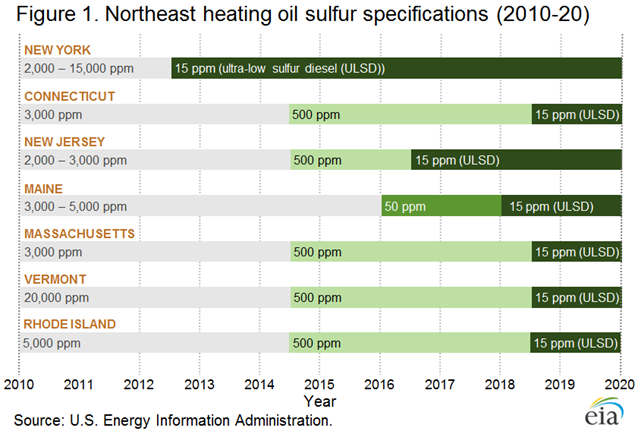

Reductions in the maximum sulfur content of heating fuels in five northeastern states will likely result in higher demand for ultra-low sulfur diesel (ULSD). On July 1st, New Jersey, Massachusetts, Connecticut, Vermont, and Rhode Island reduced the maximum allowable content of sulfur in heating oil to 500 parts per million (ppm) from 20,000–3,000 ppm. It is expected that heating oil meeting the 500 ppm specification will be blended from higher-sulfur heating oil and ultra-low sulfur diesel (ULSD), which has a maximum sulfur content of 15 ppm. The 500 ppm sulfur limit for heating fuel is an interim step in most Northeast states’ plans to reduce the acceptable maximum sulfur level to 15 ppm by mid-2016 (New Jersey) or during 2018 (Figure 1).

U.S. home heating oil consumption is highly concentrated in the Northeast. Four-fifths of all homes in the United States that use heating oil are located in the Northeast (source: U.S. Census Bureau, 2012 American Community Survey). Moreover, 25% of homes in the Northeast, or 5.3 million homes, use oil as their main heating fuel.

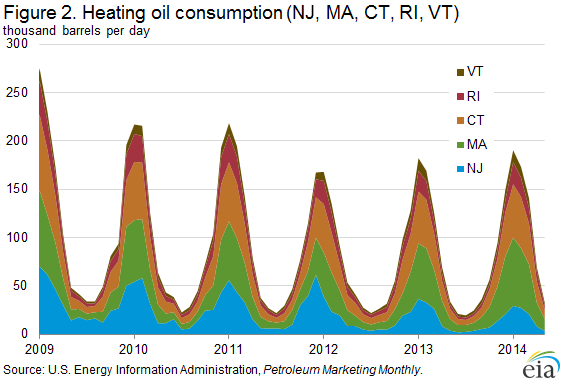

The five Northeastern states adopting lower sulfur limits this year have used an average of 139,000 barrels per day (bbl/d) of No.2 heating oil during the past five winters (October – March). Massachusetts and Connecticut, the largest consumers among the five states, averaged 42,000 bbl/d and 40,000 bbl/d, respectively over the past five winters. Demand typically peaks in January, with the January average demand for all five states combined over the past 5 years averaging 195,000 bbl/d. However, demand in the region has been declining, as existing homes that use heating oil for space heating convert to natural gas and as fewer new homes are built to use heating oil (Figure 2).

U.S. refineries, as well as refineries in the Atlantic Basin that supply distillate to the Northeast United States, do not typically produce substantial volumes of 500 ppm sulfur specification distillate. In 2013, U.S. refineries produced 146,000 bbl/d of distillate with sulfur content greater than 15 ppm but less than 500 ppm, almost of all of which was produced in the Gulf Coast region. The East Coast (PADD 1) produced only 3,000 bbl/d. ULSD was 90% of total U.S. refinery net production of distillate in 2013.

As a result of this shortfall in refinery production of 500 ppm distillate, heating oil market participants in the Northeast will likely pursue one of several strategies. One option is to supply ULSD, which, as noted, has a maximum sulfur content of 15 ppm and which is used primarily as transportation fuel, to meet heating oil demand.

U.S. refineries produce substantial volumes of ULSD and the product is readily available in the New York Harbor area because the sulfur specification for heating oil in New York was reduced to 15 ppm in 2012., Additionally the New York Mercantile Exchange (Nymex) converted the standard heating oil futures contract to 15 ppm in May, 2013. Thus, the Northeast has access to a fungible distillate product that can supply both home heating demand as well as transportation demand and that does not require separate storage and handling facilities for the different fuels. However, because ULSD typically costs more that higher-sulfur heating oil, homeowners could face higher prices to heat their homes.

A second option is to blend higher-sulfur distillate with ULSD to produce 500 ppm heating oil. This option requires separate storage and handling facilities for the two fuels, but allows the blender to capture the price difference between the higher-priced ULSD and the lower-priced higher-sulfur distillate. Based on a blend of 80% ULSD to 20% No. 2 heating oil, to meet the 500 ppm sulfur limit, blending the two fuels would yield a 2-cent-per-gallon average margin based on August spot prices in New York harbor.

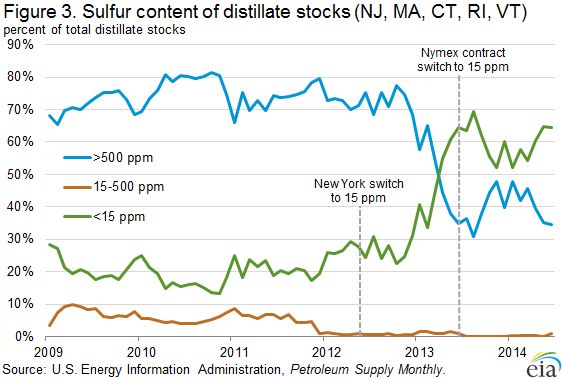

As winter approaches, inventories take on greater importance. With the change in the sulfur specification on the horizon, the sulfur level of distillate fuel in inventory in the converting states has changed. Before 2013, the percentage of distillate inventory in the converting states that was 500 ppm sulfur content or greater averaged over 70%. Ahead of July 2013, when the Nymex distillate specification changed to ULSD, the quality of distillate held in inventory began to shift.

Many of the bulk terminals qualified to deliver against the Nymex are located in New Jersey, and as a result much of the distillate inventory in New Jersey was converted to a lower-sulfur specification in advance of the May 2013 contract deadline. As the July 1, 2014 specification change approached, the share of distillate inventories the converting states with sulfur content under 15 ppm increased further (Figure 3).

The latest state-level inventory data (June) show that low-sulfur distillate now makes up 64% of total distillate inventories in the converting states, while distillate with a sulfur content greater than 500 ppm now only makes up 35%. That higher-sulfur distillate inventories have not dropped further is an indication that inventory holders in some states intend to blend. However, as a 15 ppm sulfur limit is planned for these states in 2016 and 2018, the share of distillate inventories with a sulfur content of less than 15 ppm is expected to continue to grow in the future. Only 1% of total distillate inventories in the converting states are of a distillate with sulfur content greater than 15 ppm but less than 500 ppm.

While the change in Northeast heating oil specifications likely will increase demand for ULSD, the increased low-sulfur demand should easily be met through a combination of domestic refinery production and imports from the actively traded Atlantic Basin market.

Gasoline prices mostly lower, diesel fuel prices flat

The U.S. average price for regular gasoline as of September 8, 2014, was $3.46 per gallon, down less than a cent from the previous week, but 13 cents lower than the same time last year. The West Coast price decreased two cents to $3.77 per gallon, while the Rocky Mountain price decreased one cent to $3.63 per gallon. The East Coast price fell less than a penny to remain at $3.41 per gallon. The Midwest and Gulf Coast prices both increased less than a cent, rising to $3.44 per gallon and remaining at $3.22 per gallon, respectively.

The U.S. average price for diesel fuel was unchanged from the previous week at $3.81 per gallon, 17 cents lower than the same time last year. There was little change in regional prices across the nation, with the Gulf Coast showing the largest change at a half-cent decrease, but remaining at $3.72 per gallon. The Midwest price decreased less than a cent to remain at $3.75 per gallon. The East Coast, Rocky Mountain, and West Coast prices each increased less than a penny, to remain at $3.84 per gallon, $3.87 per gallon, and $4.03 per gallon, respectively.

Propane inventories down slightly

U.S. propane stocks decreased by 0.1 million barrels last week to 76.0 million barrels as of September 5, 2014, 11.5 million barrels (17.9%) higher than a year ago. Gulf Coast inventories decreased by 0.6 million barrels and East Coast decreased by 0.2 million barrels. Midwest inventories increased by 0.6 million barrels while Rocky Mountain/West Coast inventories remained unchanged. Propylene non-fuel-use inventories represented 4.7% of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

| Retail Data | Change From Last | Retail Data | Change From Last | ||||

| 09/08/14 | Week | Year | 09/08/14 | Week | Year | ||

| Gasoline | 3.457 | Diesel Fuel | 3.814 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Change From Last | Stocks Data | Change From Last | ||||

| 09/05/14 | Week | Year | 09/05/14 | Week | Year | ||

| Crude Oil | 358.6 | Distillate | 127.5 | ||||

| Gasoline | 212.4 | Propane | 76.046 | ||||