Released: September 14, 2011

Next Release: September 21, 2011

Key factors affecting the outlook for restoring Libya's oil production

As the fighting in Libya begins to wind down and the Transitional National Council (TNC) establishes itself as the internationally recognized government, it is timely to review the many factors that will affect the pace and timing of the restart of the Libyan oil industry.

The TNC leadership, which views oil revenues as a means to rebuilding the country, and participants in world oil markets, who continue to grapple with tightness in the global supply of high-quality crude, share a common interest in restoring Libya's oil production and exports. When this will happen is uncertain and depends to a significant extent on the political, military, and security situation that will determine when companies can return to oil fields to repair and/or restart production. It is also worth noting that at the time of writing, only the European Union and United Nations had lifted sanctions on Libya; U.S. sanctions remain in place.

Opinions vary across analysts. Some predict a slow and protracted recovery, while others are more optimistic, pointing to TNC statements on its commitment to restarting oil production. Most international oil companies (IOCs) have been cautious regarding their public statements on resuming production.

Political and military outcomes will each play an important role in creating conditions that speed or retard production activity. Politically, there must be sufficient legitimacy and legal clarity to allow for financing activity and exchanges of funds. A recognized government with the institutions in place to uphold contracts and manage revenues will be necessary for the IOCs to return. While the TNC has stated that it will respect existing contracts, IOCs seeking to purchase oil from Libya or invest in the country's oil sector must be able to identify their institutional and financial counterparts within the new regime. One question to be addressed is whether oil revenues should be paid to the national oil company, to the oil ministry, or to other parties. Another option might be to allocate funds to an escrow account pending clarification of future arrangements so that operations can resume. IOCs also need to consider that the government and its institutions are likely to continue to evolve over time.

Militarily, remnants of the conflict may also continue to present challenges. As of this writing, Gaddafi loyalists are still in control of a few areas of the country and some analysts believe that pockets of resistance will remain even after the fighting has come to an end. Beyond the military conflict, security concerns could delay the return of oil workers and the resumption of production. While the oil industry is not very labor-intensive, a large part of the labor employed in the sector is highly specialized, and, in many cases, comprises expatriates who are likely to have found employment elsewhere. The conflict also scattered the Libyan workforce. It will take time to reassemble the staff, and even then there is a risk that the aftermath of the conflict could affect workforce morale and cohesion as employees face up to their differing roles and loyalties before and during the fighting.

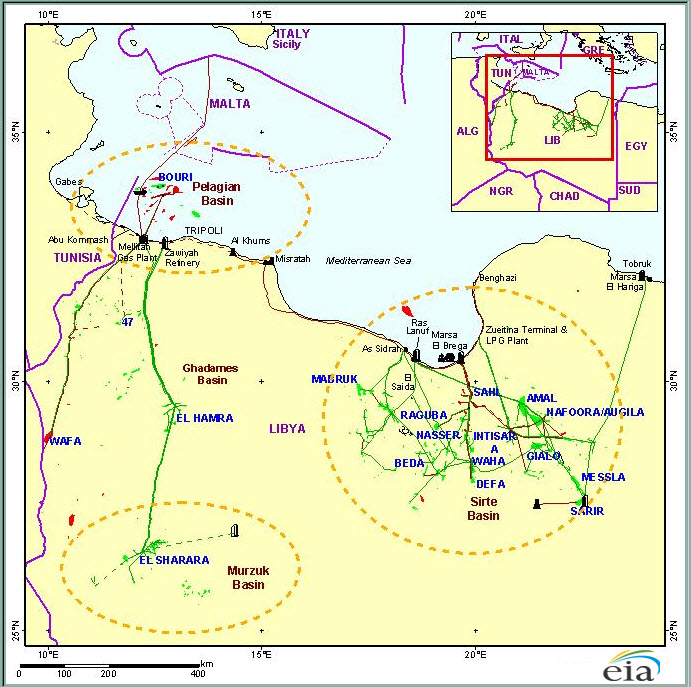

Some of the security concerns are directly tied to the oil infrastructure (Figure 1). For instance, Gulf of Sirte, an area that accounts for about two-thirds of Libyan oil production, saw the heaviest fighting and the most damage and is likely to face continuing security concerns. In terms of security, press reports suggest that the oil terminals and surrounding infrastructure of Ras Lanuf and Brega have been booby trapped with explosive devices. The Financial Times cited land mine experts as saying it could take 18 months to clear some of the explosives - an issue that will need to be addressed before the known damage can be fully repaired. Resuming production will bring with it its own security concerns as the infrastructure is a relatively easy target. During the conflict, oil production out of the east was sporadic at times because when production resumed, it became a target for loyalist forces.

Figure 1. Libya's Oil Infrastructure

Source: Wood Mackenzie

And finally, the damage itself. The Libyan oil industry is divided up into nine separate streams, each with its own transport and export infrastructure. Geographically, it can be divided into three sections, Eastern, Central, and Western. The reported status of infrastructure is summarized below; exports by terminal are estimated based on Lloyd's List Intelligence APEX database and other press reports.

Most of Libya's oil production is located around the Gulf of Sirte, in the central part of the country, where it was damaged by the fighting. This region has four terminals, Es Sider, Brega, Ras Lanuf, and Zueitina. Es Sider, the largest of the terminals, came under direct attack during the fighting and there were reports of damage to at least its storage tanks, metering equipment, and a feeder pipeline. Prior to the fighting, this terminal exported close to 350,000 bbl/d from the Waha concession, a partnership between the Libyan National Oil Corporation (LNOC) and three U.S. companies: Hess, ConocoPhillips, and Marathon.

The terminals of Brega and Ras Lanuf, which combined exported over 300,000 bbl/d in 2010, were severely affected by the fighting. Ras Lanuf is reported to have damage to its power supply and, more significantly, these facilities are believed to have been booby trapped with explosive devices laid in and around the oil infrastructure. The Zueitina terminal on the central eastern part of the Gulf of Sirte accounted for close to 150,000 bbl/d of exports in 2010; this terminal is fed by the Attifel and Zueitina streams and there were reports of explosions near the terminal.

The Eastern infrastructure consists of two main fields, Messla and Sarir, oil from which is exported via pipeline to the Tobruk (Hariga) terminal in the east. This stream is entirely under the operation of the Benghazi-based Arab Gulf Oil company (AGOCO), which sided with the rebels early in the conflict and maintained minimal production during the fighting. AGOCO was even able to export two shipments of approximately 500,000 bbl during the conflict, but production and exports did not reach the pre-conflict rate of around 250,000 to 300,000 bbl/d. However, production out of this area made it a target for loyalist forces and there were reports of damage in and around Messla field, including some power infrastructure.

Other production that was maintained during the conflict was that from the southwest fields that fed into the Zawiyah refinery where it was processed for domestic consumption in Gaddafi-held areas near Tripoli. Production at the refinery (which has a reported capacity of 120,000 bbl/d) was maintained until it was shut-in in early August as a result of rebel sabotage to the pipeline connecting the refinery. This affected both fuel supplies and electricity generation in the region. Oil production for the Zawiyah export terminal is the Sharara blend that originates in the Murzuq basin. Exports in 2010 were estimated to be close to 200,000 bbl/d while overall production was estimated as high as 320,000 bbl/d. The second western stream is Mellitah, but there is little information available about the current status of the field. Exports in 2010 were estimated to be around 150,000 bbl/d, also coming from the Murzuk basin and including the El-Feel (Elephant) fields.

Additional production could come from the offshore Bouri (Eni-operated) and Al Jurf (Total and Wintershall) crude streams if the IOCs return. These fields and floating production storage and offloading units (FPSOs) were not affected by the conflict but were shut in so their status will need to be evaluated. Combined offshore production was about 75,000 bbl/d prior to the conflict.

In some cases, there are different degrees of repairs that could be taken into consideration. For instance, some "quick fix" options that would have been preferable during the fighting might not be the best way to move forward when planning for the longer term. For example, metering stations that were damaged can be bypassed if the goal is simply to keep volumes flowing. However, it is in the long-term interest of companies to make permanent repairs to avoid any damage that could be caused by temporary bypass fixes and to track transfer of crude between companies.

Finally, any possible timeline for exports will also need to take into account Libya's domestic oil needs. In 2010, Libyan oil consumption was estimated to average 290,000 bbl/d and would be expected to increase in order to meet the country's reconstruction needs. It is likely that any early production will be refined domestically, to the extent possible, or swapped out in exchange for the needed refined products.

In summary, political and security issues will remain the most significant factor in returning Libyan crude production. Under stable political and security conditions, the damaged infrastructure can be repaired, some parts faster than others.

Retail gasoline and diesel prices decline

The U.S. average retail price of regular gasoline decreased this week, losing over a penny to fall to $3.66 per gallon. The average price is $0.94 per gallon higher than last year at this time. Regional changes were mixed with the largest decline occurring in the Midwest as the price fell just under three cents to average $3.68 per gallon. The Gulf Coast price decreased two cents to $3.47 per gallon. The East Coast price declined a penny to an average $3.63 per gallon. Prices rose just over two cents in the Rocky Mountain region and a fraction of a penny on the West Coast to $3.60 per gallon and $3.87 per gallon, respectively.

The national average diesel price totaled $3.86 per gallon after decreasing less than a penny. The diesel price is $0.92 per gallon higher than last year at this time. The Midwest and Gulf Coast prices fell a penny to put prices at $3.84 per gallon and $3.79 per gallon, respectively. The East Coast diesel price decreased to $3.88 per gallon. The price in the Rocky Mountains increased a cent to $3.90 per gallon while the West Coast average stayed at $3.98 per gallon.

Propane stocks resume build

Propane stocks gained 1.2 million barrels last week to bring the total U.S. inventory level to 54.7 million barrels. Although propane stocks have risen for 20 of the last 21 weeks, inventories are 9.0 million barrels (14 percent) lower than last year and are tracking below the average range for this time of year. The largest gain was in the Midwest region with 1.2 million barrels of new propane stocks. Meanwhile, the East Coast and Rocky Mountain/West Coast regions gained 0.2 million barrels and 0.1 million barrels, respectively, which were offset by a draw in the Gulf Coast region of 0.3 million barrels. Propylene non-fuel use inventories represented 5.3 percent of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

| Retail Data | Changes From | Retail Data | Changes From | ||||

| 09/12/11 | Week | Year | 09/12/11 | Week | Year | ||

| Gasoline | 3.661 | Diesel Fuel | 3.862 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Changes From | Stocks Data | Changes From | ||||

| 09/09/11 | Week | Year | 09/09/11 | Week | Year | ||

| Crude Oil | 346.4 | Distillate | 158.5 | ||||

| Gasoline | 210.8 | Propane | 54.745 | ||||