Released: March 19, 2014

Next Release: March 26, 2014

Crude oil inventories at Cushing down 29% over the past seven weeks

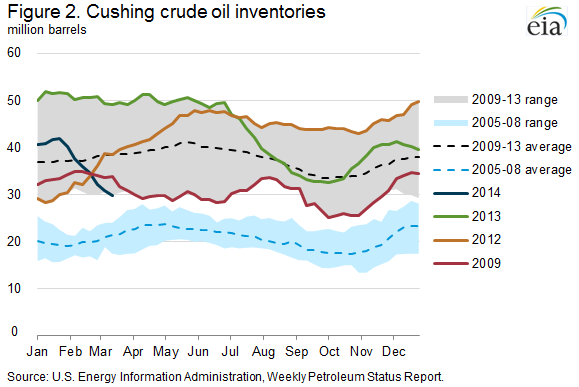

Crude oil inventories at Cushing, Oklahoma, the primary crude oil storage location in the United States and the delivery location for the New York Mercantile Exchange (Nymex) West Texas Intermediate (WTI) crude oil futures contract, declined 12 million barrels (29%) over the past seven weeks. On March 14, 2014, Cushing inventories were 30 million barrels, 19 million barrels lower than a year ago and the lowest level since early 2012.

The recent drawdown of stocks at Cushing resulted from (1) the startup of TransCanada's Cushing Marketlink pipeline, which is now moving crude from Cushing to the U.S. Gulf Coast; (2) sustained high crude runs at refineries in Petroleum Administration for Defense Districts (PADD) 2 (Midwest) and 3 (Gulf Coast), which are partially supplied from Cushing; and (3) expanded pipeline infrastructure and railroad shipments that have made it possible for crude oil to bypass Cushing storage and move directly to refining centers in PADDs 1 (East Coast) and 5 (West Coast).

In December 2013, TransCanada began injecting crude from Cushing to fill the Marketlink pipeline before its commercial startup. Marketlink linefill has been estimated at 3 million barrels. In late January, TransCanada completed the first delivery of crude oil via Marketlink to U.S. Gulf Coast refineries. Trade press has reported that crude oil deliveries via Marketlink are expected to average 525,000 barrels per day (bbl/d) in 2014.

PADD 2 refinery utilization averaged 92% in 2014 through March 14, up from 89% over the same period in 2013. Refinery utilization in PADD 3 was also higher, up 4%, even though PADD 3 refinery capacity increased. Refinery crude inputs in PADDs 2 and 3 for year-to-date 2014 through March 14 averaged 780,000 bbl/d higher than in 2013.

Steep backwardation (when near-term prices are higher than longer-term prices) also incentivized selling crude out of inventory. Since early January, the WTI 1st-13th price spread increased from less than $6/bbl to $10/bbl on March 19. With Marketlink operational, more crude can flow out of inventory at Cushing to refineries in the Gulf Coast in response to market price signals.

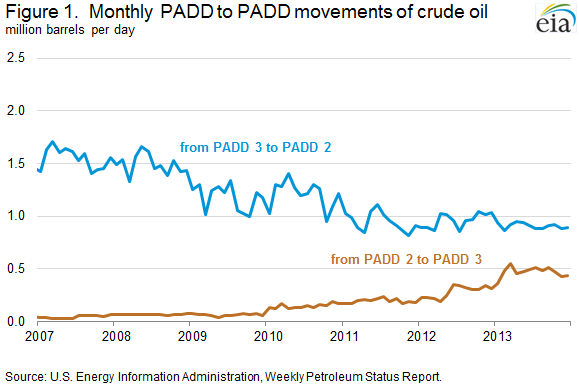

Marketlink is the most recent in a series of infrastructure developments that have either increased Cushing crude takeaway capacity or made it possible to bypass Cushing and move crude directly to refining centers. In January 2013, significant new takeaway capacity was added with the completion of Enbridge/Enterprise Seaway's 250,000-bbl/d pipeline expansion. With new infrastructure online, average crude movements from PADD 2 to PADD 3 rose to 470,000 bbl/d in 2013, 68% higher compared with 2012 (Figure 1). With these expansions, the current situation at Cushing is very different from that during the 2010-12 period when additions of roughly 815,000 bbl/d of pipeline capacity into Cushing far exceeded additions of 150,000 bbl/d in capacity out of Cushing.

New pipelines that bypass Cushing also came online in 2013. Sunoco's Permian Express pipeline and Magellan's Longhorn pipeline began delivering an additional combined 315,000 bbl/d of Permian Basin crude directly to the Gulf Coast, while rapid development of crude-by-rail networks has made it possible to move Bakken crude to East Coast and West Coast refineries.

With the completion of Marketlink and other infrastructure, flows from Cushing to the Gulf Coast are no longer constrained. EIA weekly crude oil inventory data for 2014 show PADD 3 stocks have built 28 million barrels (17%) over the past seven weeks as inventory flows south from Cushing. As a result, while Cushing inventories have broken out of the bottom of the 5-year range, Gulf Coast inventories broke out of the top of the 5-year range.

Despite the considerable decline in Cushing inventories, stocks remain well above the top of the 2005-08 range (Figure 2). Over the past several years, much of the rapidly rising volume of crude oil produced from tight oil formations in the Midcontinent was delivered to Cushing storage. Because takeaway capacity from Cushing storage was insufficient, inventories there rose. Today, Cushing inventory levels have fallen to levels that reflect current market conditions and although reduced, remain consistent with crude supply requirements to meet regional refinery demand.

Gasoline price increases, diesel fuel sheds two cents

The average U.S. price for regular gasoline was $3.55 per gallon as of March 17, 2014, an increase of four cents from a week ago, but 15 cents less than a year ago. Prices on the West Coast increased by six cents to $3.81 per gallon. Retail gasoline prices in the Midwest and Gulf Coast increased by four and three cents from last week respectively, to $3.57 and $3.28 per gallon. The East Coast price of $3.52 per gallon was up three cents from last week.

The average U.S. on-highway diesel fuel price decreased to $4.00 per gallon as of March 17, 2014, down two cents from last week, and four cents less than the same time last year. The East Coast, Midwest, and West Coast had prices drop by two cents, to $4.14, $3.99, and $4.02 per gallon respectively. Rocky Mountain and Gulf Coast prices decreased by a penny from last week, to $3.99 and $3.80 per gallon respectively.

Residential heating oil and propane prices decrease

Residential heating oil prices decreased 7 cents per gallon to reach a price of $4.12 per gallon during the period ending March 17, 2014. This is over 9 cents per gallon higher than last year's price at this time. Wholesale heating oil prices fell by more than 12 cents per gallon last week to $3.19 per gallon.

The average residential propane price decreased by nearly 9 cents per gallon last week to $3.08 per gallon, almost 77 cents per gallon higher than the same period last year. Wholesale propane prices decreased by nearly 6 cents per gallon to $1.37 per gallon as of March 17, 2014.

This is the last data collection for the 2013-2014 SHOPP season. Data collection will resume on October 6, 2014 for publication on Wednesday, October 8, 2014.

Propane inventories gain

U.S. propane stocks increased by 0.2 million barrels to end at 26.2 million barrels last week, 15.5 million barrels (37.2%) lower than a year ago. Gulf Coast stocks posted the only gain with 0.8 million barrels of new inventories. Midwest inventories decreased by 0.4 million barrels, East Coast stocks dropped 0.1 million barrels and Rocky Mountain/West Coast stocks were down slightly. Propylene non-fuel-use inventories represented 12.9% of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

|

|

||||||

| Retail Data | Change From Last | Retail Data | Change From Last | ||||

| 03/17/14 | Week | Year | 03/17/14 | Week | Year | ||

| Gasoline | 3.547 | Heating Oil | 4.123 | ||||

| Diesel Fuel | 4.003 | Propane | 3.079 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Change From Last | Stocks Data | Change From Last | ||||

| 03/14/14 | Week | Year | 03/14/14 | Week | Year | ||

| Crude Oil | 375.9 | Distillate | 110.8 | ||||

| Gasoline | 222.3 | Propane | 26.241 | ||||