Released: May 4, 2011

Next Release: May 11, 2011

Oil from the Americas: a current and future source for the United States

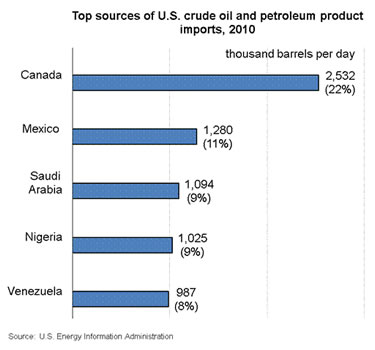

While unrest in the Middle East and North Africa has focused attention on crude oil supply in that part of the world, this edition of This Week In Petroleum focuses on the largest exporters in the Americas ( Canada, Mexico, and Venezuela), which supplied 41 percent of U.S. total petroleum imports in 2010.

The United States' largest source of petroleum imports is Canada, which supplied about 22 percent of total U.S. crude oil imports in 2010 (about 1.97 million barrels per day (MMbbl/d) of crude oil and 0.56 MMbbl/d of petroleum products). Canadian crude oil exports come mainly from its western provinces. The United States consumes essentially all (99 percent) of Canadian crude oil exports. Much of the Canadian crude oil exported to the United States originates in the oil sands, which is an extra heavy crude oil that requires additional processing or addition of diluents for export. In addition to geographic proximity, exports from Canada to the United States can utilize an existing U.S. import/refining infrastructure designed to transport and process these heavier grades of crude oil. Of the estimated 2.9 MMbbl/d of crude oil produced in Canada in 2010, 1.5 MMbbl/d of that was derived from the oil sands of Alberta. Oil sands production is currently the largest single source of U.S. crude imports. With projected growth in oil sands production, Canada's role as a supplier to the United States is likely to grow in both absolute volume and share terms.

Mexico is also a significant source of U.S. imports. In 2010, the United States imported 1.1 MMbbl/d of crude oil from Mexico. While Mexico also exports about 140,000 bbl/d of refined products to the United States, mostly residual fuel oil, naphtha, and motor gasoline blending components, it is actually a net importer of U.S. products as it imports substantial volumes of gasoline from U.S. refineries. Mexico is consistently one of the top three exporters of crude oil to the United States, along with Canada and Saudi Arabia. Mexico's crude oil exports to the United States generally rose through the 1980s and 1990s, before peaking in 2004 at 1.6 MMbbl/d. The combination of Mexico's falling crude oil production and rising domestic demand has led to a reduction in exports to the United States in recent years. Future trends will depend on the success of Mexico's efforts to increase production through increased investment and reforms, including recent actions that will allow for expanded participation by international oil companies in the country's oil sector.

Venezuela is one of the Western Hemisphere's largest exporters of crude oil. In 2010, Venezuela was the United States' fifth largest supplier of imported crude oil and petroleum products. However, U.S. imports from Venezuela have declined in recent years. In 2010, the United States imported 987,000 barrels per day (bbl/d) of crude oil and petroleum products from Venezuela, just 8.4 percent of total U.S. imports. Venezuelan crude oil imports of 912,000 bbl/d comprised the majority of those volumes. Even factoring in 255,000 bbl/d of petroleum product imports from the U.S. Virgin Islands (about 60 percent of the crude oil refined in the U.S. Virgin Islands comes from Venezuela), the significance of Venezuela to the American energy sector has declined. When combined, 2010 total U.S. imports from Venezuela and the U.S. Virgin Islands represented a 40 percent decline from their peak of 2.1 MMbbl/d in 1997. Notwithstanding the recent decline in Venezuela's exports to the United States, reflecting both its production problems and the political situation, Venezuela retains a tremendous resource base and is in close proximity to the U.S. Gulf Coast region where roughly half of U.S. refinery capacity is concentrated. Venezuela's future role as a supplier to the United States will depend on its ability to expand production from its ample resources and an improvement in bilateral relations.

While it is clear from the above that there are significant unanswered questions about future trends in supply from Mexico and Venezuela, it seems clear that the Americas as a whole will continue to be a major source of petroleum supply to the United States. Other producers in the Americas may also play an expanded role. Brazil, the tenth largest supplier of U.S. crude oil imports (and the eleventh largest for total petroleum), is increasing both its ethanol and crude oil production, which may find expanding U.S. markets in the future. Colombian production is also increasing, much of which may be destined for U.S. markets.

Finally, while the previous discussion focuses on the prospects for supply outside the United States, trends in U.S. petroleum production and use will also play a key role in determining our overall need for imports. The Annual Energy Outlook 2011, released last week, includes many sensitivity cases that explore factors affecting projected production and use of petroleum. Particularly in cases where the overall need for petroleum imports declines over time, there is ample prospect for a significant increase, perhaps even a doubling or better, in the share of total U.S. petroleum imports that are sourced in the Americas.

Retail gasoline and diesel prices move higher

The U.S. average retail price of regular gasoline added more than 8 cents over the last week to hit $3.96 per gallon. This is $1.07 per gallon higher than last year at this time and is the highest price in May since EIA began tracking weekly data in 1990. For the second straight week, the Midwest registered the biggest increase across the major regions, with prices jumping 11 cents to $4.01 per gallon. The Midwest is the now the second major region where prices average more than $4 per gallon. On the Gulf Coast and East Coast, the average gasoline price increased more than eight cents per gallon. The Rocky Mountains saw prices increase six cents on the week, while West Coast prices recorded a four-cent gain to $4.14 per gallon, the highest average regional price in the country.

The national average diesel price gained almost 3 cents this week, climbing to $4.12 per gallon. The diesel price is $1.00 per gallon higher than last year at this time. The Gulf Coast saw prices gain almost four cents, the biggest increase among the regions, but Gulf Coast prices still remain the lowest in the Nation at $4.06 per gallon. Diesel prices on the West Coast are still the highest in the country at $4.33 per gallon. The East Coast, Midwest, Rocky Mountain, and West Coast regions all recorded price increases of more than two cents per gallon on the week.

Propane stocks post a large build

U.S. propane inventories grew by 1.3 million barrels to end at 27.8 million barrels during the week ending April 29, 2011. Most of the gain occurred in the Midwest region, where stocks increased by 0.8 million barrels. Gulf Coast stocks grew by 0.5 million barrels and the Rocky Mountain/West Coast regional stocks were up by almost 0.1 million barrels. East Coast regional inventories declined by 0.1 million barrels. Propylene non-fuel use inventories represented 6.0 percent of total propane inventories.

Text from the previous editions of This Week In Petroleum is accessible through a link at the top right-hand corner of this page.

|

|

||||||

| Retail Data | Changes From | Retail Data | Changes From | ||||

| 05/02/11 | Week | Year | 05/02/11 | Week | Year | ||

| Gasoline | 3.963 | Diesel Fuel | 4.124 | ||||

|

|

||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||

| *Note: Crude Oil Price in Dollars per Barrel. | |||||||||||||||||||||||||||

|

|

||||||

|

|

||||||

| Stocks Data | Changes From | Stocks Data | Changes From | ||||

| 04/29/11 | Week | Year | 04/29/11 | Week | Year | ||

| Crude Oil | 366.5 | Distillate | 145.1 | ||||

| Gasoline | 204.5 | Propane | 27.751 | ||||