Released: July 30, 2014

Next Release: August 6, 2014

Global growth in use of gasoline outpaces diesel in 2014

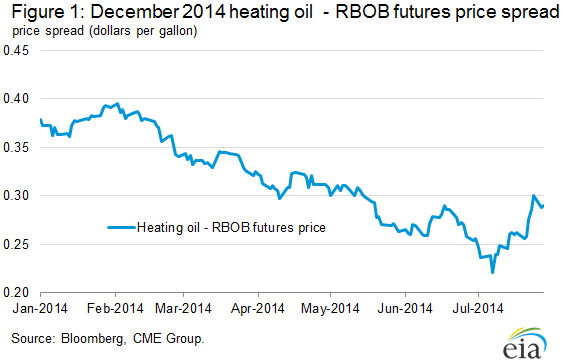

Unlike in recent years, growth in global gasoline consumption is outpacing diesel growth in 2014. At the same time, new refining capacity engineered to produce more distillate than gasoline is coming online in 2014. The narrowing spread for December 2014 futures contracts demonstrates how these two factors may be temporarily leading to a tighter global gasoline market than was expected at the beginning of the year.

On July 8, the futures price premium of New York Harbor ultra-low-sulfur diesel (heating oil) over reformulated blendstock for oxygenate blending (RBOB) for December 2014 delivery fell to 22 cents per gallon (gal) on the New York Mercantile Exchange (Nymex) (Figure 1). This was the lowest spread for December contracts since 2010.

The decline in December contract differentials this year is a result of both the weakening of heating oil prices and the strengthening of gasoline prices. The December 2014 heating oil-Brent crack spread averaged 42 cents/gal in January and fell to an average in July of 35 cents/gal on July 29. In contrast, the December RBOB-Brent crack spread widened from an average of 5 cents/gal in January to an average of 9 cents/gal so far in July.

Disappointing economic growth in developing economies is a key factor driving weaker than expected year-to-date growth in global distillate consumption. EIA’s expectations for total 2014 GDP growth in countries outside the Organization for Economic Cooperation and Development (OECD) fell from 4.6% in January to 3.9% in July. China’s first-quarter 2014 gross domestic product (GDP) growth was 7.4%, the lowest in a year and a half. India’s first-quarter GDP growth was 4.6%, the eighth consecutive quarter below 5%, and Brazil’s first-quarter GDP growth was 1.9%, the third straight quarter of lower year-over-year growth. Weak GDP growth in these emerging markets has a greater impact on global distillate demand, which is used primarily in the transportation of goods and services needed to improve or sustain an economy, than it does on gasoline demand. Gasoline demand is more closely related to personal income and domestic consumption.

The International Energy Agency (IEA) estimates that total non-OECD gasoline consumption growth was 3.8% in the first half of 2014, more than the consumption growth for distillate, which grew 0.7% over the same period. China’s average implied demand for diesel from January to May of 2014 was 3.4 million barrels per day (bbl/d), almost 70,000 bbl/d lower than during the same period in 2013. On the other hand, China’s average implied demand for gasoline increased 0.2 million bbl/d to 2.4 million bbl/d. Meanwhile, the Indian government’s decision to allow increases in the price of distillate from its previously subsidized rate and a review of diesel support in Europe could contribute to a shift from diesel to gasoline consumption later this year.

While diverging gasoline and diesel demand trends are main drivers in the declining December 2014 product contract spreads, the expected increase in distillate supply by the end of 2014 is also important. Over the past several years, refiners overseas and in the United States invested heavily in new projects and expansions to attain higher distillate production yields in anticipation of strong global distillate demand growth. In general, the increase in distillate yields results in lower gasoline production ratios. Some of the larger and more recent global refining projects include the 400,000-bbl/d SATORP refinery in Jubail, Saudi Arabia, which began operating in late 2013 and is configured to produce 216,000 bbl/d of distillate and jet fuel compared to 55,000 bbl/d of gasoline, according to the Oil Price Information Service. Also in Saudi Arabia, the 400,000-bbl/d Yasref refinery in Yanbu is scheduled to be operational in the latter half of 2014 and will produce about 260,000 bbl/d of distillate compared with 90,000 bbl/d of gasoline. A portion of the heating oil produced in these new refineries in Saudi Arabia may be allocated for domestic power generation to replace direct crude oil burn. In India, the Indian Oil Corporation’s 300,000-bbl/d refinery in Paradip is scheduled to start commercial production by the end of 2014 and produce about 120,000 bbl/d of diesel and 80,000 bbl/d of gasoline. U.S. refineries also modified operations to produce more distillate, with the annual U.S. distillate-to-gasoline production ratio rising from 0.47 in 2010 to 0.52 in 2013.

Refinery construction and expansions take years to plan, finance, and build. Companies undertake these projects to meet estimated demand many years into the future. Despite recent weakness, long-term forecasts for growth in emerging market economies remain strong. If expected non-OECD economic growth materializes, it could lead to a return of robust distillate consumption growth.

Gasoline and diesel fuel prices down for fourth consecutive week

The U.S. average retail price of regular gasoline decreased 5 cents this week to $3.54 per gallon as of July 28, 2014, 11 cents per gallon lower than last year at the same time. The national average price has fallen for four consecutive weeks, and is now the lowest since early March. Prices declined in all areas of the country except the Rocky Mountains, where the average increased half a cent to $3.65 per gallon. The Midwest price declined the most, nine cents, to $3.41 per gallon. The East Coast and Gulf Coast prices each declined five cents, to $3.54 per gallon and $3.35 per gallon, respectively. The West Coast price decreased four cents to $3.92 per gallon.

The national average diesel fuel price decreased a cent this week to $3.86 per gallon, six cents less than the same time last year, and the lowest since November 2013. Prices dropped in all regions, with the East Coast experiencing the largest decline, two cents, to $3.91 per gallon. The Midwest, Gulf Coast, and West Coast each fell one cent, to $3.80 per gallon, $3.77 per gallon, and $4.02 per gallon, respectively. The Rocky Mountain price decreased less than a penny to remain at $3.89 per gallon for a second week.

Propane inventories continue to rise

U.S. propane stocks increased by 1.8 million barrels last week to 67.2 million barrels as of July 25, 2014, 5.9 million barrels (9.6%) higher than a year ago. Midwest inventories increased by 0.8 million barrels while Gulf Coast and East Coast inventories each increased by 0.4 millionbarrels. Rocky Mountain/ West Coast inventories increased by 0.1 million barrels. Propylene non-fuel-use inventories represented 6.1% of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

| Retail Data | Change From Last | Retail Data | Change From Last | ||||

| 07/28/14 | Week | Year | 07/28/14 | Week | Year | ||

| Gasoline | 3.539 | Diesel Fuel | 3.858 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Change From Last | Stocks Data | Change From Last | ||||

| 07/25/14 | Week | Year | 07/25/14 | Week | Year | ||

| Crude Oil | 367.4 | Distillate | 126.7 | ||||

| Gasoline | 218.2 | Propane | 67.201 | ||||